Agriculture, Energy Transition, LNG, Metals & Mining, Biofuels, Renewables, Grains, Non-Ferrous

June 30, 2026

COMMODITY TRACKER: 5 charts to watch this week

By Staff

Editor:

High renewable fuel compliance costs are reshaping US refining strategies, while Asia-Pacific LNG prices climb on Strait of Hormuz tensions and Asian refiners await sanctions clarity on Iranian crude. Meanwhile, China's bauxite imports are set to decline after May's record increase, and extreme European heat pushes French wheat prices higher.

1. Record RIN costs reshape US fuel production mix

What's happening? The US fuel market is being reshaped by record-high renewable fuel compliance costs, with refiners increasingly leaning into jet fuel production to limit exposure to road-fuel blending obligations. Under the Renewable Fuel Standard, obligated parties must blend renewable fuels or purchase compliance credits known as Renewable Identification Numbers. Platts, part of S&P Global Energy, assessed the current-year Renewable Volume Obligation at 37.6198 cents/gallon on June 26, setting a new all-time high. US jet fuel production has reached new all-time highs 18 times this year, with the latest Energy Information Administration data from June 24 showing a record 2.203 million b/d -- 7.6% above the five-year average. D4 RIN credits have soared 131% since the beginning of the year, with Platts assessing D4 RINs at $2.44/gal June 26.

What's next? The increase in RIN prices reflects biofuel blending mandates for 2026 and 2027 finalized in late March, representing the highest volumes in the 20-year history of the RFS program. The 2026 mandates rose 20.06% to 26.81 billion gallons, while the 2027 mandates increased 21% to 27.02 billion gallons compared to 2025. The Environmental Protection Agency estimated biodiesel and renewable diesel production would need to increase by more than 60% to meet these targets. With US diesel prices easing and biodiesel blending economics weakening, production could decline, potentially reducing D4 RIN generation and sustaining high prices, according to market sources.

2. Asia-Pacific LNG prices rise amid Strait of Hormuz tension

What's happening? Asia-Pacific spot LNG prices rose on June 29 following reports of the US and Iran trading fire near the Strait of Hormuz on June 28, despite an initial ceasefire agreement signed on June 17. Platts assessed the August JKM, the benchmark price for LNG cargoes delivered to Northeast Asia, at $15.908/MMBtu June 29, up 4.89% from the previous close.

What's next? Northeast Asian buyers are exploring alternatives to limit full exposure to spot prices, including joint procurement strategies and advancing deliveries under long-term contracts, according to a South Korean source. Rising temperatures in South Korea are beginning to shift sentiment, with power generators preparing for stronger summer cooling demand as the Korea Meteorological Administration issued heat wave advisories on June 29. The Platts-assessed balance-month-September time spread remained at a three-month high of 52 cents/MMBtu, reflecting prompter demand. On the supply side, Train 1 at Indonesia's Tangguh LNG project, shut since June 4, is expected to return to normal operations in July without disrupting export activities or domestic supply, Platts reported.

3. Asian refiners await sanctions clarity on Iranian crude

What's happening? Refiners in South Korea, Japan, Thailand and Taiwan are delaying purchases of Iranian crude despite competitive pricing, as they seek long-term clarity on sanctions relief before committing to spot and term deals, industry and trading sources said over June 22-24. South Korea was among the top three buyers of Iranian crude before sanctions, importing 148 million barrels in 2017, data from state-run Korea National Oil Corp. showed. Japan imported 172,216 b/d from Iran in 2017, according to data from the Ministry of Economy, Trade and Industry. Platts assessed Iran's South Pars condensate at an average discount of $5.11/b to Qatar's Deodorized Field Condensate this year to date.

What's next? Refiners are unlikely to commit to Iranian crude without strong assurance that purchases can continue freely over the long term without renewed sanctions risk. A temporary waiver lasting only 60 days would not justify operational disruption and re-optimization costs, according to feedstock managers at ENEOS and an Ulsan-based refiner. The commercial appeal of Iranian barrels remains strong, with South Pars condensate assessed at an average discount of $5.27/b against front-month Dubai in June. If sanctions are permanently lifted, competitively priced Iranian South Pars condensate and various light and sour Iranian grades would broaden supply options and spur new competition among Middle Eastern producers for Asian demand, according to the South Korean, Japanese and Thai refinery feedstock managers.

4. China's bauxite imports expected to decline in June

What's happening? China's bauxite imports are likely to decline in June after reaching a record high of 23.03 million metric tons in May, up 16.7% month over month and 31.9% year over year, according to General Administration of Customs data. The May surge was driven by concerns over potential export curbs in Guinea, the largest supplier to China, prompting Chinese alumina producers to lock in prices and restock early. Guinea accounted for 85.1% of China's bauxite imports in May, with shipments reaching 19.61 million mt. Chinese bauxite prices rose, with Platts assessing CIF China spot bauxite at $70/dry metric ton June 25 for low-temperature ore, basis 45% alumina and 3% silica, up $1/dmt from the previous assessment. Improved spot buying interest emerged as alumina refineries prepared to restock.

What's next? Despite the anticipated June decline due to Guinea's rainy season, China's bauxite imports are likely to remain elevated throughout 2026, staying above the 10 million mt monthly mark, with the country's import dependency exceeding 60%, according to market sources. For the first five months of 2026, China's bauxite imports totaled 100.69 million mt, up 18.5% year over year. Market sources said refineries are likely to continue restocking in anticipation of potential Guinean export restrictions and seasonal supply disruptions.

Further reading: METALS MONITOR: Pentagon taps miners for facilities; Dubai bans steel, copper, aluminum scrap exports

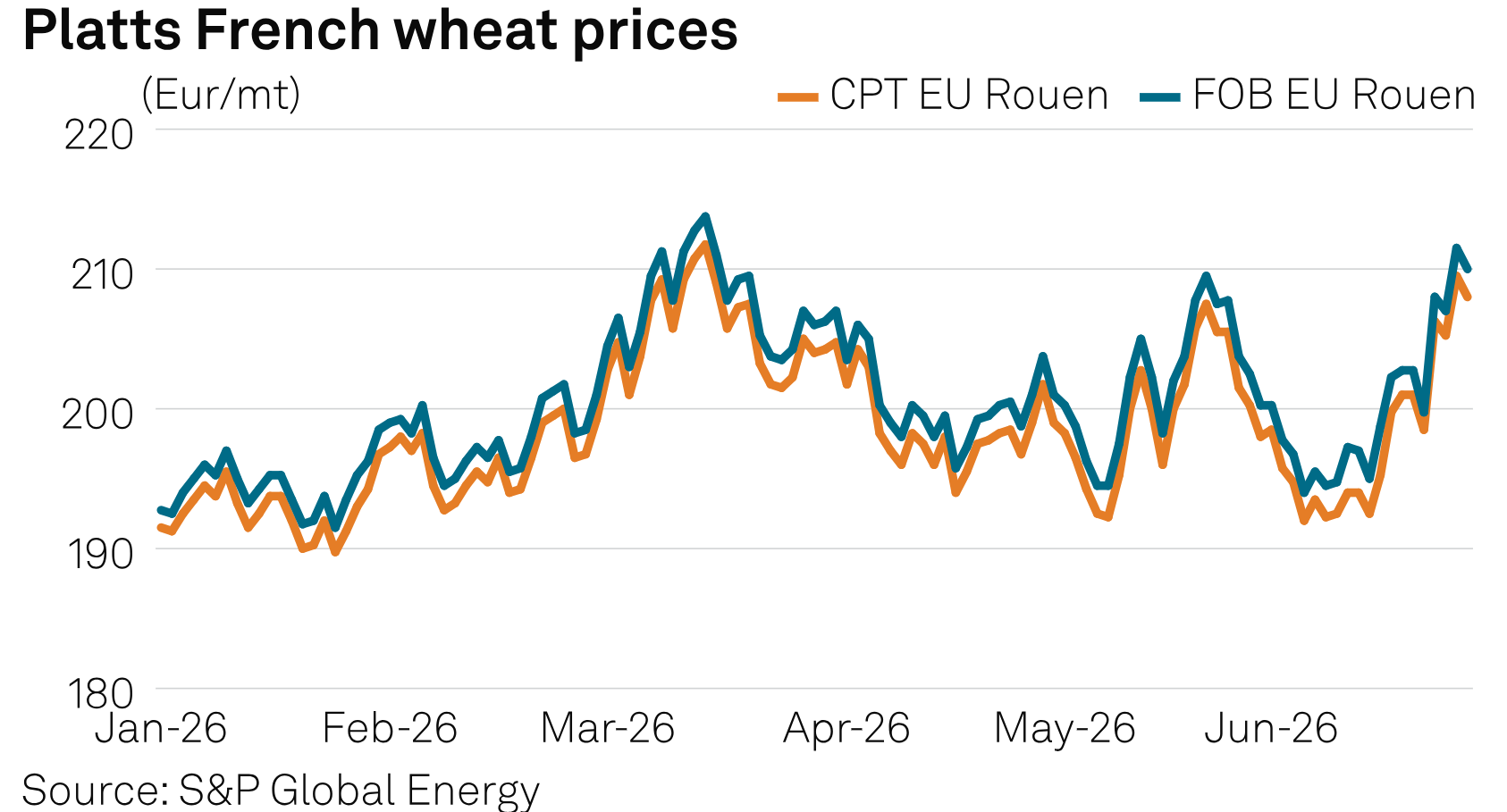

5. French wheat prices hit three-month high on heat wave concerns

What's happening? French wheat prices reached their highest level in three months as record-breaking temperatures across Europe sparked concerns about crop stress and yield losses. Platts assessed wheat 11% FOB and CPT Rouen prices at Eur211/mt and Eur209/mt respectively on June 25, the highest since March 16. France set a new national temperature record, with extreme heat spreading to Germany, Poland and the UK. While some winter crops that have already been harvested have protection, spring crops remain vulnerable. Brokers reported significant damage to spring wheat, with corn and sunflowers facing critical periods as temperatures reached 40 degrees Celsius.

What's next? The heat wave in France is gradually ending, with the system shifting east to Germany and Poland for a few days before exiting Europe. Winter grain harvest has begun in southern and Atlantic coastal regions, offering some buffer for wheat and barley, though spring barley and corn remain highly vulnerable, according to brokers.

Reporting and analysis by Aaron Tucker, Ana Hernandez, Gwen Teo, Philip Vahn, Lucy Tang and Fikayo Owoeye.