08 Jul 2020 | 12:15 UTC — Insight Blog

European steel industry looks for way forward amid coronavirus demand blow

By Annalisa Villa and Laura Varriale

The coronavirus has dealt the European steel sector a heavy blow. Coming on the heels of Brexit and global trade tensions, the crisis has also highlighted the region’s overcapacity problem, raising the possibility of previous merger and divestment plans being revived.

As much as 18.9 million mt of steelmaking capacity was taken offline in Europe during the market slump caused by the pandemic – more than in any other region. This comes on top of 2019’s marginal contraction in production.

By mid-May, steelmakers across Europe had restarted production, but the industry faced an unprecedented situation as the sector organization Eurofer was unable to offer a production outlook, while mills still had very little clarity about their order bookings.

The collapse in demand brought about by widespread lockdowns is not the only worry for steelmakers. The current global health crisis may have pushed Brexit to one side, but the issue is resurfacing as the end of the transition period looms. Competition from imports continues to pressure the domestic industry, spurring yet another EU antidumping investigation on top of a raft of measures over the last few years.

The prospects for the EU construction and automotive sectors, the steel industry’s main buyers, have both taken a massive hit, with lockdowns resulting in closures of construction sites, particularly for civil engineering projects.

In March, the automotive sector shut down almost completely all over Europe, with very few exceptions. In light of the major economic crisis facing the auto industry, the European Automobile Manufacturers’ Association radically revised its 2020 forecast for passenger car registrations to a drop of 25% year on year, on 23 June. That means the body expects car sales in the European Union to tumble by more than 3 million units to some 9.6 million units this year.

Following the first shockwaves of the crisis between mid-March and May, the EU market has contracted by 41.5% so far this year. This situation is expected to ease to a certain extent in the coming months as lockdown and containment measures are lifted throughout the region. However, some EU countries have explicitly planned to restart public construction projects as quickly as possible to use it as a countercyclical tool during the unprecedented economic downturn. Meanwhile, steelmakers, as well as other industries, have sought government funds to keep afloat.

A slow restart

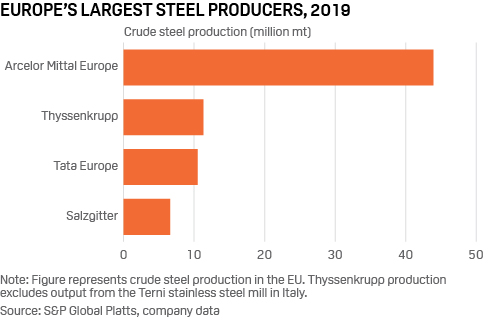

In Germany, the EU’s biggest producer of steel, restarts are proceeding even more slowly. Steelmaker Thyssenkrupp said it expected a production cut of 20%-30% of its capacity to last into the summer, and Salzgitter plans to continue with reduced production amid a gloomy outlook for the rest of the year.

With 39.7 million mt of crude steel produced in 2019, Germany saw crude steel output fall 10% on year in the first quarter, with year-on-year falls also likely over the summer.

Italy, the EU’s second largest steelmaker with 23 million mt crude steel production last year, was the first to officially restart steel production from late April. Italian crude steel production in May went down by 43.6% to 1.25 million mt, according to official data released by worldsteel on 22 June, and industry sources said that mills were continuing to run at low capacity.

In their first-quarter earnings calls, steel mills forecast very low production and profit for Q2, while for the first time they were not able to give a full Q3 and Q4 outlook. The overriding message was that balance sheets would continue to worsen as the recovery in demand is expected to be slow, and a return to pre-pandemic levels is not expected until the end of this year.

“We saw a slow restart of the mills but I am not confident production will bounce back any time soon and I think that we will also soon see some re-closures due to low order intake. I would not be surprised if we saw earlier and longer summer stoppages this year”, a senior industry source told S&P Global Platts.

The World Steel Association (worldsteel) said June 4 it expects global demand to fall by 6.4% to 1.65 billion mt of steel in 2020. While a recovery is underway in China, and steel demand is forecast to grow 1% this year, worldsteel expected steel markets in Europe, North America, India and other Asian economies to take longer to rebound.

Read more features on metals and mining in the latest edition of Insight magazine

For the EU 28 countries, worldsteel forecast a 15.8% drop in steel demand in 2020, followed by a 10.4% increase in 2021. The outlook was echoed by European steel industry association Eurofer, which said in its latest report that it did not expect market conditions to improve before Q4 or early 2021, although much would depend on the length of the lockdown in downstream sectors.

Significantly, due to the unprecedented nature of the disruption caused by the pandemic, Eurofer said it would temporarily not publish quantitative forecasts for 2020 and 2021. “Uncertainty and volatility surrounding possible developments in the coming months means no forecast could be considered reliable,” the association said.

The consequences of the coronavirus-related shutdown for industrial activity stretch far beyond Europe, Eurofer stressed.

“They have reached a global scale, in terms of huge disruption to supply chains and supplies of input and raw materials. This will probably have unprecedented repercussions on output in Q2 and Q3 of 2020. Against this background, a substantial rebound is not in sight before Q1 2021.” The early demand and output data for this year shows the dramatic impact of coronavirus, but in in 2019 there were already signs the steel market was struggling. Business conditions deteriorated, with the trend accelerating in the second half, particularly in the automotive industry, although the construction sector continued to outperform other major steelconsuming sectors.

Total output in steel-using sectors fell by 1.6% in Q4 2019, after 0.4% growth in Q3. For the whole of 2019, total output eased back 0.2% year on year compared with growth of 2.9% in 2018, Eurofer said.

According to European steel producers, even after the end of the pandemic, external risks will continue to cast a shadow over steel-consuming industrial sectors into 2021, and will likely hamper investment. The possibility of a no-deal Brexit – as the final agreement with the EU must be reached before the end of 2020 – continues to generate uncertainty, while a new escalation in protectionist trade measures would contribute to a sustained bearish outlook.

Resurgent trade tensions

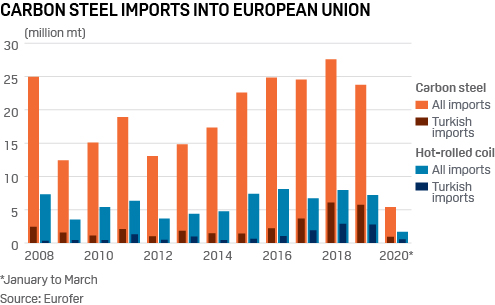

The EU has been tightening import restrictions over the past few years as protectionism in global trade has increased. Safeguard quotas on steel imports were imposed in addition to existing anti-dumping duties in 2018 in response to the US government’s protectionist measures and the fear of redirected imports into the EU.

With domestic demand for steel still weak, European mills have been seeking extra support from the EU this year. After years of pushing for even tighter import restrictions, their calls appear to have hit home, as the European Commission accelerated trade defense measures by launching an anti-dumping investigation into imports of hot-rolled flat products originating from Turkey in May.

The Commission additionally notified the WTO the same month that it would move the global safeguard import quota for hot-rolled coil to a country-by-country quota from July 1. This means that each country has a different contingent that can be imported and if the import volumes exceed the quota, a 25% tariff-rate duty applies. While country specific quotas have been in place for other steel products, HRC had received a global quota.

The new anti-dumping investigation into Turkish HRC is in response to an increase in imports from Turkey and Turkish suppliers’ comparatively low import prices.

The anti-dumping duty would apply until the quota was filled. Once it is filled, further duty levels would be applied depending on the initial duty rate. This means Turkish imports would face tighter restrictions, although latest data from Eurofer showed substantial year-on-year decreases in Turkish imports in the first three months of this year.

In March, EU imports of HRC dropped 16% on the month, and 40% on the year to 452,502 mt. Turkish volumes were 56% lower than March 2019’s 319,289 mt.

According to the EU’s notification to the WTO, seen by S&P Global Platts, Turkey can export 344,890 mt of HRC to the EU in the quarter starting July 1, with similar quarterly limits in the subsequent periods up to and including Q2 2021.

Price moves during pandemic

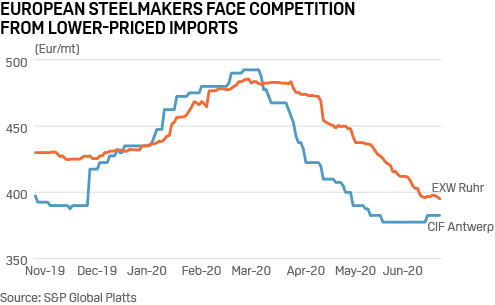

European finished steel prices have taken a dive due to the slump in demand since the pandemic unfolded in March, despite ramp-up efforts by key consumer markets since late April.

The price of HRC,ex-works Ruhr – a benchmark for flat steel, which has been severely affected by the auto-plant shutdowns – has fallen around 18% since the beginning of March according to the daily Platts TSI Northwest European HRC index. Northwestern European mills tried to hold offer prices up but eventually had to make concessions.

The trend was similar in Southern European flat steel prices, with HRC ex-works Southern Europe falling 13.5%. However, lockdown restrictions had been more severe on the supply chain there with the result that the overwhelming majority of buyers and sellers had to stop production.

Increasingly, more competitive import offers ex-Russia and Turkey for flat steel are putting additional pressure on domestic European prices. Although rebar import quotas for some countries such as Turkey have been exhausted, and European buyers are having to look more into sourcing material domestically, construction steel prices have also moved lower on weak demand.

Rebar prices have fallen further after intermittent rises in late March as scrap supply tightened due to restrictions on collection. While European scrap prices recovered after a brief drop in late March, though they remain volatile overall, rebar did not follow suit and has fallen by 8.5% since early April, according the weekly Platts TSI Northwest rebar assessment.

Although mills are continuing to restrict production, it is still outpacing demand across Europe. Particularly in countries such as Germany, where the government did not impose a shutdown, production continued throughout. As a result, mills had to search for buyers outside of Europe to sell volumes as demand was still failing to keep up with production.

Steelmakers have been warning of recessions in key markets and German mills are making extensive use of the government’s short-time working scheme. Order intake was low in March and April, which means that production rates in May and well into the summer will be affected as the entire steel supply chain is disrupted.

Squeezed into consolidation?

With the European steel industry in the doldrums and margins squeezed as showed by the low prices, some merger and acquisition activity could re-emerge to help mills to cut costs.

Thyssenkrupp, Germany’s largest steel producer, said in May that the new environment the steel market is finding itself in would increase the need for consolidation, as Europe simply has too much capacity. The steelmaker revived its merger talks with undisclosed partners and is – following the collapse of the merger with Tata Steel in 2019 – now actively looking again to consolidate its steel operations to save costs. There is talk in the market that Swedish steelmaker SSAB and Chinese steel company Baosteel would also be part of the talks.

There are also persistent reports that ArcelorMittal, the world’s largest steel producer, which has its core business in Europe, could withdraw from its Italian asset, the former Ilva works at Taranto, due to an option to withdraw from the troubled works in November. Adding fuel to speculation about the company’s strategy, in a plan for the 2020-2025 period presented to the Italian government, ArcelorMittal Italia reduced an existing target to ramp up crude steel production to 6 million mt/year by 2025, from 8 million mt/year previously, with a loss of 3,300 jobs in the process.

Industry sources have suggested that ArcelorMittal’s requests for government loans to help finance the Ilva acquisition could now be problematic, given the planned lower output and redundancies. Sources close to the Italian government said the government is divided between some who want ArcelorMittal to stay and others who want a future for the former Ilva facility without ArcelorMittal.

New direction needed

The current crisis has again brought into focus the issue of overcapacity in the European steel sector. Steelmakers in the region have been focusing on the automotive industry for years by reopening previously idled production lines or building entirely new ones.

The demand from the car industry was going from strength to strength until the emission testing scheme changes put a halt on it in 2018. A slowdown was long feared by market participants but mills pushed on with their race towards the automotive industry. Those whose biggest customers are the car industry are now hurting the most.

“Mills have been focused on the auto industry for years and that is breaking away. Auto has turned out not to be the right path,” a German distributor told Platts. European steelmakers particularly have been reluctant to take out capacity in the market, despite constant calls for streamlining of production by the producers themselves. They said they would be shifting from making commodity grades to higher grades which have a higher selling price.

According to Eurofer, in 2021, provided that the steel industry has been able to restore its production at normal conditions, the launch of new car models – many of them electric vehicles – could be a supportive factor along with rises in real wages and labor market dynamics on the demand side.

However, subdued car demand in major markets such as the US, China and Turkey would remain a challenge for EU car exporters, the association said.

It remains to be seen whether the pandemic will be the final push that finally forces mills to tackle their excess capacity.