Fertilizers, Chemicals, Energy Transition, Agriculture, Maritime & Shipping, Renewables, Biofuels, Grains, Dairy, Meat, Sugar, Vegetable Oils

April 03, 2026

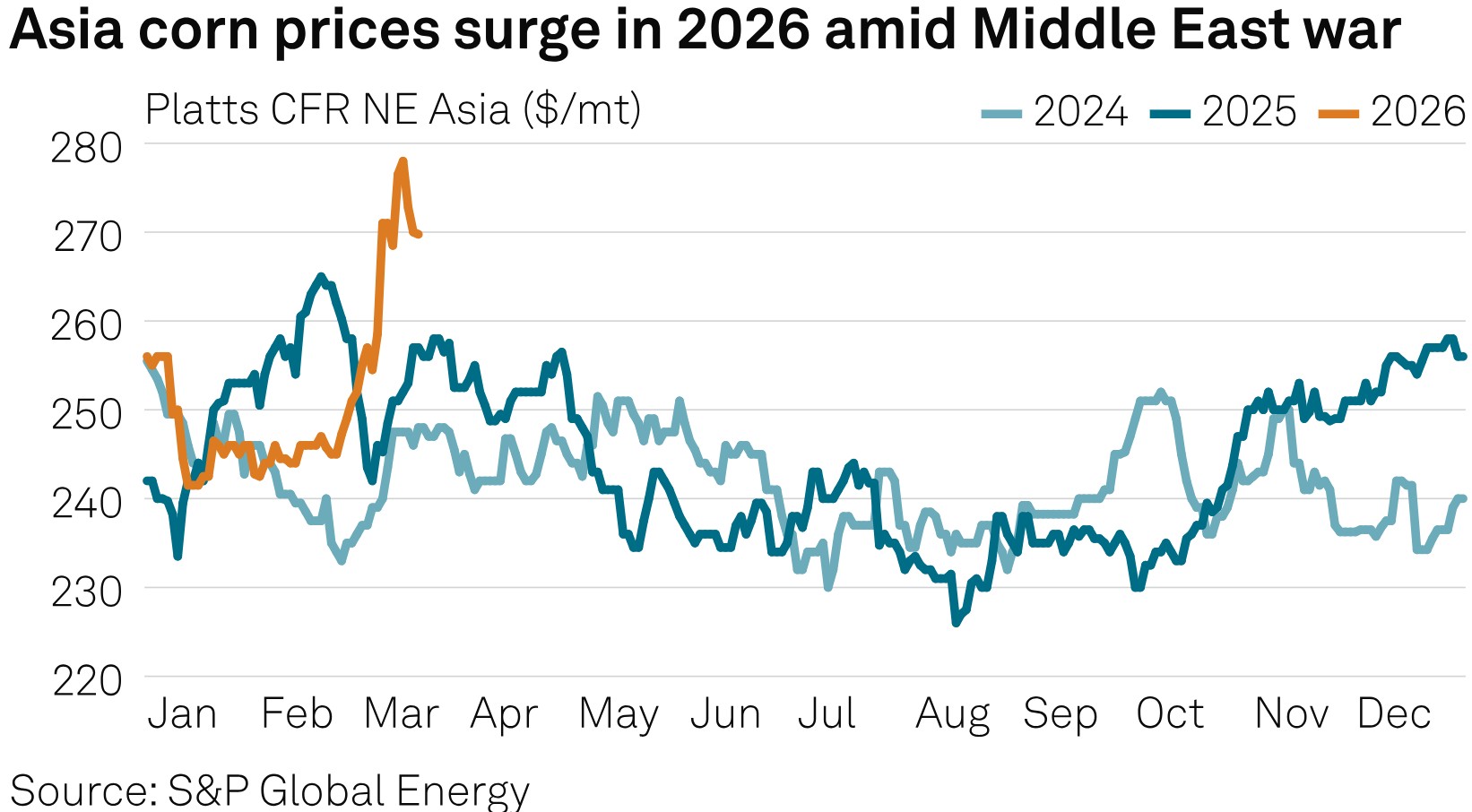

Global food prices rise in March across basket amid Middle East energy shocks

Editor:

HIGHLIGHTS

Global food prices rise 2.4% MOM in March

Energy shock drives vegetable oil, sugar higher

Middle East conflict disrupts fertilizer supply

Global food prices rose for the second consecutive month in March, with energy-driven cost pressures linked to the escalating Middle East conflict feeding through into vegetable oil and sugar markets, according to the Food and Agriculture Organization April 3.

The FAO Food Price Index averaged 128.5 points in March, up 2.4% month over month, as all major commodity groups, including cereals, meat, dairy, vegetable oils and sugar, posted gains.

This marked its highest level since December. The index was also 1% higher year over year, though still nearly 20% below its March 2022 peak.

All major commodity groups posted gains, reflecting both underlying supply-demand fundamentals and rising input costs tied to higher energy prices and freight disruptions.

The increase reflects a broadening transmission of higher crude oil and freight costs into agricultural markets, reinforcing concerns that the ongoing energy shock is evolving into a wider food inflation cycle.

Energy-agriculture link strengthens

The strongest upward pressure came from vegetable oils and sugar -- two markets most directly exposed to energy price dynamics.

The FAO Vegetable Oil Price Index rose 5.1% month over month, with palm oil prices rising to their highest level since mid-2022.

The rally was driven in part by spillover from higher crude prices, which lifted biofuel demand expectations and tightened feedstock availability.

The FAO Sugar Price Index averaged 92.4 points in March, up 6.2 points (7.2%) from February, reaching its highest level since November 2025, supported by expectations that Brazil -- the world's largest sugar exporter -- could divert more cane toward ethanol production as fuel prices rise.

This biofuel linkage is emerging as a key transmission channel, with higher energy prices incentivizing the use of agricultural commodities for fuel, thereby tightening food supply balances, according to a Brazil-based ethanol producer.

Cereals, meat rise

Cereal prices rose more modestly, with the FAO index up 1.5% month over month. Wheat prices increased by 4.3%, supported by drought concerns in the US and expectations of reduced plantings in Australia due to higher fertilizer costs.

Corn prices edged higher, supported by improved ethanol demand prospects and concerns about fertilizer affordability ahead of the Northern Hemisphere planting season.

In protein markets, the FAO Meat Price Index rose 1%, led by higher pig meat prices in the EU amid seasonal demand.

Dairy prices also posted their first increase since July 2025, rising 1.2% on the back of tightening milk supply in Oceania and firm import demand.

Conflict-driven cost push

The price gains come as disruptions linked to the Middle East conflict ripple across energy, fertilizer and logistics chains, raising input costs across the agricultural sector.

According to FAO Chief Economist Maximo Torero, the conflict represents a "systemic shock" affecting not just energy markets but the entire agrifood system, particularly through fertilizer supply disruptions and higher transport costs.

The Strait of Hormuz, a critical artery for global energy and fertilizer trade, handles about 30% of global urea exports and significant volumes of ammonia and phosphates, making it a key chokepoint for agricultural inputs, according to the FAO.

Fertilizer prices have already surged, with FAO warning that global prices could average 15%-20% higher in the first half of 2026 if disruptions persist.

Outlook hinges on duration of disruption

Despite the recent gains, the FAO index remains nearly 20% below its March 2022 peak, suggesting markets are not yet in full crisis mode.

However, the trajectory will depend heavily on the duration of the disruption.

In a short-term scenario, global food stocks remain sufficient to absorb shocks. But a prolonged conflict could begin to affect planting decisions, reduce fertilizer application, and ultimately lower crop yields -- tightening supply and amplifying price pressures into 2026.

The latest data underscores a familiar but intensifying dynamic: as energy markets tighten, the knock-on effects are increasingly visible across food systems, raising the risk of renewed global food inflation.