LNG, Natural Gas, Metals & Mining, Agriculture

May 19, 2026

COMMODITY TRACKER: 5 charts to watch this week

By Staff

Editor:

Northwest Europe LNG prices strengthened on geopolitical tensions and seasonal injection demand, while US natural gas consumption is forecast to reach record levels this summer. LME copper and aluminum rose on falling inventories, Canadian wheat premiums hit a 10-month high, and India banned sugar exports through September.

1. Northwest Europe LNG premium to Henry Hub widens

What's happening? The DES Northwest Europe LNG premium to Henry Hub widened to a five-week high, as NWE LNG prices reached a month high. Platts, part of S&P Global Energy, assessed the delivered ex-ship Northwest Europe marker for June at $16.696/MMBtu on May 15, at a discount of 26.50 cents/MMBtu to the June TTF hub futures price. This placed the Northwest European marker for June at its highest price since April 7, when Platts assessed DES NWE marker at $17.327/MMBtu. Platts assessed the spread between DES NWE LNG and Henry Hub at $13.736/MMBtu, up 56.60 cents day over day. EU gas storage stood at 36.14% of capacity as of May 15, down 7.74 percentage points year over year.

What's next? Geopolitical tensions in the Middle East continued to support risk sentiment, increasing interbasin competition for LNG cargoes between Europe and Asia. Injection season in Europe added further support to NWE LNG prices, as gas storage levels remained below year-on-year levels. Seasonal maintenance across US LNG export facilities lowered available cargo flows, with Freeport LNG in Texas taking one liquefaction train offline for several weeks. Market sources anticipated that the arbitrage economy would flip back to Europe in August or September, as European countries need to fill gas tankers ahead of winter.

2. US natural gas demand to hit record high

What's happening? US natural gas demand is forecast to reach a record 108.7 billion cubic feet/day this summer, a 6.3% increase over summer 2025, according to the Natural Gas Supply Association's Summer 2026 Natural Gas Market Outlook released May 13. US gas production is also projected to hit a record high, rising 4.4 Bcf/d year over year to 117 Bcf/d, driven by a 4.9 Bcf/d increase from the Permian and Marcellus regions. Natural gas storage is projected to enter summer near 1.9 trillion cubic feet, almost 5% above the five-year average.

What's next? LNG exports are expected to lead US gas demand growth, rising from 15.6 Bcf/d in summer 2025 to about 20 Bcf/d by the end of 2026 as new liquefaction capacity comes online. Power generation and industrial uses are expected to increase overall gas demand by about 2.47 Bcf/d, driven by rising data center loads. End-of-summer injection inventories are expected to finish near 3.7 Tcf, slightly below average. The outlook forecasts this summer will be 4.8% cooler than last summer, which could reduce gas demand and result in flatter prices.

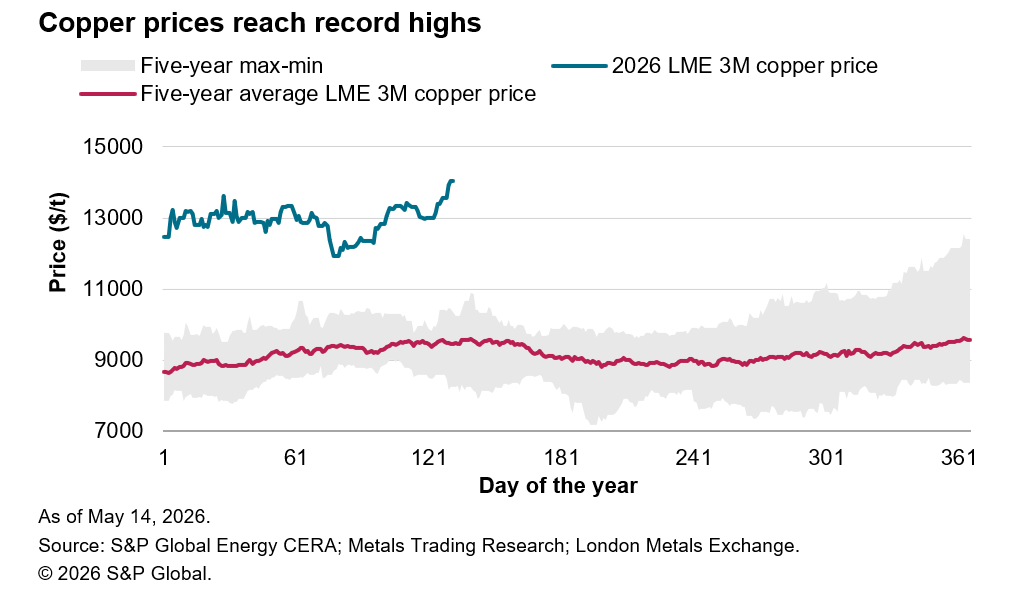

3. LME copper prices climb on falling stocks

What's happening? London Metal Exchange copper cash prices rose to $13,986/mt at the May 14 close, up $541/mt from $13,445/mt on May 8, as stocks fell to 397,050 mt, down 2,350 mt week over week, exchange data showed May 15. Platts assessed clean copper concentrate CIF China at $3,825/mt on May 14, down $45/mt day over day. Platts assessed Chinese copper import premiums at $70/mt plus LME cash, CIF China, on May 13, up $5/mt from May 6. LME aluminum inventories fell 9,275 mt week over week to 346,500 mt on May 14, with the cash settlement price at $3,768/mt, up $207.50/mt from May 8, according to exchange data. LME nickel stocks declined 2,010 mt to 275,778 mt, with the cash settlement price at $18,915/mt, up $25/mt week over week.

What's next? Aluminum showed the sharpest stock draw and strongest near-term supply tightness, with inventories down 162,775 mt from the year-to-date high of 509,275 mt recorded on Jan. 22. At the May 14 close, cash aluminum traded at a $102/mt premium to the three-month price of $3,666/mt, indicating a backward market structure, exchange data showed. Copper inventories remained elevated near the year-to-date high despite sharp price rallies, with the three-month price at $14,034/mt trading at a $48/mt premium over cash, indicating a contango market structure. Nickel's contango points to less immediate supply stress, but stocks remain 13,728 mt below the Feb. 26 year-to-date high, which should continue to underpin prices if the inventory decline extends.

4. Canadian wheat premium hits 10-month high

What's happening? The spread between the Platts Milling Wheat Marker and Canadian Western Red Spring wheat widened to a 10-month high of $51/mt on May 12, driven by futures volatility and currency weakness. Platts last assessed CWRS at $280.17/mt and the MWM at $241/mt on May 14. Canadian wheat rose to $289.54/mt on May 12, its highest since June 2025. The July MIAX hard red spring wheat futures contract rallied 37.50 cents/bushel following bearish US Department of Agriculture supply estimates that cut the US wheat production forecast by 425 million bushels.

What's next? Poor drought conditions and winter wheat quality concerns in the US have supported wheat futures since April, with the May 11 USDA Crop Progress report showing 40% of winter wheat rated poor to very poor condition. Strong Canadian wheat export demand continues to underpin prices, with year-to-date exports totaling 17.46 million mt for the week ended May 10, compared with 16.8 million mt the previous year. Selective producer selling is also supporting CWRS prices as growers await better pricing opportunities.

Listen: Global wheat markets on edge as war, weather, fertilizer shocks drive new rally

5. India bans sugar exports through September

What's happening? India imposed an immediate ban on sugar exports through Sept. 30, effective May 13, after changing the export policy from "restricted" to "prohibited," according to the Directorate General of Foreign Trade. The ban exempts exports under EU and US quotas, government-to-government sales, and shipments already in the physical export pipeline where loading began before May 13. March NY11 sugar futures settled at 14.99 cents/lb on May 14, up 3.09% from May 7. Platts assessed hydrous ethanol ex-mill in Ribeirao Preto, converted to a raw sugar equivalent, at 13.73 cents/lb on May 18. The move reflects concerns that Indian sugar production could fall short of domestic consumption for a second consecutive year due to weaker sugarcane yields in key producing states Maharashtra, Karnataka, and Uttar Pradesh.

What's next? A Singapore-based sugar trader said the market expected India to export 600,000-700,000 mt of white sugar post-ban, down from earlier estimates of 700,000-800,000 mt. A second Singapore-based trader said export demand remains limited, with Brazil's surplus in the raw sugar market remaining the bigger driver of prices. An Indian exporter said global price direction still depends largely on the Brazilian crop, and some demand might shift to Thailand. Platts assessed the FOB premium for Thai HiPol raw sugar spot June shipment at 112 points over ICE New York No. 11 July 2026 futures on May 14, unchanged week over week. Strong supply from Brazil and Thailand is expected to fill the gap and limit sustained price impact.

Reporting and analysis by Clio Ho, Parker Leipzig, Shivam Prakash, Maham Quadri, Vivian Iroanya, Samyak Pandey, Muskan Agarwal and Grace Tan.