Metals & Mining, Non-Ferrous

July 06, 2026

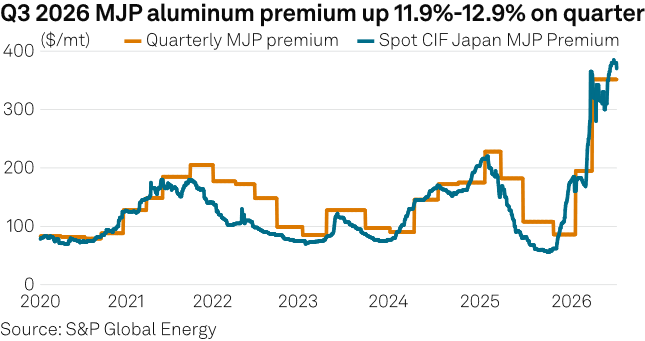

Japanese Q3 aluminum premium settles higher at $395/mt CIF Japan

By Yuxi Du

Editor:

HIGHLIGHTS

Q3 premiums gain 11.9%-12.9% from $350-$353/mt in Q2

10 trades with total minimum volume of 15,500/month concluded

Supply side uncertainty drives premiums to decades-high levels

Platts, part of S&P Global Energy, assessed the 2026 third-quarter premium for imported primary aluminum to Japan at $395/mt plus London Metal Exchange cash, CIF main Japanese ports, on July 6, up 11.9%-12.9% from $350-$353/mt in the second quarter.

The Q3 premiums were the highest quarterly premiums observed over the past decade. They were last higher for Q3 2014, at $404/mt CIF Japan.

The Q3 premium assessment was based on 10 trades concluded between July 3 and July 6. All deals were concluded at $395/mt with a total minimum volume of 15,500 mt/month, plus LME cash CIF Japan, for seaborne P1020/P1020A ingot for loading over July-September.

Offers throughout the negotiations ranged from $440-$480/mt CIF Japan. Initial Q3 MJP offers were heard at $480/mt CIF Japan on May 25 and $460/mt CIF Japan on May 26, respectively. The latest offer was at $440/mt CIF Japan, which was made on June 23 later expired on June 26.

Quarterly premium offer levels were initially elevated due to the limited availability of Good Western-origin tons following earlier supply disruptions.

"Buyers resisted price levels above $400/mt amid expectations of improving Middle Eastern supply," a Japanese trader source said.

Market sentiment shifted throughout the negotiation period. Several market participants said sellers gradually lowered offer levels as concerns over Middle Eastern supply disruptions eased and premiums in Europe and the US softened. Buyers, however, eventually agreed to premiums at $395/mt CIF Japan as they felt that a full recovery of Good Western-origin supply within the quarter was unlikely.

Weakening premiums in other regions also reduced buyers' willingness to accept significantly higher quarterly settlements. Platts assessed the Daily Aluminum Duty Unpaid IW Rotterdam Premium at $525-$560/mt on July 3, with a midpoint of $542.50/mt, down $70/mt from $600-$625/mt on May 13, with a midpoint of $612.50/mt.

The Platts US aluminum premium was assessed at 108.7 cents/lb plus LME cash, delivered Midwest, on July 3, down 10.35 cents/lb from 119.05 cents/lb on May 20.

Aluminum smelters in the Middle East were still operating below normal levels, while the timeline for restoring full production and export volumes remained uncertain. Emirates Global Aluminium said July 2 that production at its Al Taweelah smelter was being restored faster than initially anticipated following recent disruptions. However, the producer added that hot metal production could take up to one year to return to pre-disruption levels.

In addition, market participants noted that the LME aluminum market structure remained predominantly in backwardation during much of the negotiation period. Narrower backwardations and occasional contangoes were short-lived; traders generally showed limited interest in carrying forward cargoes. Expectations of continued Good Western-origin supply tightness outweighed any support provided by the market structure, keeping spot availability constrained.

On the demand side in Asia, particularly Japan, market participants reported largely stable year-over-year consumption, with no significant improvement in end-user demand.

Port stocks at the main Japanese ports at the end of May stood at 238,000 mt, down 4.60% month over month and 28.10% year over year. The May 2026 main Japanese port stock levels were the lowest observed since February 2012 at 237,200 mt.

Several market participants said the decline in port stocks reflected both reduced arrivals and inventory management strategies adopted by Japanese trading houses in response to the backwardated LME structure.

Some market participants remained cautious regarding long-term sustainability of current premium levels, expecting premiums to ease in Q4 as Middle Eastern production and export flows normalize.

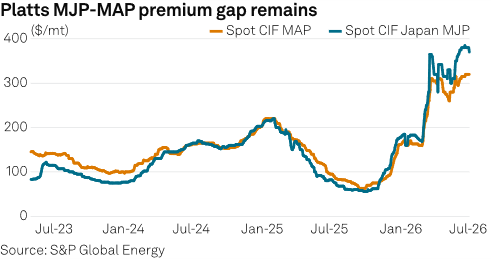

Market participants also pointed to a widening divergence between the CIF Main Asian Ports (MAP) and MJP markets.

Platts assessed the CIF main Asian ports (MAP) spot P1020 aluminum premium at $320/mt plus London Metal Exchange cash July 6, unchanged day over day.

Elsewhere in Asia, spot buying interest remained mixed. While some consumers sought replacement units amid cost advantages and limited availability of Good Western-origin tons, others remained on the sidelines due to elevated outright aluminum prices.

Market participants continued to monitor ramp-ups at Xinfa's electrolytic aluminum project and PT Kalimantan Aluminum Industry, as well as increasing export availability from India.

"Alternative tons are available, but not all Japanese consumers can switch immediately," a regional trader said. Japanese buyers continued to show a preference for Good Western-origin material, limiting the impact of additional regional supply on quarterly negotiations.

The Platts CIF Japan spot premium for 99.7% P1020/P1020A aluminum ingot was assessed at $370/mt plus London Metal Exchange cash, CIF Japan on July. 06, unchanged day over day.

Platts specifications are for all quarterly settlements on a CIF main Japanese port basis, negotiated before the quarter between two unaffiliated counterparties, for P1020/P1020A 99.7% primary aluminum ingot, with payment in cash against documents, for volumes of 500 mt/month or more under annual frame contracts.