17 Feb 2021 | 11:30 UTC — Insight Blog

Insight from Moscow: Russia's strong economic position among OPEC+ members underpins its negotiating power

In early 2021 Russia secured an increase to its oil output quota under the OPEC+ agreement for February and March, the latest sign that Russia's comparatively strong economic position is allowing it to push for better terms under the deal.

Economics are set to underpin future negotiations in 2021, with Russia likely to continue to push to increase output volumes, despite uncertainty over demand.

Moscow-based analysts welcomed the latest OPEC+ decision, which allowed Russia to increase output by 65,000 b/d in February, and a further 65,000 b/d in March. Russia's crude output was 9.10 million b/d in December according to the S&P Global Platts OPEC+ production survey.

In contrast, most other members of the group will maintain output at January levels, with Saudi Arabia announcing that it would add an extra 1 million b/d cut. Russia's close ally Kazakhstan also secured a small increase to its quota from February.

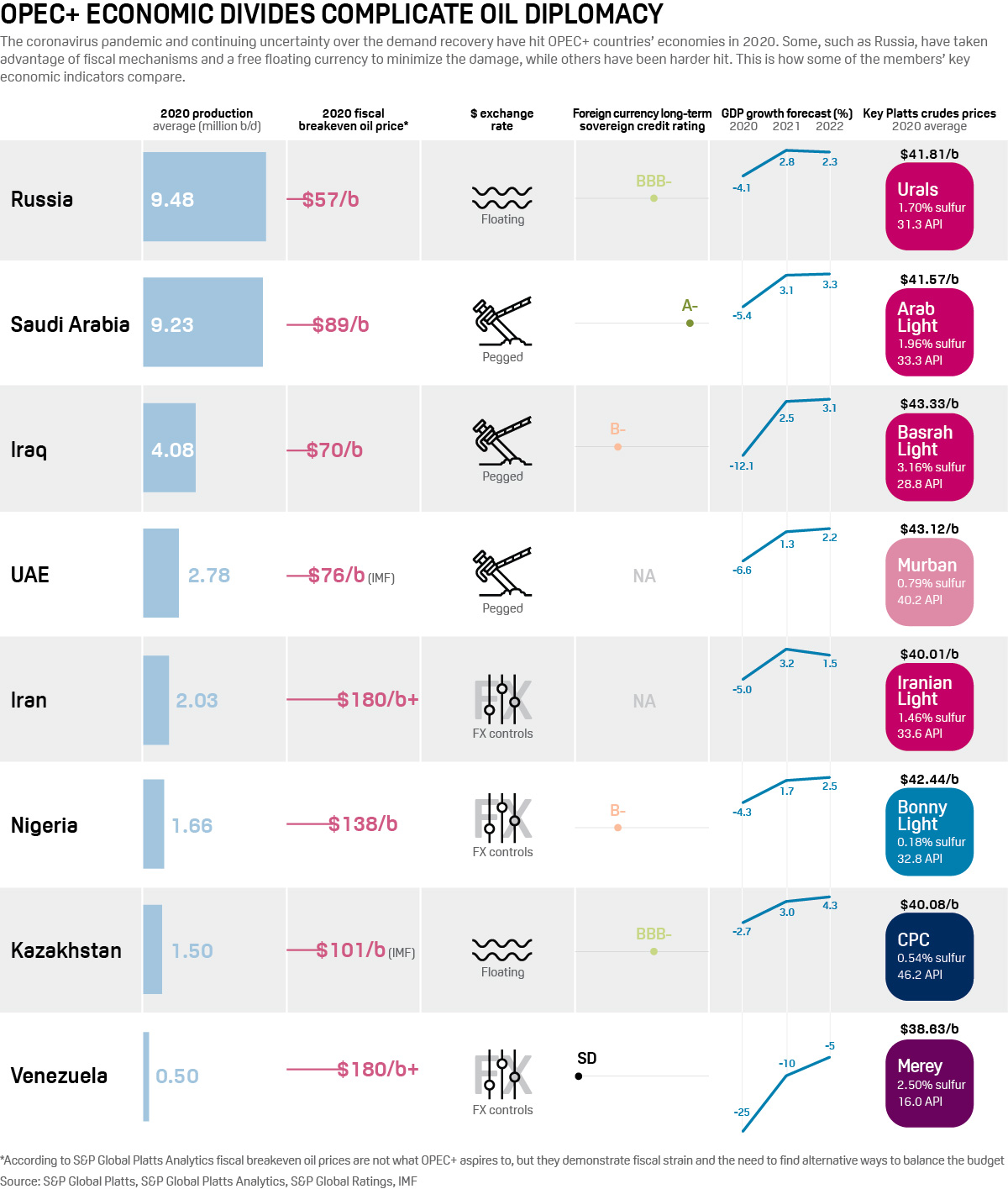

Russia is better able to absorb oil shocks than many of its OPEC+ allies, primarily because of its flexible exchange rate to the US dollar, the currency used to price its crude. The ruble's value tends to fall against the US dollar when oil prices drop. This allows Russian producers, whose costs are primarily in rubles, to minimize the impact of low prices on their operations.

On March 6, 2020 when Russia temporarily walked away from the OPEC + agreement, one dollar was worth 66.2 rubles. By February 16, 2021 the ruble had weakened to 73.31 against the US dollar, according to data from Russia's Central Bank.

Speaking after the January meeting where the new quotas were agreed, Russian deputy prime minister Alexander Novak said he hoped the outlook would be even more positive in two months' time, and there would be an option to further increase production.

Russia is aiming to bring back 2 million b/d of production compared to its December 2020 output level by June. Analysts at VTB Capital estimate that Russia's quota may increase further by some 80,000 b/d in April-June, if Russia is to achieve this aim.

Future policy

Uncertainty over the demand situation makes it hard to predict what may be on the table when the group next holds its full ministerial meeting on March 4.

Many countries continue to struggle with rising coronavirus cases and have tightened lockdown measures in recent months. While there is significant optimism around vaccines, there is also a lot of uncertainty over how quickly these can be rolled out, and when that will translate to a return to normal economic activity.

Even under negative demand forecasts, Russia is likely to remain in a comparatively strong economic position. As well as the flexible ruble-to-dollar exchange rate, the fiscal rule introduced in 2017 has reduced revenue volatility and softened the impact of oil price fluctuations on Russia's economy and budget.

Oil prices in early 2021 have so far been above those included in the Russian state budget. Approved late last year, the budget includes Urals oil prices of $45.3/b in 2021, $46.6/b in 2022, and $47.5/b in 2023.

Click to enlarge

Furthermore, Russia is pushing to reduce the state budget's reliance on oil and gas revenues, which has for decades left Russian oil producers exposed to significant changes in the tax regime during times of economic turbulence. Producers have frequently said that this complicates planning long-term development projects which require taxation stability to accurately evaluate costs.

Russian President Vladimir Putin said last year that hydrocarbons revenues will account for one third of all budget revenues in 2021, down from half in 2011.

In a positive demand scenario these factors are likely to underpin a bid to secure further production increases later in 2021. If the group faces a more negative scenario, requiring further cuts, Russia is likely to seek smaller cuts for shorter durations.

A lot is also likely to depend on US shale production volumes. The risk of losing market share to US producers has long been raised by Russian oil producers as a reason to be cautious in committing to significant crude output cuts.

Despite economic differences, and the likelihood of further disputes this year, analysts expect Russia to remain part of OPEC+, which President Vladimir Putin continues to support, and has become a key part of Russia's foreign strategy.