Metals & Mining, Non-Ferrous

July 16, 2026

TRADE REVIEW: Pacific alumina demand to improve in Q3, but surplus risks remain

By Nick Tan and Louissa Liau

Editor:

HIGHLIGHTS

Alumina surplus pressured prices through most of Q2

Guinea export-control concerns triggered late-quarter rally

Q3 hinges on Guinea policy, Indonesia demand growth

This report is part of the S&P Global Energy's Metals Trade Review series, where we dig through datasets and digest some of the key trends in iron ore, metallurgical coal, copper, alumina, cobalt, lithium, nickel and steel and scrap. We also explore what the next few months could bring, from supply and demand shifts to new arbitrages, and to quality spread fluctuations.

The Pacific alumina market could see stronger support in the third quarter of 2026, as uncertainty over Guinea's export controls, rising Indonesian aluminum demand, and the gradual recovery of Middle Eastern smelting capacity begin to offset Q2 surplus conditions.

Although the alumina market remains structurally well supplied, market participants increasingly expect supply-demand balances to tighten compared with the previous quarter.

Guinea's potential bauxite export controls have introduced uncertainty around future feedstock availability, while Indonesian aluminum expansions are expected to create a new source of regional demand. Concurrently, recovery in Middle Eastern alumina consumption is likely to be gradual as smelters affected by the conflict continue their restoration efforts.

Improving demand will support a more balanced market in the second half of the year, according to S&P Global Energy CERA analysts.

Middle East disruptions spark supply surplus

Following attacks on EGA and Alba facilities in late March, alumina demand in the region weakened significantly, prompting cargoes to be redirected to the Pacific market. Market participants repeatedly described the spot market as "long," citing ample availability and subdued buying interest.

Concurrently, China's alumina market faced supply pressure from rising imports and new refining capacity. Alumina imports rose 80.3% to 610,081 metric tons in April, according to China Customs data, marking the highest level in available customs records since 2015. New refinery capacity in Guangxi, including the 2.4 million mt/year Fangchenggang project, reinforced expectations of a persistent surplus.

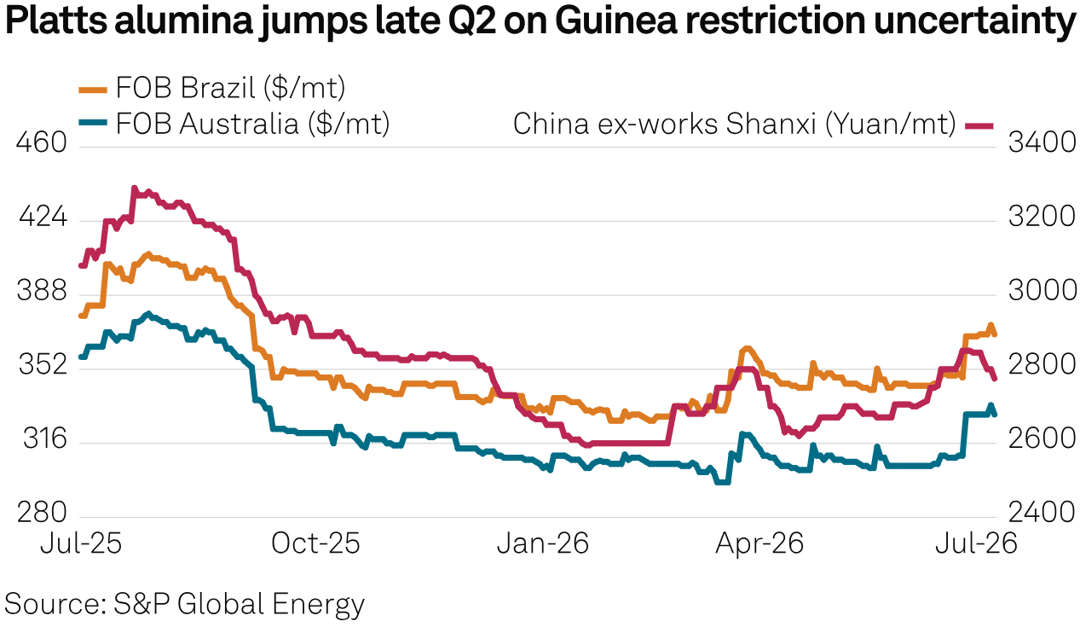

FOB Australia alumina prices were in the range of $300-$310/mt in April and May amid oversupply concerns, according to data from Platts, part of S&P Global Energy.

Despite expectations that the reopening of the Strait of Hormuz could alter trade flows, most participants described a limited impact. Cargoes originally destined for Middle Eastern smelters largely remained committed to those buyers rather than re-entering the spot market.

CERA analysts forecast the global alumina market will remain in a 1.79 million mt surplus in 2026 compared with an estimated 2.4 million mt surplus in 2025 despite improving sentiment.

Guinea concerns lift sentiment

Sentiment shifted in June after expectations of Guinea export controls resurfaced, pushing u[ Chinese alumina futures and domestic spot prices.

Chinese alumina futures saw a sharp rally, with the Shanghai Futures Exchange's most-active September alumina contract rising to Yuan 2,899/mt ($425.39/mt) on June 11, while CIF China bauxite reached a quarterly high of $69.50/dmt, according to Platts data.

However, trading activity slowed between May and June as market participants waited for policy clarity.

The stronger Chinese market eventually reopened the import arbitrage, supporting Pacific alumina prices and improving market sentiment. High freight rates had earlier kept the Pacific arbitrage closed for most of Q2.

Spot availability appeared to tighten as sellers held back cargoes amid uncertainty. Producers reported difficulty offering material for July-August delivery, while consumers increasingly reported a lack of spot offers by late June.

Indonesia provided some support through spot alumina purchases, although most sources viewed Indonesian aluminum expansions as a driver for H2 demand.

FOB Australia alumina climbed 8.19% to its highest level of Q2 2026 at $330/mt June 26, from $305/mt in early June, according to Platts data. It averaged $307.42/mt in Q2, up marginally from $306.91/mt in Q1.

Meanwhile, the Platts CIF China alumina assessment averaged $340.74/mt in Q2, up 2.83% quarter over quarter. Chinese domestic alumina prices averaged Yuan 2,702.54/mt ex-works Shanxi, up 1.62%.

Platts FOB Brazil alumina premium to FOB Australia material averaged $39.69/mt in Q2, up 38.57% quarter over quarter, reflecting tighter Atlantic basin availability and steady refinery demand.

Nevertheless, market participants emphasized that China's elevated bauxite inventories would likely delay any immediate impact from export restrictions. China imported a record 23.03 million mt of bauxite in May, up 31.9% year over year, with Guinea accounting for 85.1% of total volumes as refiners accelerated purchases ahead of possible policy changes.

Sentiment improves, surplus remains

Guinea export restrictions or quota measures could raise feedstock costs for Chinese refiners, supporting SHFE alumina futures and Pacific alumina prices in Q3. However, China's elevated bauxite inventories are likely to cushion the initial impact, suggesting that any supply shock may take time to reach to physical markets.

Indonesian aluminum expansions remain the clearest source of incremental alumina demand. CERA forecasts Indonesia's aluminum output could approach 1.2 million mt in 2026, about double 2025 levels. Indonesia's alumina exports also rose 10.3% month over month in June, highlighting the country's growing role in regional alumina trade flows.

By contrast, recovery in GCC alumina demand is expected to be gradual. Although EGA has resumed hot metal casting at its Al Taweelah smelter and reported progress ahead of schedule in restoring operations, the company still expects a full return to pre-war production levels to take up to a year.

For now, the market remains caught between improving sentiment and sufficient physical availability. Q3 prices are likely to be driven more by policy developments and expectations for future demand growth than by immediate changes in supply-demand fundamentals.