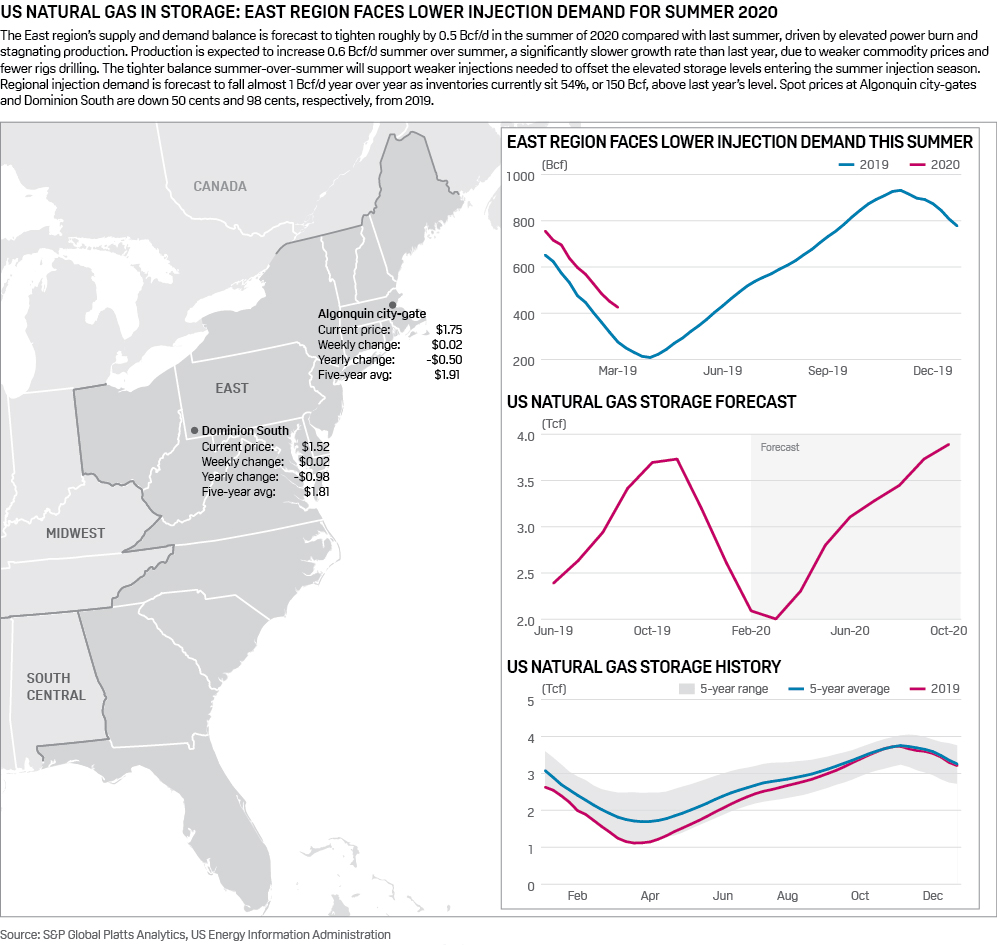

12 Mar 2020 | 15:23 UTC — Denver

US working natural gas in underground storage decreases by 48 Bcf: EIA

By Brandon Evans and Eric Brooks

Highlights

Volumes grow to 64% above this time last year

Small net injection possible for week in progress

Denver — Oversupply issues continue in the US gas storage as volumes fell by 48 Bcf, less than the market expected, and the NYMEX Henry Hub April contract retreated on Thursday morning from gains made earlier in the week.

Storage inventories fell by 48 Bcf to 2.043 Tcf for the week ended March 6, the US Energy Information Administration reported Thursday morning.

The pull was less than an S&P Global Platts' survey of analysts calling for a 55 Bcf withdrawal. It was much less than the 164 Bcf pull reported during the corresponding week in 2019 as well as the five-year average draw of 99 Bcf, according to EIA data.

Storage volumes now stand 796 Bcf, or 64%, more than the year-ago level of 1.247 Tcf and 227 Bcf, or 13%, more than the five-year average of 1.816 Tcf.

The NYMEX Henry Hub April contract slipped 7 cents to $1.80/MMBtu in trading following the release of the weekly storage report. The balance of the 2020 contract strip for NYMEX Henry Hub fell 5 cents to average $2.08/MMBtu.

Despite a bounce in prices earlier in the week supported by a collapse in oil prices, bearish domestic fundamentals continue to weigh on gas prices, especially in light of sticky production levels and falling seasonal demand, according to S&P Global Platts Analytics.

US supply-demand balances continue to slacken as the market lurches towards the shoulder season. On the supply side, production has managed to remain remarkably flat over the past several weeks. The week ended March 6 posted zero change to maintain an average of around 92 Bcf/d of combined onshore and offshore receipts. Rather than from production, lower Canadian imports drove most of the drop in supply, which fell by 0.6 Bcf/d for the reference week.

Platts Analytics' supply and demand model currently expects a 2 Bcf injection for the week ending March 13, which would mark the first net injection of year. The first net injection of the year typically occurs during the last week in March or first week in April, according to EIA data.

The week in progress has closely followed last week, with balances widening by 6.6 Bcf/d on small drops in supply matched with larger drops in demand. Total supplies are down 1.3 Bcf/d to average 94.5 Bcf/d, with almost all of the declines stemming from lower Canadian imports and LNG sendout. Downstream, total demand fell by about 7.9 Bcf/d, the vast majority of which was from residential and commercial usage as average US population-weighted temperatures increase.

Click here for full-size image

{kind=link}