28 Apr 2020 | 21:46 UTC — Insight Blog

Cushing WTI price rout leaves US crude benchmark reeling: Fuel for Thought

The oil hub of Cushing, Oklahoma, has overcome times of stress before without losing its prime role in US oil pricing.

But when it made history on April 20 with a headlong dive into negative pricing, the potential difficulties of using it as a pricing benchmark for oil trade in other US markets and beyond was highlighted like never before.

It’s not unheard of for commodities to trade at negative prices, but for it to happen to crude at Cushing is exceptional. Negative prices have been seen only rarely (and not usually for long), with examples from recent years including cases such as associated gas in far western Texas or even very light natural gas liquids in Western Canada .

In both cases, the commodity in question was an unwanted byproduct alongside more valuable crude oil, and on the whole had to be sold even at a negative price in order to keep the more valuable oil flowing.

But this is not what happened at Cushing. This was the benchmark itself, the commodity that was supposed to be the valuable thing, plunging way below zero to settle at an unprecedented minus $37.63/barrel.

Cushing is something of an outlier among the major oil benchmarks, as it is not particularly close to either major production or consumption areas. What it does have is a lot of physical infrastructure, with a wealth of pipeline connections and a commercial crude storage capacity that is unrivaled.

By comparison, North Sea Brent crude, widely used as a benchmark in Europe and in markets around the world, is based on trade in physical waterborne cargoes of five different crude grades. While Brent's nominal storage capacity is lower than WTI at Cushing, it is intrinsically linked to the global market, with the crude making up the Dated Brent benchmark easily deliverable by tanker to refiners in any continent.

WTI price and differentials

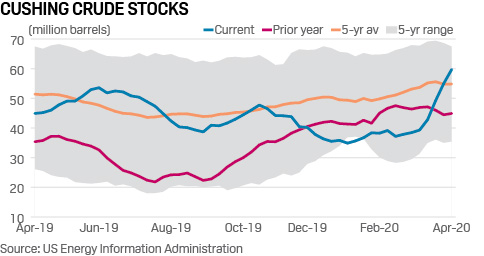

Cushing lacks this easy access to the global market, so if you buy oil, you need a storage tank to put it in, and for several weeks now, that storage has been getting steadily fuller.

There is still free tank space at Cushing, but it’s not necessarily available to anyone needing it on the open market. The scale and speed of the precipitous drop in oil demand has left the market incredibly oversupplied, and despite the best efforts of producing countries, that oversupply is weighing heavily on prices.

This played out in extremis on April 20, when anyone needing to sell May WTI crude found there were no buyers left in the market until they chased them all the way down into negative territory - market forces, turned up to 11.

WTI crude at Cushing is one of the most-watched and most-referenced crude prices in the world. Traders of other physical crude grades in other locations, notably the major US Gulf Coast market built around Texas and Louisiana, typically buy and sell oil at a differential to Cushing.

In normal times one could argue this serves them well, with these differential markets reflecting the Gulf Coast fundamentals of a specific grade while the link to Cushing ensures that the final price reflects the overall value of the oil. In this way, they rely on Cushing to act as a general barometer for world oil prices and fine-tune the price via the differentials.

But this mechanism breaks down when the reference price at its heart behaves as it did on April 20.

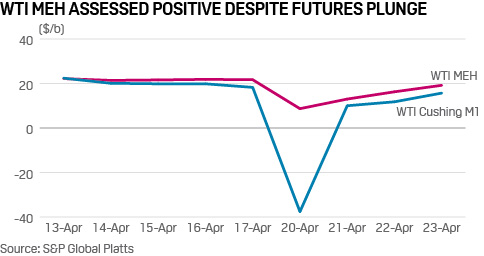

In normal times, a seller willing to offer Midland grade crude oil at the Magellan East Houston terminal might do so at a premium of a few dollars to Cushing. In fact, earlier the same day before the May contract went into free fall, there was trade reported in this MEH market at May WTI plus $7/barrel.

But what does that mean when Cushing then crashes into negative territory and settles where it did at minus $37.63/barrel? Is MEH crude in Houston really only worth $7 more than this, which would still be below minus $30/barrel?

Similar questions had to be asked about the market value of other Gulf Coast grades such as Mars or LLS, WTI cargoes being traded for export, or even crude oil loading in Latin America.

Go deeper: Explore crude grades with S&P Global Platts Periodic Table of Oil

Everything is pretty weak right now, sure, but that did not mean everything was going to march down in lockstep with the May Cushing contract. Other major benchmarks such as Platts Dubai and Dated Brent , for example, show no signs yet of falling into negative territory.

In its crude oil price assessments, S&P Global Platts judged there was no evidence that crude prices on the Gulf Coast were also in negative territory, as Cushing indisputably was. The core purpose of a price assessment is to reflect market value, and on the Gulf Coast those values for MEH, Mars and other crudes were still positive.

Negative pricing and the end-user

One big problem for US traders now is how to price their crude if they cannot rely on prompt Cushing prices as a stable benchmark.

Do they move to a further-forward Calendar Month Average WTI pricing basis such as that used in Canada, to try and avoid the dependency on a contract getting close to expiry? Or perhaps switch to a different benchmark altogether like Brent, which history has proven to be a more reliable bellwether for the global oil complex as a whole.

Riding out the storm and hoping that the extreme volatility is not repeated next month is always an option, although it is worth noting that June WTI also faced some pressure in the aftermath of the astonishing movements in the May contract.

With the oil market reeling from the impact of coronavirus pandemic, perhaps the last thing US traders wanted was a fundamental doubt to emerge over their preferred pricing benchmark.

But that’s exactly what they’ve now got.

The May WTI episode is also a big wake-up call. Negative pricing is not just theoretical, it has actually happened and could happen again in major commodity markets if the right circumstances combine.

That doesn’t mean negative pricing would necessarily fan out from a benchmark to all corners of the market, and it’s even less likely that we could see them reaching all the way to the end-user.

Don’t forget, a lot of the world’s oil is owned directly by the countries where the reservoirs are located and is not necessarily sold on a free-market basis. In most of these cases, a state oil company or other arm of the state has a primary goal of maximizing revenues for the state through the sale of its natural resources.

Can you really envisage that state oil company – whether Saudi Aramco , Pemex or any of the scores of others – authorizing a buyer to fill up a tanker with crude and be paid for the pleasure?

And what about all of us , the individual consumers of oil products in myriad ways?

Well, suppose that benchmark gasoline prices in a market like Houston turned negative. Do you think it’s remotely possible that your local gas station will pay you money to drive up and fill your tank? You could forget all about social distancing, there would be a line a mile long.

In its crude oil price assessments, S&P Global Platts judged that there was no evidence that crude prices on the Gulf Coast were also in negative territory, as Cushing indisputably was.

One big problem for US traders now is how to price their crude if they cannot rely on prompt Cushing prices as a stable benchmark.

Fuel for Thought is a weekly column published first in S&P Global Platts Oilgram News