29 Jul 2021 | 19:45 UTC

US working natural gas volumes in underground storage increase 36 Bcf: EIA

Highlights

Third straight build above five-year average

Henry Hub winter strip remains above $4/MMBtu

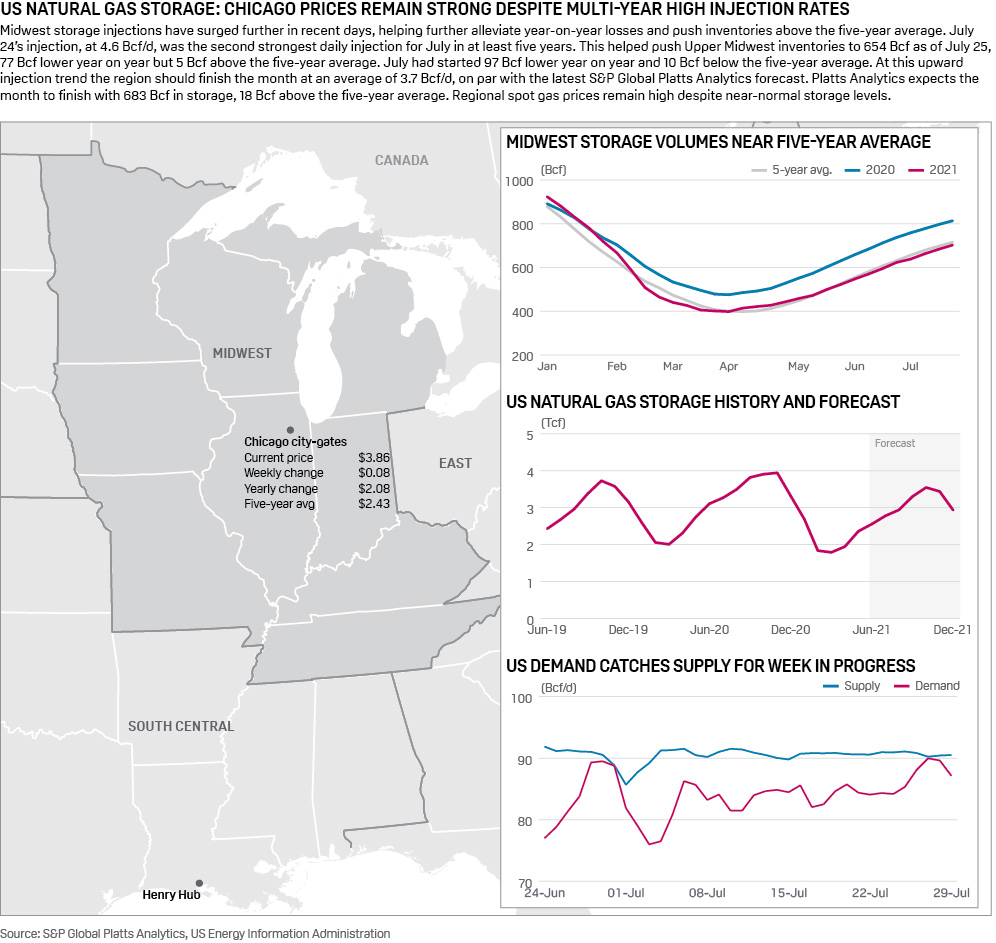

US natural gas storage fields added volumes above the five-year average for the third consecutive time for the week ended July 23, while the Henry Hub September contract, now the prompt month, surpassed $4/MMBtu.

Working gas in storage increased by 36 Bcf to 2.714 Tcf for the week ended July 23, US Energy Information Administration data showed July 29.

It was less than the 40 Bcf addition expected by an S&P Global Platts survey of analysts. It outgained the five-year average build of 28 Bcf and last year's 27 Bcf injection in the corresponding week. Although it marked the third-consecutive above-average injection, the weekly builds have not registered strong enough to make a serious dent in the lingering deficit.

Storage volumes now stand at 523 Bcf, or 16%, less than the year-ago level of 3.237 Tcf, and 168 Bcf, or 6%, less than the five-year average of 2.882 Tcf.

Total supplies fell by 200 MMcf/d from the week prior to average 95.6 Bcf/d. Small gains in onshore production were canceled out by an equal decline in offshore receipts, leaving only a dip in net Canadian imports to drive supplies slightly downward on the week. Downstream, total demand was seen rising by about 500 MMcf/d, with much of that stemming from higher gas-fired power demand.

Small net withdrawals were recorded in the Pacific and South Central regions for the second week in a row.

Prices were up sharply by midday during the July 29 session, lifted by an inventory report that was generally lower than the consensus view, indicating markets were tighter than anticipated last week.

With September now taking over the prompt-month position, balance-of-summer NYMEX Henry Hub prices were trading 8 cents higher on the day, building upon the 4 cents of gains from the July 28 session. This effectively unwound the sharp losses from July 27, when the summer contract strip fell by nearly 14 cents.

It propelled September and October prices firmly above the $4 line, averaging $4.05/MMBtu by late afternoon trading. Winter pricing also rebounded following a nearly 13 cent selloff on July 27, with July 29's 11 cent gain bringing prices from November through March up to $4.17, after briefly testing the $4 level just a few days earlier.

Platts Analytics' supply and demand model currently forecast a 16 Bcf injection for the week ending July 30, which would measure 14 Bcf less than the five-year average. The following week shows an injection matching the five-year average build of 42 Bcf.

The week in progress has seen a continued rise in demand, far surpassing gains in supply and leaving markets tighter overall. Total supplies have risen by 500 MMcf/d on the week, led primarily by an uptick in net Canadian imports. Downstream, total demand is up 2.7 Bcf/d on the week, with lower industrial demand dragging down roughly 3 Bcf/d of gains from the power sector and 300 MMcf/d of gains in LNG feedgas demand.