Coal, Metals & Mining Theme, Metallurgical Coal, Ferrous

October 22, 2025

TRADE REVIEW: Asian met coal market eyes Q4 support from Chinese import demand

By Samuel Chin and Olivia Zhang

HIGHLIGHTS

Asian met coal prices rebound in Q3 on China buying

LV HCC relativities against PLV CFR China hit four-year high

Q4 outlook hinges on China policy, India post-monsoon demand

This report is part of the S&P Global Energy Metals Trade Review series, where we dig through datasets and digest some of the key trends in iron ore, metallurgical coal, copper, alumina, cobalt, lithium, nickel and steel and scrap. We also explore what the next few months could bring, from supply and demand shifts to new arbitrages, and to quality spread fluctuations.

The Asian seaborne metallurgical coal market is poised for firm prices in the fourth quarter, supported by the expected recovery in Indian demand following the monsoon season and sustained interest from China. However, the outlook remains contingent on potential policy shifts in China, particularly regarding steel production and coal mining.

In Q3, regional prices across grades were buoyed by a rebound in Chinese low-vol hard coking coal demand, which also supported a recovery in LV HCC price relativities against the premium low-vol hard coking coal assessment.

Conversely, India, the largest importer of seaborne metallurgical coal, saw limited interest due to its prolonged monsoon season, which extended into mid-October.

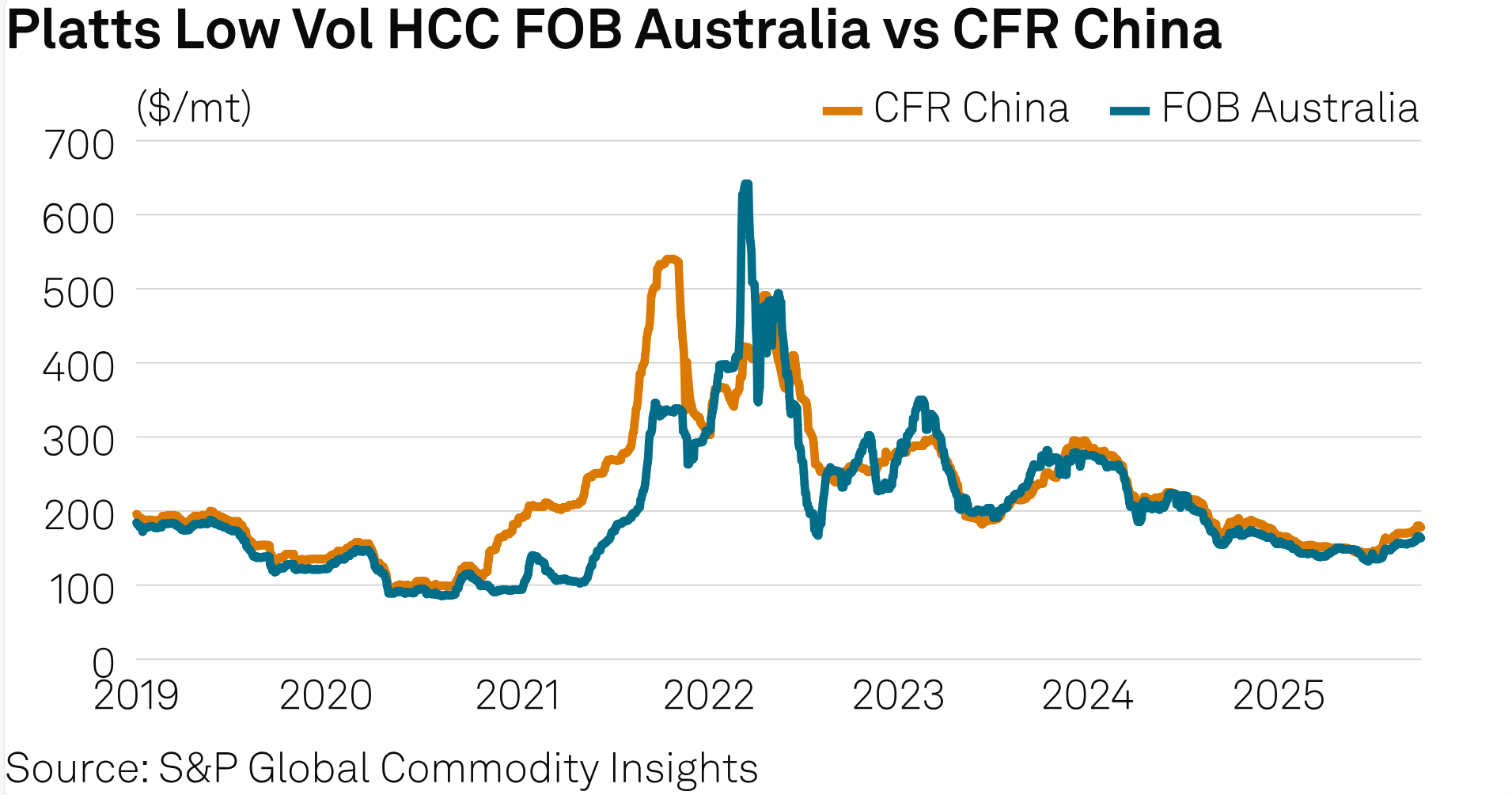

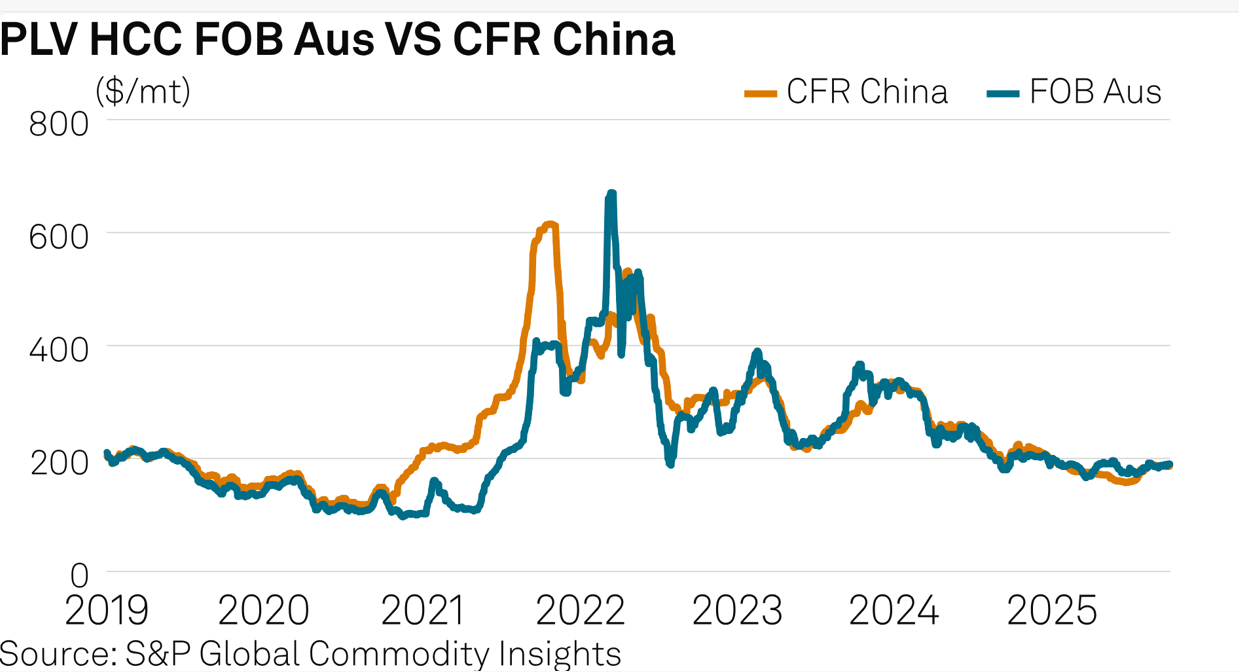

Premium hard coking coal prices rose steadily through Q3, according to data from Platts, part of S&P Global Energy, with the Platts PLV HCC index recovering $16.7/metric ton, or 9.6%, through the quarter, from $173.5/mt on July 1 to $190.20/mt on Sept. 30

China returns to LV HCC spot market

Chinese spot seaborne activity rebounded in Q3, following a rally in coking coal futures on the Dalian Commodity Exchange since early July.

The most active January contract surged 78% in Q3, reaching Yuan 1,258.50/mt ($176/mt) on Sept. 17, up from a nine-year low of Yuan 709/mt on June 3. The contract closed the last trading day of Q3 at Yuan 1,126/mt, just before the Golden Week holidays on Oct. 1-8.

The rally was part of a broader ferrous price increase in China earlier in the quarter, spurred by positive GDP data released July 15 by the National Bureau of Statistics and a July 21 notice from Henan's provincial government calling for curbs on coal overproduction.

Higher domestic coal prices created arbitrage opportunities for coking coal traders, with the spread between domestic and seaborne prices widening to $20/mt on Aug. 13, according to Platts' calculations.

"There has been a lot of interest by Chinese traders in Australian, Indonesian and Canadian coals," said a trader based in Zhejiang province, adding that "we've been actively looking for spot cargoes too." At the same time, Australian producers said that they didn't have enough spot cargoes available to meet demand.

The Platts LV HCC CFR China index averaged $164/mt in Q3, up $16.50/mt from Q2's $147.50/mt, and hit a 10-month daily high of $180/mt on Sept. 23. This also lifted the Platts LV HCC FOB Australia index, which averaged $150.68/mt in Q3, up $6.68/mt quarter over quarter.

Reflecting increased interest in China, Platts published 1,092 bids, offers, trades and tradable indications on a CFR China basis across all metallurgical coal grades in Q3, compared with 580 in Q2.

LV HCC relativities narrow

Chinese interest in LV HCC also impacted PHCC cargoes, albeit to a lesser extent, resulting in higher LV HCC price relativities against the PLV HCC assessment.

On a CFR China basis, relativities for the Platts LV HCC index rose to 91.7% in Q3, the highest in almost four years, up from 88.7% in Q2.

The last time quarterly averages were higher was in Q1 2021, when China implemented an unofficial ban on Australian coal imports.

"There are opportunities for [PHCC] prices to improve on potential cuts to mining operations in China," a Singapore-based trader said, holding a bullish view on prices for CFR China and FOB Australia. "We're seeing possibilities too for further government stimulus to be announced, which could boost steel demand."

Although Chinese traders considered purchasing PHCCs as LV HCC prices increased, the availability of competitively priced Canadian material at Chinese port stocks deterred them from acquiring Australian PHCCs from the spot market, the traders said.

In September, Canadian Premium and Standard offers reached a year-to-date high of Yuan 1,600-1,620/mt ex-stock at northern Chinese ports, equivalent to $189-$191/mt CFR China. In comparison, Australian PHCC prices averaged $202.05/mt CFR China, including Panamax freight costs, a level that was still higher than port-side Canadian coals available in China, according to Platts' calculation.

The Platts PLV HCC CFR China index averaged $176/mt in Q3, up $10/mt quarter over quarter, lagging behind LV HCC CFR China's $16.50/mt growth. Similarly, the Platts PLV HCC ex-stock Jingtang index averaged Yuan 1,482/mt in Q3, up Yuan 217/mt quarter over quarter.

PLV HCC CFR China-FOB Australia spread narrows

Elevated Chinese market prices narrowed the spread between the Platts PLV HCC FOB Australia and CFR China indices to $3.20/mt at the end of Q3, down from $15.50/mt at the start of the quarter. However, Chinese market participants do not expect the spread to invert unless demand for Australian PHCCs strengthens significantly.

"It's not likely because the Chinese market has supply options; no longer are we in the days when half of our imports are from Australia," the Zhejiang-based trader said.

China imported nearly equal volumes of Australian and Canadian coals from January to September, totaling 10 million mt and 8.8 million mt, respectively, according to S&P Global Commodities at Sea data on Oct. 13. Meanwhile, Australian PHCCs received price support from South Asia, with 68 out of 80 deals in the first nine months of 2025 destined for India, Platts data showed.

Q4 outlook hinges on China's stability, India's return

As Q4 began with a quiet trading week due to China's Golden Week holidays, market participants anticipated firm prices, closely monitoring potential policy changes affecting China's steel sector.

Coking coal demand in Q4 is likely to be subdued due to possible steel production curbs and shrinking mill margins, according to Platts Metals and Mining Research. All respondents to the Platts Metals and Mining Research Q4 China Iron Ore & Steel Quarterly Survey, published Oct. 21, expected crude steel production to fall in the quarter, with half not expecting any steel-supportive government policies to be announced. This contrasted with previous surveys, which typically found more upbeat expectations around stimulus measures, and was surprising given the important plenary meeting taking place in October.

"There aren't any strong negative factors yet, but if China curbs pig iron output, then that spells trouble across the ferrous space. If China curbs mining output, then that will keep coal prices firm," a Shanghai-based trader said.

Market participants also anticipated a slowdown in mining operations and transportation later in Q4, as snowfall may affect coal production at north China's key mining regions and Mongolia.

In India, trading sources expected coal demand to recover after the extended monsoon season. Construction and infrastructure activities are typically expected to ramp up post-Diwali, which was on Oct. 20.

"There is a lower likelihood of the market declining," an Indian trader said. "[Steel] production and demand typically increase post-Diwali each year."

Analysts at Energy retained their price forecast for PLV HCC FOB unchanged at $191/mt for the December quarter, "supported by post-monsoon restocking in India. There could also be some buying later in 2025 in anticipation of weather-driven supply disruptions that typically affect northern Queensland in the March quarter," according to a Sept. 30 publication.

Editor: