15 Oct 2020 | 19:03 UTC — Houston

US oil, gas rig count up by 13 to 336 on week, resuming double-digit leap: Enverus

Highlights

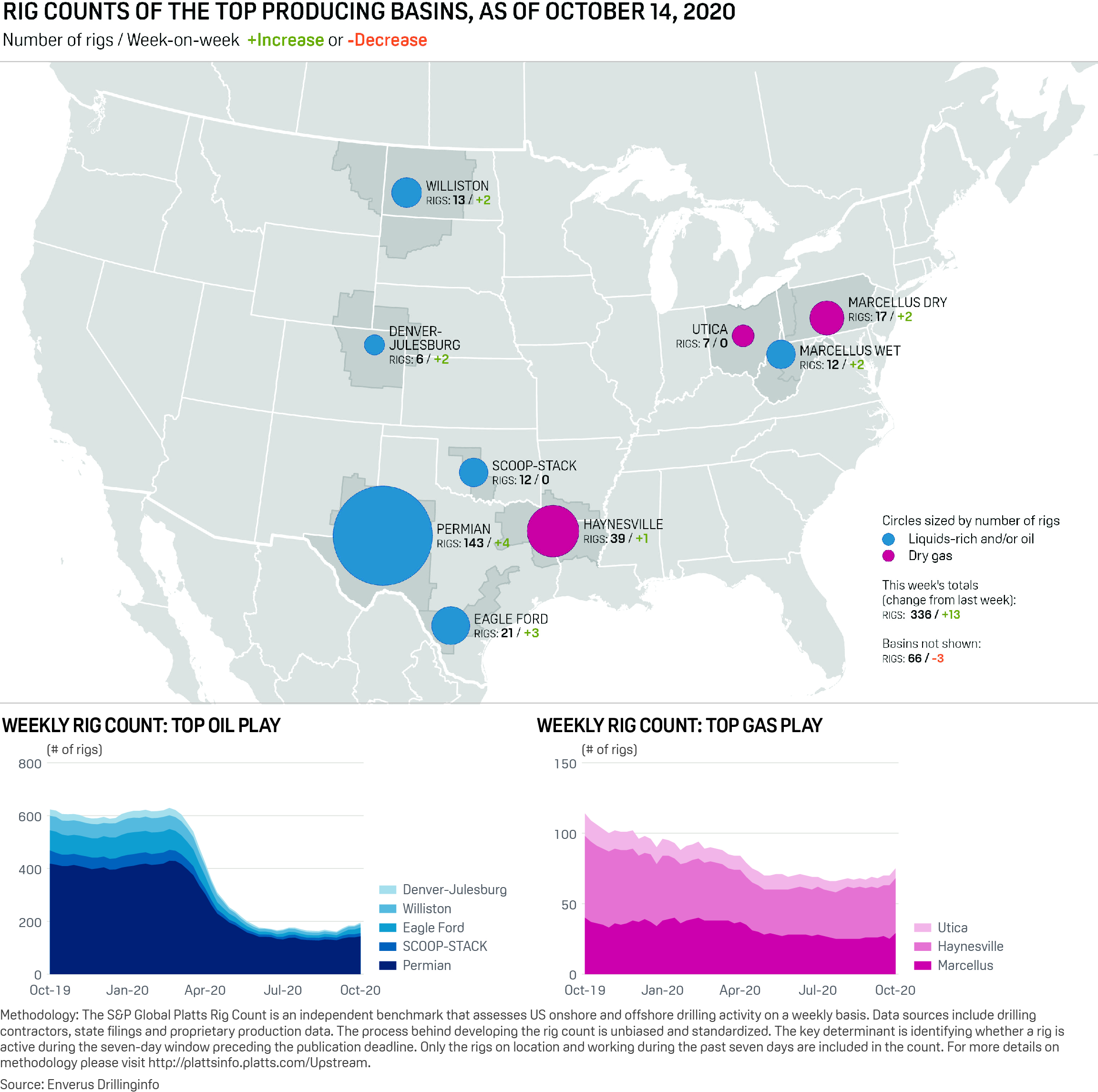

Oil rigs up 10 to 238; gas rigs up 3 to 98

Most domestic basins gained multiple rigs

Awaiting industry landscape updates in Q3 calls

Houston — The US oil and gas rig count rose by 13 to 336 on the week, rig data provider Enverus said Oct. 15, as activity ticked up on the heels of what experts say may be a final push to complete projects in 2020 with remaining capital budgets.

Oil rigs accounted for the bulk of increases, up 10 to 238, but natural gas rigs were also up by three to 98.

"These modest week-on-week gains were expected," analyst Matthew Andre of S&P Global Platts Analytics said. "Relative to what we've seen for growth it's pretty good. I'm not sure we'll see [double-digit] rig gains every week for the rest of the year."

Horizontal activity, a better indicator of shale activity since it focus on players drilling larger, more productive wells, has climbed recently and is now at 265, up by seven on the week – far past its long rangebound period in the 230s-240s from June through most of September.

Since then, the horizontal rig count has ticked up steadily.

"This relatively widespread recent stability increases our confidence that the horizontal activity trough is now indeed behind us, and we continue to expect to see further modest gains into year-end 2020," Tudor Pickering Holt said in its daily investor note Oct. 12.

Horizontal rig count highest since June

This past week is the highest the horizontal rig count has been since June, although it's still just about a third of its recent peak of 734 in late February 2020.

Most domestic basins saw multiple rig gains on the week and none lost rigs. Biggest were the Permian Basin and the Marcellus Shale, which each increased by four rigs. That resulted in totals of 143 rigs in the Permian, sited in West Texas/New Mexico, and 29 in the Marcellus, a largely gas-prone basin mostly in Pennsylvania and neighboring states.

In addition, the Eagle Ford Shale of South Texas was up by three to 21, a volume not seen in the basin since mid-May. Also, the Bakken Shale of North Dakota/Montana and DJ Basin of Colorado were each up by two rigs, for respective totals of 13 and six.

The SCOOP/STACK play in Oklahoma and Utica Shale of Ohio held steady at 12 and seven rigs respectively. The gassy Haynesville Shale of East Texas/Northwest Louisiana was up one to 39, the most activity posted in that play since late March.

All things considered, the relatively buoyant rig activity of the last week comes a week before Q3 earnings begin, which typically provides a glimpse into activity outlooks during the following few months and the rest of the year.

This year's Q3 outlooks will be especially scrutinized since activity is sluggish from two full quarters of activity tamped down by the coronavirus pandemic, as operators slashed drilling rigs and their 2020 capital budgets beginning in March.

The oil and gas rig count, at its July trough of 279, was down more than 65% from early March.

2020 calls may now focus on broad themes

Analysts say this year has not only been about lower oil demand and reduced activity forced by the pandemic, but unmasks the consequences of years of poor industry decisions regarding the pace of production growth and overspending.

"2020 has become Judgment Day for E&Ps," Evercore ISI analyst Stephen Richardson said in an Oct. 15 investor note.

Third quarter is typically the period where the unmet expectations from earlier in the year begin to show up and market focus shifts to the year ahead, Richardson said.

"But this year is different, with subtle changes in activity and well performance affecting year-end 2020 exit rates and strategy updates likely to outline how 2021 will be handled," he said. "Unsaid is that with calendar year 2021 [forward curve prices] hovering just over $40/b, the year ahead may not look much better for many."

Noting the rumor published Oct. 14 by Bloomberg of talks between ConocoPhillips and Concho Energy of a potential merger that could be announced in mere weeks, on the back of Chevron's already-completed takeover of Noble Energy, and Devon's pending combination with WPX Energy, Stephenson said these deals may prove the "tipping point where a better industry structure and behavior can be expected."

Wells Fargo analyst Nitin Kumar similarly believes Q3 calls will focus on broad trends – and consolidation in particular, and whether individual operators might play roles in that trend. "But we are not expecting too many updates to 2021 and beyond," he said, also in an Oct. 15 investor note.

The macro outlook – i.e., pandemic and oil price – is still uncertain and earnings mostly occur before the US presidential election, he said. Consequently, "operators ... are unlikely in our view to give more clarity [on capex and production outlooks] than they already have."

Click here for full-size image

{kind=link}