09 Mar 2023 | 10:38 UTC — Insight Blog

China's economy is on a patchy way to recovery

China has witnessed a rapid revival of consumer spending in service sectors since the Lunar New Year holidays started Jan. 21, bouncing back from a distressing period during an unprecedented pandemic wave in December and January.

There has been a remarkable growth seen in spending, indicated by a flush seen in sectors such as dining, moviegoing, accommodation and tourism.

Enthusiastic tourists have flocked popular cities since late-January, booking up hotels and even pushing up local coffee prices.

Some popular restaurants amassed waiting lists exceeding 4,000 tables per day during the January holidays, and 1,000 to 2,000 tables on weekends in February, according to sources.

People are also lining up at popular temples to pray for their 2023 fortune. January-February ticket orders for temple-related scenic spots increased by 310% on the year, according to data from Chinese travel agency Ctrip.

Yet something has been amiss during this period of meteoric rise seen in spending.

At a time when air tickets and hotels in popular cities are rising, urban bus operations in Shangqiu, a city with close to 8 million residents in central China's Henan province, were nearly suspended in late-February due to inadequate fiscal subsidies.

While the number of people, mostly tourists, applying for outbound travel permits in Shanghai hit an all-time high in January, the number of empty containers waiting for export goods at the ports of Shanghai and Shenzhen hovered in near-record high as of end-February.

Fancy coffee shops in big cities are seen packed with people enjoying sunny afternoons, but people with poor expectations of future income and property prices have largely reduced their spending, leading to huge excess savings.

The increase in China's household deposits hit an all-time high of Yuan 17.9 trillion ($2.589 trillion) in 2022, much higher than the Yuan 9.9 trillion increase in 2021, according to the People's Bank of China. In January, this increased by Yuan 6.2 trillion from a year ago, also a record-high growth ever for the month.

According to respondents to PBC's latest survey, more than 60% of urban savers prefer "more savings," while only 16% prefer "more investment."

Recovery remains fragile

These conflicting scenarios indicate that the road to China's economic recovery in 2023 may be patchy.

The sharp increase in savings last year was largely due to reduced investment spending by mid- and upper-income households amid the slowdown in property sector. But China's reopening from the pandemic lockdowns is unlikely to trigger a flow of the savings into the consumption sector.

The current "revenge spending on services," as well as the sales growth in passenger cars and some home appliances, might not be sustained.

The key to a sustainable consumer spending recovery in China is the increase in disposable income of low- and middle-income households. But these are the groups that will be mostly weighed down by the slowdown in property investments and shrinking overseas demand for Chinese manufactured goods this year.

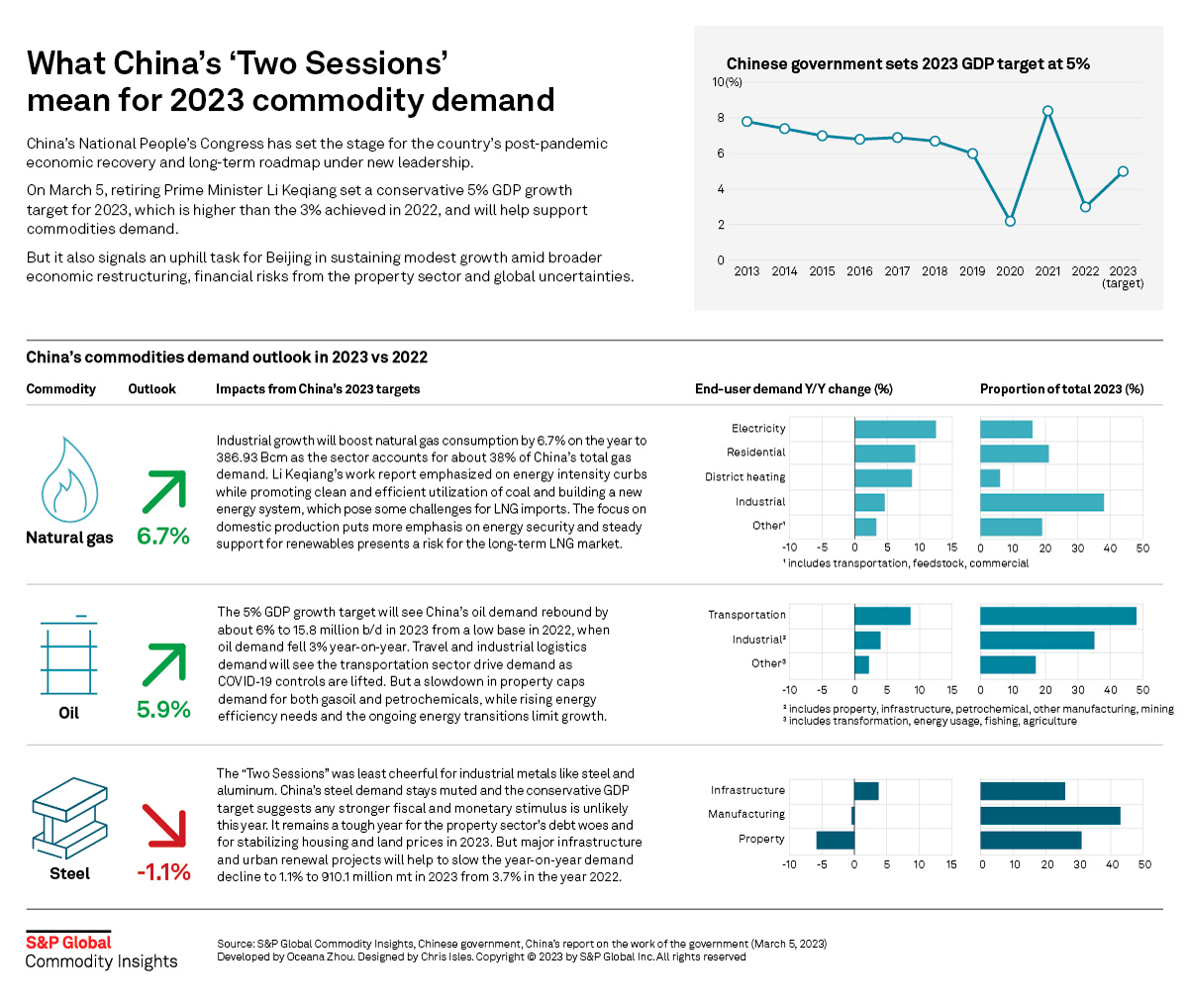

Moreover, during the "Two Sessions" China set its 2023 GDP target at a conservative 5%, suggesting fiscal and monetary stimulus this year – either for investment or consumption – will be comparatively modest, according to market sources.

The country has announced to align broad money supply (M2) with the GDP growth in 2023, indicating the growth rate of M2 this year is likely to be lower than that in 2022 at 11.8%.

According to National Bureau of Statistics data, the disposable income per capita of the bottom 20% of the population is only about a tenth of that in the top 20% in 2022.

End of an era

Moreover, China's property sector – a crucial driver for economic growth, as well as for metals and some other bulk commodities demand – may continue to see a downward trend in the long-term after an upcycle that lasted more than 20 years.

In 2022, China's population growth turned negative for the first time in 61 years. According to the China Population and Development Research Center, the country is likely to have a negative population growth for decades to come, although the decline will be slow and gradual at least before 2035.

Urbanization rate reached 65% in China last year, but the actual rate could be much higher. Many young people from rural areas have already moved to work in cities, although they are still counted statistically as part of the rural population.

Since the Q3 2022, a plethora of policies to encourage home buying have been introduced in China in an attempt to stabilize housing prices and ease debt woes in the property sector.

The average loan interest rate to first-home buyers in 103 major cities has dropped to a four-year low in mid-February, according to data from a Chinese property data provider Beike Research Institute.

The year-on-year growth rate of China's M2 also hit a six-year high in January at 12.6%. With such a large supply of liquidity, new-home prices in tier-one cities have shown signs of recovery as of February, and speculative buyers are once again actively scouting for investment targets at good locations.

However, for most of the smaller cities, the prospects may be different.

Negative population growth has changed people's expectations for property in small- and medium-sized cities. When people realize children in smaller cities will inherit two, or sometimes even four or five homes from their parents and grandparents but cannot find enough tenants or buyers, injecting liquidity into the property market will not persuade them to buy more properties in these locations.

In an economy facing a tough year to stabilize housing and land prices, with the exception of tier-one and some strong tier-two cities, the birth of another housing boom is unlikely.

Moreover, China's service sector may soon become the source of inflation, which could also limit policy room for supporting property sector in H2.

China's property steel demand is likely to fall by 5.8% on the year to 280 million mt in 2023, after a drop of 12% on the year in 2022, data from S&P Global Energy showed.

The slowdown of activities in the property sector also weighs on diesel demand, which is used as energy for construction and fuel for transporting materials. The barrel is estimated to have the slowest year-on-year growth in 2023, at 4% to 4.1 million b/d, among clean oil products. This is much slower than the 9% and 45% for gasoline and jet fuel, respectively, according to S&P Global.

Aluminum demand from property sector may slightly recover in 2023, because new-home completion is expected to see an increase amid the efforts to ensure timely deliveries of pre-sold homes.

China's primary aluminum consumption could reach 41.9 million mt in 2023, up 2.2% from 2022, driven by demand from the photovoltaic, new energy vehicle, extra-high voltage and new infrastructure sectors, according to state-run research agency Antaike.

China's commodity demand has been a centerpiece for the broader global economy for years and 2023 seems to be no different. Focus has already shifted to the one of the world's most influencing economies in a year that is signaling the country could be walking a difficult road to recovery, keeping global markets wide awake.