03 Mar 2020 | 16:51 UTC — Insight Blog

Scrubbers bet pays off for shipowners as marine fuels spread remains wide

Last year, as the shipping and oil markets prepared for the onset of IMO 2020 regulations limiting sulfur emissions, expectations were that prices of high-sulfur fuel oil (HSFO) would fall while those for very low-sulfur fuel oil (VLSFO) would rise, as a result of changing demand.

At the start of 2020, the spread between 3.5% HSFO and 0.5% VLSFO was relatively wide, appearing to reward those shipowners that bet on scrubbers, or exhaust gas cleaning systems. This technology allows them to run the cheapest of all bunker fuels – HSFO – while still meeting IMO regulations.

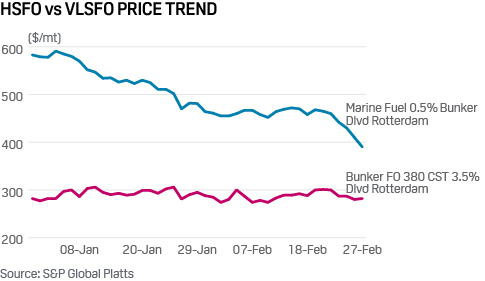

On February 28, the spread between the two types of fuel oil stood at $99/mt basis delivered Rotterdam, according to S&P Global Platts data, although there is variation between ports depending on the supply-demand balance.

However, the spread differential in Rotterdam has softened from highs at the start of January, raising questions about the soundness of the economic bet on scrubbers, and fuelling uncertainty for market participants. The spread between the two fuels dropped $82/mt, from $181/mt on February 3 to $99/mt on February 28.

The ‘scrubbers bet’

Ahead of the IMO 2020 deadline, shipowners faced three main choices to comply with the new 0.5% maximum share of sulphur exhaust in their bunker fuel.

The first option involved switching to marine fuels containing 0.5% sulfur content or less, and accepting higher fuel costs as well as variations in fuel properties, as suppliers released a plethora of blends onto the market.

The second was to retrofit scrubbers on their vessels, which would thus allow shipowners to continue burning high-sulphur bunkers.

The third was to switch to lower-carbon alternatives such as biofuels or LNG. This has not been widely adopted so far due to high costs of bunker and conversion to LNG, as well as a lack of infrastructure.

In essence, the choice has been between the first two alternatives for the majority of shipowners – i.e. VLSFO or scrubbers.

Compliance with the new regulation is expected to be significant, with approximately 10-20% of voyages expected to not be compliant in the first years following enactment. Part of the United Nations, the IMO has no enforcement power but delegates implementation to individual governments via annex VI of the MARPOL agreement of 1973.

While scrubbers allow charterers to run a vessel on cheaper fuel oil, a scrubber unit is priced between $2 million up to $6 million, depending on whether it is retrofitted or installed as part of a new build. In addition, a ship-owner would also consider the cost of dry-docking, which involves taking the ship out of the water to install scrubbers, the opportunity cost of having a vessel off the market, as well as ongoing maintenance costs and disposal of waste chemicals.

Clarksons estimates that 15% of crude tankers, measured by tonnage capacity had installed scrubbers by the beginning of 2020, and predict an increase to 19% by the end of 2020. The majority of scrubbers having been retrofitted on larger vessels due to economies of costs, the integrated shipping services company reports.

Vessel earnings

One indicator of the success of the “scrubber bet” is the amount that vessels with the cleaning units installed can earn for a voyage.

Oil tankers across both crude and refined products segments saw time charter equivalent earnings (TCEs) – the daily earnings on a given ship’s voyage – peaking in recent months for scrubber-fitted vessels, earning a premium compared to their non-fitted equivalent vessels.

For voyage charters on the spot market the shipowners bear the cost of fuel and will include it in the cost of the voyage, but when a tanker is on time-charter, the charterer will bear the responsibility of re-fuelling the ship if need be, and paying for the bunkers throughout their use of the tanker while on charter.

According to Svetlana Lobaciova from Gibson Research, premiums have ranged between $14,000 and $20,000 per day, depending on the ship’s characteristics and price of fuel on board. A spokesman for the scrubber company Clean Marine reported similar estimates on Monday as they assessed premiums at $18,000 per day on average on a VLCC.

Fleet conversion is continuing at an accelerated pace in the tankers market on the back of positive premiums. According to S&P Global Platts Analytics, roughly 17% of the tanker fleet will be fitted with scrubbers by the end of 2021.

On February 19, Scorpio Tankers announced strong fourth-quarter returns, especially for their scrubber-fitted vessels. The company plans to retrofit scrubbers on their entire fleet of 136 owned and bareboat chartered tankers. Currently, 55 scrubbers have been already installed.

A lasting trend?

As the spread differential in the bunkering hub of Rotterdam has softened from highs at the start of January, questions have been raised as to how the market will play out in the future. In fact, a spokesman from Clean Marine said premiums had slightly decreased from the previous weeks and closed lower last week.

Since January, 0.5% VLFO has fallen significantly, but 3.5% HSFO has remained fairly steady, leading to a 64% decline in the spread between the fuels at Rotterdam in just two months.

International shipping association BIMCO commented on the recent narrowing differential: “The price levels [between HSFO and VLSFO] are now declining towards a point of stabilization,” BIMCO’s Chief Shipping Analyst, Peter Sand said on January 24.

But given the newness of VLSFO, predictions regarding the point of stabilisation remain hypothesis. A surprising element has been the level of support that HSFO maintained following the IMO2020 launch. While demand for HSFO as a bunker fuel has been relatively low, strong HSFO crack margins as well as alternative uses for the fuel, have kept bunker prices for HSFO in Europe relatively supported compared to declines in crude oil.

Go deeper: Podcast - Post-IMO 2020, a rollercoaster ride for 0.5% marine fuels in Asia

The European benchmark crude grade, front-month ICE Brent futures, dropped over $15/b – equating to around $105 in metric tonnes – since the start of the year. HSFO bunkers in Rotterdam have dropped only $8/mt in the same time period.

This, along with a decline in 0.5% bunker prices, has been responsible for the narrowing spread between the two bunker fuels.

Weighing costs and benefits

Viewed in the longer term, the narrowing discount of HSFO may not yet be too problematic.

“Despite the lower spread, the investment payback period for a scrubber is between half a year to one and a half years, depending on the cost of the scrubber and daily consumption, which allows for substantial fuel oil cost savings for scrubber-fitted ships,” Sand noted in the BIMCO report.

A new element has surfaced in recent months that further differentiates vessels’ profitability in the current market, depending on the type of scrubber they have installed.

Certain areas have imposed restrictions on scrubber wash water discharge from open-loop scrubbers. For open-loop scrubbers, the most common ones for large vessels, water discharge is continuous throughout the vessel’s journey. Hybrid and closed-loop scrubbers, however, have the ability to store water on board in tankers and then discharge ashore.

“Often vessels use their open loop scrubber on the voyage and, when reaching a port with a ban on open loop scrubbers, they would switch fuels to VLSFO for that period,” a spokesman for Clean Marine said. “Ultimately, they are still making money on their investment. It takes a bit of planning to bunker a ship accordingly but it is being done.”

One area of interest is the Suez Canal, which has restricted open-loop exhaust gas cleaning systems until the ratification of MARPOL Annex VI by the Arab Republic of Egypt, said the Canal Authority in a circular January 15. However, this restriction only concerned the Canal, and will not be extended to all Egyptian waters.

At the start of January, delays in scrubber retrofits put strain on availability of 0.5% bunker fuel, especially in the Mediterranean, widening the spread between HSFO and VLSFO. The situation has since improved, with production facilities across the EMEA having slots with no delays according to a spokesman from scrubber company Clean Marine.

One exception is China, where the coronavirus outbreak has caused delays to increase. “As shipyard workers are unable to return to work, progress on scrubber fittings have stalled,” a China-based source said.