25 Aug 2021 | 10:15 UTC — Insight Blog

30 years on: How the collapse of the Soviet Union transformed Russia into a global oil and gas powerhouse

It has been 30 years since the collapse of the Soviet Union transformed global energy markets and set Russia on a pathway to gaining a seat at the OPEC table along with tremendous pricing power over oil and natural gas.

The world's largest exporter of crude and gas to Europe has grown its influence from the shattered remnants of the communist bloc when the future of its energy sector looked in doubt. A year after the period leading to Russia's democratization known as "Perestroika" the country's share of the global oil markets was a fraction of the 12% it currently holds.

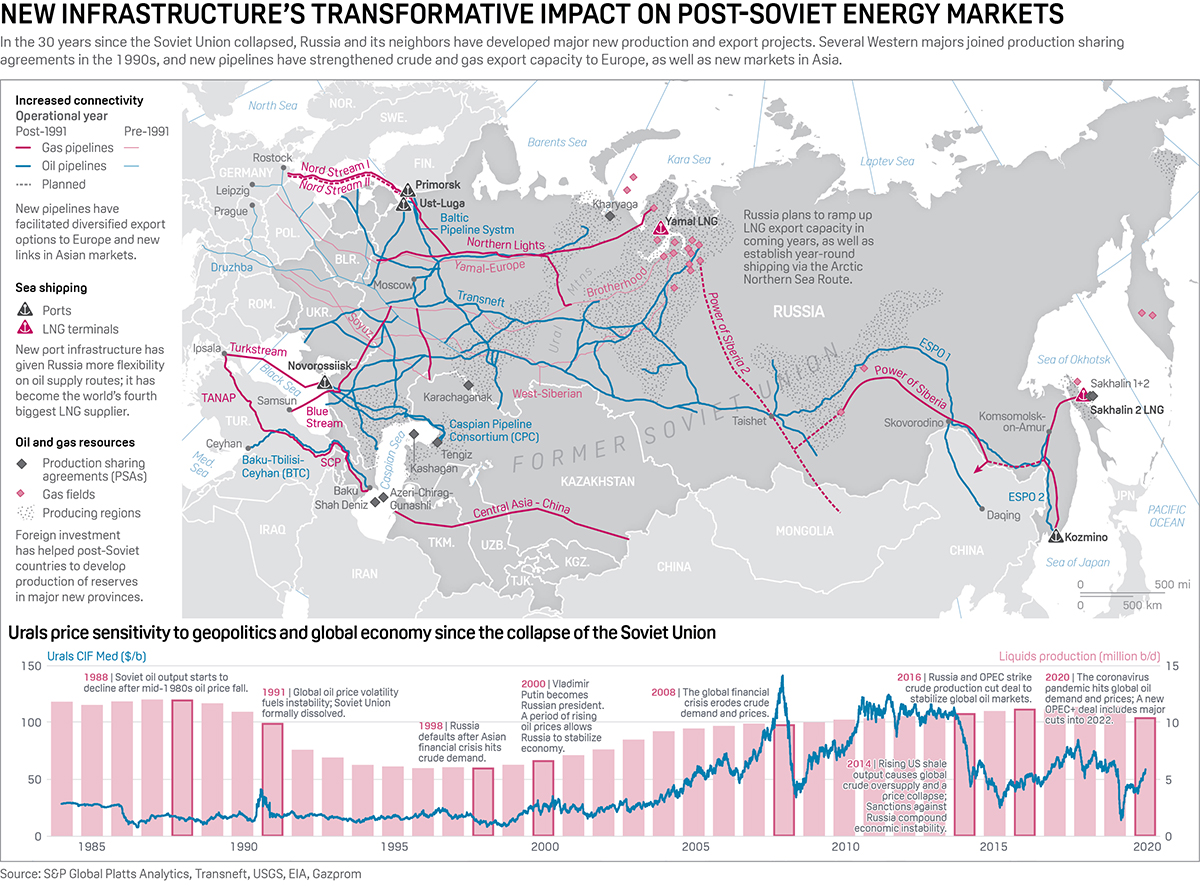

"Turbulence in the immediate aftermath of the Soviet Union's dissolution caused the region's crude and condensate supply to fall by 4.2 million b/d between 1990 and 1994 alone," said Paul Sheldon, chief geopolitical adviser at S&P Global Platts Analytics. Today, Russia produces around 9.64 mil b/d, according to the Platts OPEC Survey for July, and Platts assessed Russia's key crude grade Urals CIF Med at $68.145/b on Aug. 25.

At the beginning of January 1984, Platts assessed Russia's key crude grade Urals CIF Med at $28.55/b. On Jan. 31, 1986, prices fell to $19.95/b and remained below $22/b until August 1990, when global prices rose sharply following Iraq's invasion of Kuwait.

"The oil glut of the 1980s, which followed the 1979 oil price shock, was a direct contributor to the collapse of the Soviet Union in 1991. The USSR had just before that become a major global oil producer; lower prices immediately resulted in a substantial loss of hard-currency export revenue, forcing the USSR to deplete its official reserves amid growing deficits of almost everything across the union," said George Voloshin, head of the Paris branch of Aperio Intelligence.

Private investment

This new economic and political reality also created fresh opportunities. Privatization of oil and gas assets allowed foreign investors to enter post-Soviet markets and introduce cutting edge technology to production sites. They also helped to expand the geographical scope of Russian production through new projects developed in eastern Russia, including offshore Sakhalin, as well as in the far north of the country.

"Subsequent periods of Russian oil company privatization ultimately triggered more focused investment, increased efficiencies and technological advances, all of which paved the way for nearly unabated production growth since 1998," Sheldon from Platts Analytics added.

Other former Soviet states have followed similar policies.

"Outside of Russia, landmark foreign investment deals in Kazakhstan and Azerbaijan continue to bear fruit, helping to lift total FSU production by over 7 million b/d between 1998 and 2019, before OPEC+ cuts caused a rare drop in 2020," Sheldon said.

Export options

Foreign investment has also enabled oil and gas producers to develop new infrastructure projects, transforming the customer base for the region's oil and gas.

"The emergence of new export infrastructure, in addition to the Druzhba oil pipeline which was built in the 1960s, has contributed to the expansion of oil producing areas within Russia," Aperio's Voloshin said.

Key new projects include the Eastern Siberia-Pacific Ocean oil pipeline commissioned in 2009 to export to China and the broader Asia-Pacific region. The Baltic Transport system increased export capacity from projects in the Volga Urals and West Siberia as well as northern Russia. In recent years, the government has prioritized development of oil and LNG shipping via the Northern Sea route, which supplies Europe and Asia through Arctic waters.

"I look at how Putin was able to become friends with China and to send more oil to the east and especially start sending more gas to the east and in the Arctic, you look at what's happening on Yamal, you look at what's happening on the second Arctic project, there's going to be a lot of gas flowing to the east and that's going to be in direct competition with Qatar and Australia," independent economist and energy adviser Cornelia Meyer said.

However, more exports and the battle for market share have led to some problems, particularly over Europe's reliance on imports of gas from Russia as well as the influence the Kremlin has on countries that transit Russian gas to Europe. New export infrastructure has also been a key target for US sanctions introduced in 2014 over Russia's role in the conflict in Ukraine.

Economic resilience

Russia's dependence on oil and gas revenues has also evolved over the past 30 years. In 1998, a drop in oil demand sparked by the Asian financial crisis led Russia to default and the ruble to significantly devalue.

From 2000, when Vladimir Putin became Russia's president, a steady rise in oil prices allowed the Kremlin to pay off large amounts of foreign debt and establish a stabilization fund as protection against price volatility. This mitigated the impact of the global financial crisis in 2008 and has helped the country cope with subsequent price volatility, including the impact of growing US shale output since the mid-2010s.

In recent years, Russia's improved budget resilience has allowed it to bargain for increased output volumes within the OPEC+ agreement, as many other members of the coalition's state budgets are more sensitive to oil price volatility.

As the region marks 30 years since the collapse of the Soviet Union, these trends continue to drive political and commercial priorities. The energy transition will add an extra dimension, as producers attempt to balance plans for new hydrocarbons production and export projects with growing concerns about the environment and the increasingly evident impact of climate change.