11 Mar 2020 | 20:42 UTC — Insight Blog

India’s King Coal faces challenge as renewables look to scale up

Coal remains central in the power mix of the developing world, with coal plants still being built across Asia in order to meet rising baseload electricity needs.

However, a more challenging macroeconomic environment and slowing power demand growth are raising some questions around the growth of coal even in developing economies.

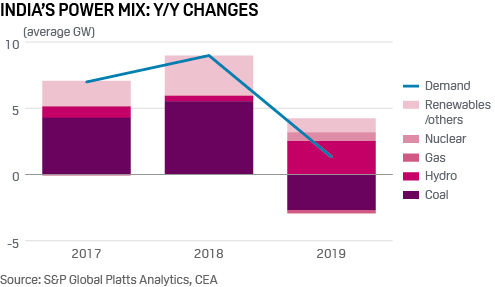

Last year may have marked a turning point in India – a country where coal accounts for over 70% of the power mix – as S&P Global Platts Analytics data shows the amount generated from coal dropped for the first time in history by an unexpected 2% year on year.

This was a stark contrast to the 7% annual average growth over the previous five years. The drop signals how far India’s energy transition has come, with renewables making clear inroads into the power mix.

However, lower Indian coal-fired output during 2019 has also been more clearly driven by a marked slowdown in demand growth for electricity. India’s electricity demand had been growing to the tune of 6% a year in 2014-18, but 2019’s growth was a mere 0.9%, equivalent to about 1.3 GW on average, accounting for the largest driver of the changes in coal use.

A weaker economy and a prolonged monsoon season in 2019 are partly to blame. More recent official data for January shows year-on-year demand growth recovering to 2.2%, while February is up 5.9% year on year.

In other words, power demand growth appears to be facing some structural challenges, but with GDP growth averaging 6% or so in the upcoming five years and power consumption per capita among the lowest in the world, there is clearly an upside for power demand, which will underpin coal. In particular, increased population would clearly lead to higher air-conditioning use, especially at peak hours.

Also, there was roughly a 20%, or 2.5 GW, surge in hydro generation in 2019, while nuclear availability was above average, up 18%, or equivalent to almost 700 MW, on average. As for renewables, output growth has been actually slower, with generation up only 1 GW over the last year.

India’s “young” coal fleet

The latest data shows utilization of existing coal units has dropped to just 56%, against 63% five years ago. The declining role of gas in power is also noteworthy, with plant load factors at a rock-bottom 22% in 2019 compared to their peak of 67% in 2010.

A lack of domestic gas availability has been the root cause of this slump, while LNG burn in the power sector has been limited by grid infrastructure constraints. The joint statement by President Trump and Prime Minister Modi following a state visit by the US leader to India in February notes the vision to “accelerate access to LNG in the Indian market”, yet India’s power sector is not currently offering great prospects for LNG.

The pace of coal newbuild has slowed considerably, but almost 8 GW of coal still managed to come online over the past year. There is no doubt, however, that thermal assets are facing a more challenging environment, with fuel logistics constraints compounding lower utilization and payment delays by electricity distribution companies that are already losing money.

Compliance with tighter emission standards is adding to those challenges. About 166 GW of coal capacity has to undergo retrofitting, out of the 203 GW currently operational.

Compliance deadlines have been extended, but it’s interesting that in the most recent 2020-21 (April-March) budget speech, finance minister Nirmala Sitharaman announced that for the “power plants that are old and their carbon emission levels are high…we propose that utilities running them would be advised to close them, if their emission is above the pre-set norms.”

However, the weighted-average age of the coal fleet in India is only 13 years, making large-scale retirements unlikely. In fact, only about 1.4 GW of capacity was retired during 2019.

RES plus storage competitive with thermal

As for renewables, the resource potential is large, especially for solar, as plants are being developed with fixed priced long-term power purchase agreements awarded through competitive auctions held by the Minister of New and Renewable Energy’s SECI or other state-level agencies.

Go deeper: Request S&P Global Platts Analytics' latest Global Solar Outlook

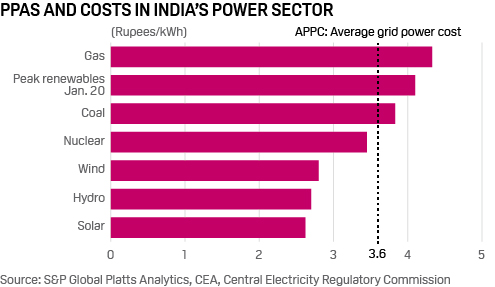

Renewables output in recently awarded projects is being compensated in the Rupees 2.50-3/kWh range ($35-$42/MWh). This price is well below current prevailing PPAs covering coal and gas plants and also the benchmark grid costs for power (APPC, as determined by the Central Electricity Regulatory Commission).

The recent, 1.2 GW renewables-plus-storage auction, with projects awarded at Rupees 4.0-4.30 /kWh on average has also been particularly interesting. The awarded plants – a combination of pumped hydro, batteries and renewables – are in line with Platts Analytics' estimated costs for a typical solar-plus-battery project. As the chart shows, this tariff is not only low compared with the gas plants, but also even challenges the role of coal as a provider of flexibility and reserve services.

Renewables face constraints

Policy support for renewables is also strong, but with 34 GW of utility-scale solar PV and 37.6 GW of wind installed as of January, India has a long way to go to achieve its ambitious goals of 175 GW by 2022. Solar PV additions have stalled to less than 8 GW/year, while wind capacity commissioned slumped to 2.4 GW in 2019.

Despite a bold policy agenda and competitive pricing, renewables development has also been hit by the broader structural issues facing the Indian power sector. Receivable delays have become a growing issue also for renewables developers, with high counterparty risks a concern for highly leveraged projects. Capacity successfully auctioned is only a fraction of the tenders, with cancellations or postponement becoming frequent last year.

The introduction of import duties on solar PV modules has led to uncertainties and cost increases for projects that had already secured PPAs at fixed prices. The coronavirus outbreak has also been impacting the supply chain of PV modules in China and this could in turn slow the commissioning of projects, since China is the largest supplier of vital parts for India’s solar panels.

Finally, the expansion of the transmission grid will have to be timely to prevent an increase in curtailments, which would hurt projects’ revenues. India’s renewables industry is facing some headwinds despite its great potential and the process of scaling it up will require further strong policy action.

New nuclear makes slow progress

India currently has 21 nuclear reactors totaling 6 GW of nuclear generation capacity, accounting for only 2% of the fleet, with aggressive expansion plans. Capacity totaling 6 GW is currently under construction, but commissioning times have been particularly lengthy, due to delays from supply chain companies providing equipment, as well as financial constraints. There are plans for around another 20 GW of capacity.

Co-operation in nuclear power was also part of the recent Trump-Modi talks. Six AP-1000 reactors, for a total of 6600 MW, designed by Westinghouse are expected to be used in the Kovvada power plant in the Andhra Pradesh state.

However, no deal has been signed, while the joint statement between the two heads of state “encouraged the Nuclear Power Corporation of India Limited and Westinghouse Electric Company to finalize the techno-commercial offer”.