24 Jun 2020 | 18:51 UTC — Insight Blog

Will ERCOT summer power prices see a repeat of 2019 fireworks?

By Travis Whalen and Manan Ahuja

After breaking records for on-peak power prices in August 2019, the Electric Reliability Council of Texas (ERCOT) is facing more limited risk this summer season amid expectations of higher reserve margins.

More generation and uncertainty around peak loads due to stuttering economy should make for less strain on the system. However, the factors that led to last year’s price spikes remain, and new elements have been added to the equation, reinforcing the enormous upside tail risk in pricing.

On the supply side, around 3 GW of new wind and solar capacity is being factored in for this summer, but much of that has yet to come online. Meanwhile, on the demand side, the region is experiencing a slump in demand familiar to many other areas in the US and worldwide due to economic slowdown in the wake of the coronavirus pandemic. A factor specific to ERCOT, however, is the prevalence of shut-ins in the Permian oil sector due to the weak crude price environment, which heavily affects the region’s economic activity.

Build-up to a blowout

Before delving into risks for summer 2020, it is important to understand what happened last year.

The idea that summer prices in ERCOT could spike was hardly unexpected. The final Seasonal Assessment of Resource Adequacy (SARA) report for summer 2019 pegged reserve margins at only 8.6% and expected inadequate reserves even below normal outage rates. Nonetheless, from June 3 to August 1, ERCOT on-peak forward prices for August fell roughly 27% in light of milder-than-normal weather that led to weak real-time pricing.

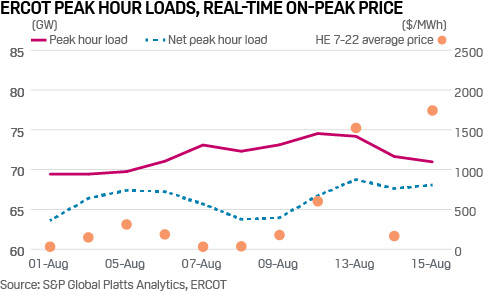

When the spikes did come, they highlighted most of the notable risks laid out in the SARA report’s scenarios. While peak load remained relatively in line with ERCOT’s forecast (74,666 MW compared to a forecast 74,853 MW), two energy emergencies and their associated price spikes ultimately resulted from wind generation shortfalls and high outages, both separately and together.

The first emergency came only a day after ERCOT comfortably managed its record-setting peak load. ERCOT was forced to call an energy emergency despite seeing a daily peak more than 360 MW lower than the day prior and more than 500 MW fewer outages throughout the peak hours. A 1.4 GW drop in wind output during the peak hour, however, countered those improved conditions and sent prices to their $9,000/MWh cap.

The second emergency – two days later on August 15 – came nowhere near the forecast peak load, capping out at only 71,073 MW. Even the net load showed a significant decline from earlier in the week despite wind output falling nearly another 1 GW. Outages, however, also jumped another 1.1 GW as plants looked to recover after burning hard to meet those record-setting loads.

A similar story played out in September, as the summer drew to a close and planned maintenances started to ramp up. Prices jumped to more than $220/MWh on September 9 despite peak net loads nearly 9 GW below their high water mark from August, driven by a nearly 6 GW increase in outages.

The risks of increased reliance on renewables during hot summer peaks have been a prominent topic in ERCOT for years. These September price spikes drew attention to the added risks of relying on older, infrequently used generation to fill in the gaps left by intermittent wind and solar generation. Significant maintenance requirements after a stretch of warm weather run the risk of exacerbating tight reserves and, as seen last year, widening the window for significant price volatility.

Same old song and dance?

Given the historic pricing levels, one could be forgiven for thinking there might be dramatic changes lined up in ERCOT’s generation mix to help meet growing demand. While there will undoubtedly be some deferred retirements after last summer, and Gibbons Creek coal plant already expects to restart on a seasonal basis, the story for this summer looks very familiar.

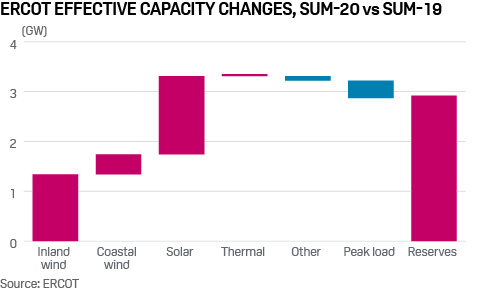

Last year, nearly all of the incremental capacity available for the summer came from intermittent generation additions. Wind and solar accounted for 95% of capacity coming online from September 2018 until August 2019. This year, wind and solar are slated to account for 99% of all new capacity, though smaller incremental changes have been achieved at existing plants.

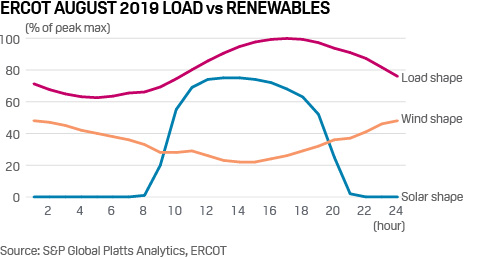

The crucial difference for this summer, however, is that solar now accounts for the majority of incremental capacity additions. While ERCOT revised its accounting of wind projects to better reflect the higher output coming out of the panhandle and coastal areas, no wind projects are consistently seeing the same level of output during peak hours as solar sees throughout the summer.

This presents solar as a potentially more reliable option for meeting demand growth that also helps diversify the risks ERCOT must account for away from the three primary factors of load, wind, and outages currently modeled in the SARA. Solar still presents its own risks, as output fell as much as 8% below expectations during some of the hottest peak hours last summer, illustrating that high temperatures and load are not always correlated with strong solar generation.

What could go wrong?

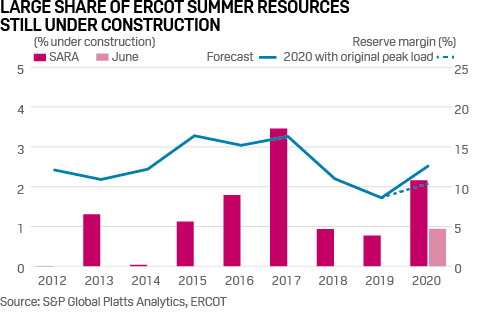

As ERCOT increasingly looks to solar to tackle its summer peaks, the obvious question becomes whether that solar has actually materialized. As much as 78 GW of solar projects have made their way into ERCOT’s generation queue, but actual capacity still remains below 3 GW. And while 900 MW of solar capacity has come online since the end of summer last year, a significant amount being included in this year’s reserve margin estimates has yet to come online.

At the time ERCOT released the final summer SARA in mid-May, roughly 2.2% of total expected effective capacity was still under construction. That marked the highest level of reliance on uncompleted plants since the SARA reports began outside of 2017, when two large combined cycle plants were set to come online. But in 2017, reserve margins remained at a healthy 16.3%, well above ERCOT’s target. While more than half of this year’s anticipated capacity had come online by mid-June, the more than 770 MW of effective peak capacity still accounts for roughly 1 percentage point of ERCOT’s already tight reserve margin.

The reserve margin remains something of a moving target as well. As with the rest of the world, Texas has weathered the impacts of the novel coronavirus on its people and its economy, though Texas’s economy was hit particularly hard by the simultaneous plunge in crude oil prices. While S&P Global Platts Analytics models suggest loads had crept fairly close to expected values by mid-May, ERCOT continued to report peak loads from 1% to 4% below expectations even late in the month. That led ERCOT to adjust its summer peak load estimates down by around 2%, boosting reserve margins by a comparable 2 percentage points.

The pace of recovery remains uncertain everywhere, but in Texas in particular that uncertainty can be tied significantly to one main industry. The plunging demand for oil, a price war between Saudi Arabia and Russia, and booming production out of the Permian sent West Texas Intermediate (WTI) crude prices into the negatives for the first time ever.

Aside from sending rig counts in the area off a cliff, the extreme conditions resulted in more than 600,000 b/d of production being shuttered, even from newer, more productive wells. While oil drilling tends to have a lagged impact on power demand, shutting that many wells undoubtedly had an immediate impact on ERCOT’s load.

After averaging more than 20% annual weather-adjusted load growth for years, ERCOT’s Far West zone that covers most of the Permian fell to a growth rate of only 2% in May. But with WTI already back into the mid-$30s, it’s unclear how long those wells will remain offline, and Platts Analytics currently expects production to mostly bounce back by the typical summer demand peak in August.

The current drought outlooks remain positive for ERCOT, which means somewhat lower loads and typically lower maintenance outages, but long-term weather forecasts do present some risks. The National Weather Service Climate Prediction Center estimates between a 50% and 70% chance of higher-than-normal temperatures throughout the summer months in most of Texas. Though forecasts as far out as two months have significant error, this outlook nonetheless adds to the list of uncertainties that seem to indicate significant upside risk to summer pricing.

Despite the numerous risks that could align to send ERCOT prices skyrocketing, Platts Analytics’ risk-weighted forecasts ultimately average out notably below the market. Forecast July and August on-peak prices average between 14% and 19% below current market forwards. That gap reflects the expectation that essentially all anticipated generation comes online before peak loads hit, as well as assuming an extended recovery period comparable to other regions around the country. While the risk to the upside can be extreme, the most likely scenario seems to be another summer like the more moderate 2018.

Large generation companies well hedged

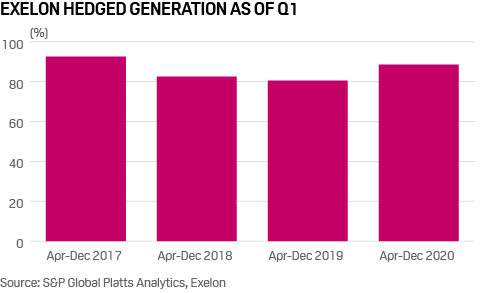

The hedged positions of large generation owners in ERCOT this summer also support Platts Analytics’ view of potential for lower prices. As of end-March 2020, Exelon’s ERCOT generation was 87-90% hedged for balance of year (April-December 2020). This is significantly higher hedge than the 79-82% hedged for April-December 2019 at end-March 2019 and also higher than hedging for the

same period in 2018(81-84%). Interestingly, this is similar to the level of hedging

last witnessed in 2017.

NRG, which owns generation and serves retail load in ERCOT, also seems to have a similar positioning. According to the company’s recent Q1 earnings call, it is well hedged and is “not net short”.

Also, Vistra energy - which owns generation and serves retail load in ERCOT - stated in its Q1 earnings release that it is close to 100% hedged for balance of 2020 in ERCOT. This is in contrast to the unhedged generation length position it carried into the summer months around this time in 2019.

Though all these market participants acknowledge the upside risk in ERCOT summer pricing, their hedge positioning indicates that there’s much lower expectation of large upside in prices this summer in ERCOT.

The longer-dated ERCOT curve staying much weaker also implies that there is little incentive for a lot of new generation to be built. That means the tight reserve margin situation is likely to persist for a while as the load growth in Texas continues, and while there are no formal capacity market or reserve margin targets.