10 Jun 2021 | 20:11 UTC

US working natural gas volumes in underground storage increase by 98 Bcf: EIA

Highlights

Balance-of-summer Henry Hub rises above $3.15/MMBtu

Forecast shows smaller injection ahead

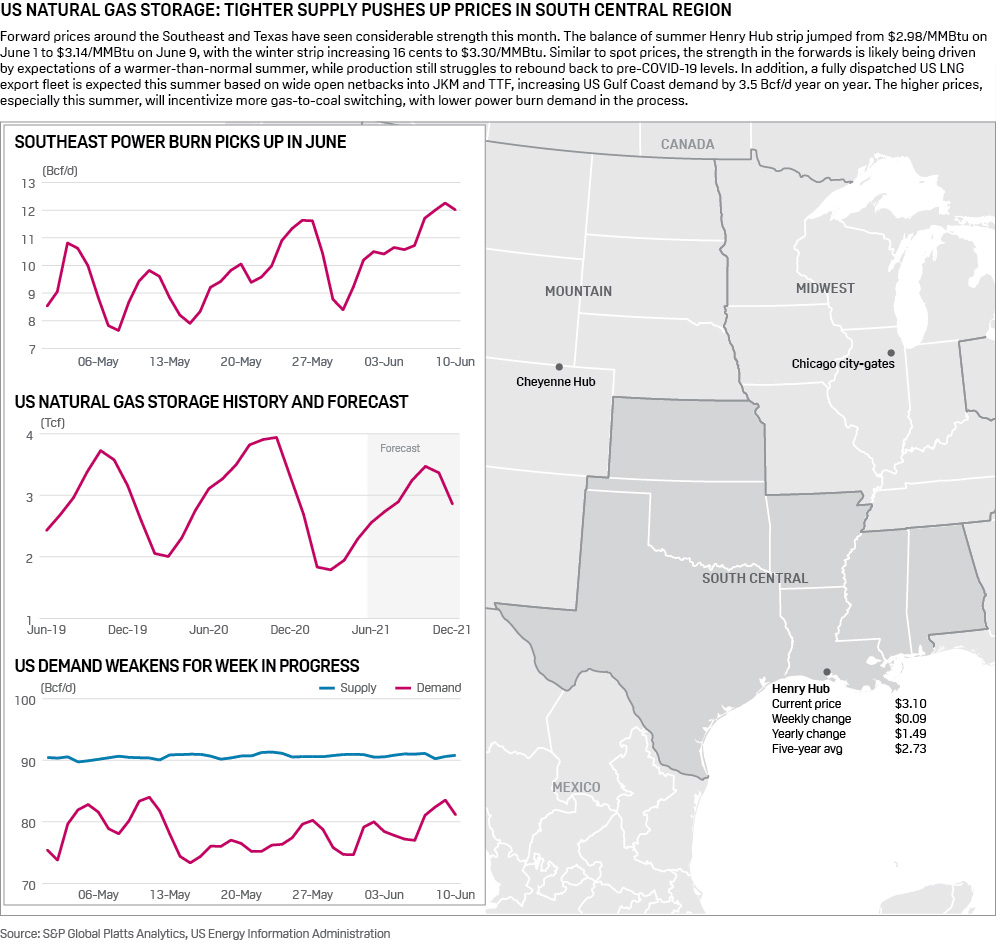

US natural gas storage fields added just above the five-year average for the second consecutive week, but smaller builds due to greater power demand look likely for the rest of the month, providing support to Henry Hub futures.

Storage inventories increased 98 Bcf to 2.411 Tcf for the week-ended June 4 the US Energy Information Administration reported June 10.

The build was more than the 95 Bcf addition expected by an S&P Global Platts' survey of analysts, as well as the five-year average build of 92 Bcf, according to EIA data.

Storage volumes now stand 383 Bcf, or 13.7%, less than the year-ago level of 2.794 Tcf and 55 Bcf, or 2.2%, less than the five-year average of 2.466 Tcf. The injection matched the 98 Bcf added to inventories for the week prior.

Month-to-date total feedgas deliveries have averaged 10.1 Bcf/d, slightly below the June forecast of 10.4 Bcf/d, according to S&P Global Platts Analytics. When available, US LNG export facilities are expected to run at full utilization, about 11 Bcf/d, as netbacks into JKM and TTF remain wide open at $5/MMBtu and $4/MMBtu, respectively, through the end of the year.

The NYMEX Henry Hub July contract added 2 cents to $3.147/MMBtu in trading following the release of the weekly storage report on June 10. The balance-of-summer contract strip was trading higher by roughly 3 cents/MMBtu for an average of $3.175/MMBtu, while the winter 2021-22 strip was up 2 cents on the day, trading at $3.323/MMBtu.

Platts Analytics' supply and demand model currently forecasts a 56 Bcf injection for the week ending June 11, which would measure 31 Bcf less than the five-year average as gas-fired power generation draws on supply.

Summer appears to be fully underway during the week in progress, with power burn demand rising by more than 7 Bcf/d on the week. The effects of that were dulled by a 2.4 Bcf/d drop in residential and commercial demand, and a 1.7 Bcf/d drop in LNG feedgas demand thought to be linked to annual maintenance taking place at certain liquefaction plants on the Gulf Coast.

Amid fairly substantial changes in the various demand sectors, total US demand has seen a net increase of about 2.6 Bcf/d week over week. Supply, on the other hand, has been mostly stagnant, with nearly all of the week's 900 MMcf/d increase in total US supplies the result of an increase in imports from Canada.

Sample storage fields across the Lower 48 injected 20% less gas into storage for the week ending June 11, falling from an injection of 47 to 37 Bcf. Temperatures in the East and Midwest climbed by more than 13 degrees degrees week over week, pushing up local power burn demand and cutting into the volumes available for storage. The tighter injections in major demand regions were partially offset by small gains in the West, which saw a bit of a reprieve from the ongoing heat wave.