13 Feb 2020 | 22:48 UTC — New York

Oil rebounds, but LNG remains bearish as market weighs coronavirus demand impacts

Global oil markets were higher for a third straight session Thursday, but LNG prices remained bearish, as the market weighed the demand implications of a steep uptick in coronavirus cases reported overnight.

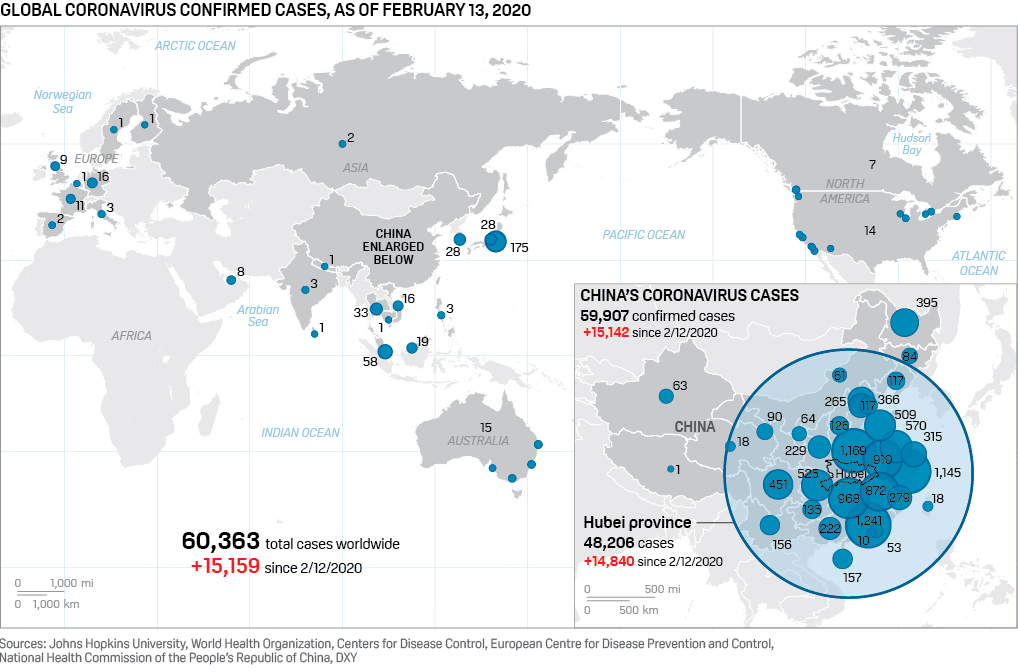

Globally, the number of confirmed cases has risen to 60,364, with 59,826 of those in China, according to the Johns Hopkins University.

In Hubei province, where the number of new cases and deaths were initially reported to stabilizing, an additional 242 deaths were recorded Wednesday, as well as 14,840 new diagnoses, according to media reports citing Chinese government figures.

Travel restrictions were still preventing some employees from returning to work Thursday and factories expected only partial production restarts, with some delaying a return to operations until late February or early March.

Airlines have canceled flights, reducing jet fuel demand.

Click here for full-size image

{kind=link}

Crude prices have fallen steadily since January 20, when news of the outbreak began to take hold of the market. Dated Brent has fallen 18% to $53.115/b, according to S&P Global Platts data, while NYMEX front-month crude futures have fallen below $50/b.

Russia has yet to inform its OPEC partners whether it will commit to new output cuts that were recommended by an advisory committee last week. The recommendation calls for the alliance of OPEC, Russia and nine other countries to tighten production quotas by 600,000 b/d through the second quarter.

But analysts were confident that OPEC+ would take some action to stabilize markets after a number of Russian oil companies said they support extending production cuts at current levels through June.

"Markets are still convinced that this is just going to be a first quarter, possibly April, event that will be predominately impacting China," OANDA Senior Market Analyst Edward Moya said. "Optimism is still strong that the virus will peak."

In LNG markets, the drop in demand has raised the possibility of more Chinese importers reneging on supply contracts, with suppliers expressing concerns about cargo cancellations after state-run CNOOC, China's largest LNG importer, declared force majeure last week.

PRICES

Oil

**Dated Brent was assessed by S&P Global Platts at $56.17/b Thursday, up $1.85 from a Monday nadir, but still 13% off its most recent high on January 20.

**The crude price drop has been seen primarily in the front of the curve, reflecting the expectation that demand losses will be short-lived. The NYMEX crude front-month/six-month spread settled in a 89 cent/b contango Thursday, compared to a $1/b backwardation January 20.

**The Singapore jet crack spread against Brent ended Thursday at $9.04/b, down from $11.34/b January 20.

**The Rotterdam jet fuel crack against Brent ended Thursday at $11.29/b, down from $14.17/b January 20. The New York jet crack ended at $12.839/b, down from $14.19/b January 20.

LNG

**The Platts JKM, the LNG price benchmark for the Northeast Asia region, was unchanged at an all-time low $2.763/MMBtu Thursday, down 34% from January 20.

**The Platts FOB Gulf Coast LNG price has fallen 17% since January 20 to be assessed at $2.138/MMBtu Thursday.

Shipping

**The West Africa to East route for VLCCs was assessed at $16.57/mt Thursday, down $15.85 since January 21.

**The Arab Gulf to China VLCC route was assessed Thursday at $9.36/mt, down $10.50 since January 20.

Metals

**The front-month rebar futures contract on the Shanghai Futures Exchange closed at Yuan 3,380/mt Thursday, down 9% from January 20.

**Platts assessed the 62% Fe Iron Ore Index at $88.2/dry mt CFR North China Thursday, up 20 cents on the day, but down 8% from January 20.

**The London Metal Exchange three-month copper price ended Monday at $5,739.50/mt, down $22 on the day and $531 lower from January 20. Copper is often seen as a barometer for global economic health.

TRADE FLOWS

LNG

**The impact of China's coronavirus outbreak on LNG market is expected to worsen in coming weeks as economic activity in key manufacturing hubs struggles to rebound, keeping a lid on natural gas demand and triggering more LNG trade flow disruptions.

**China's state-owned CNOOC has declared force majeure on LNG contracts.

**CNOOC remains most affected due to the suspension of many factories and transport restrictions, and many domestic LNG terminals were running with high inventories due to the fall in gas demand.

**Qatar is working with China to re-route or reschedule LNG and other energy product deliveries to the Asian country, the country's energy minister said Wednesday.

**A source with city gas distributor Guangzhou Gas said only half of its employees were able to return to work Monday morning, and gas demand from its customers had fallen by around 40% in the past two weeks.

**Australian LNG exports are most exposed to any potential cargo cancellations by Chinese buyers.

**The force majeure and coronavirus impact, combined with a lack of tariff relief on Chinese imports of US LNG, create a perfect storm for already struggling project developers in the US.

**Several US developers have delayed final investment decisions, with one warning it was running out of cash to continue normal operations.

**"It's all happening in real-time. We don't know what's going to happen with cargoes that might not be able to find a home. Some will float. Maybe some maintenance gets moved up," said George Nemeth, director of marketing and business development for Sempra Energy's LNG unit.

**Cheniere has a 1.2 million mt/year supply contract with PetroChina. Cargoes are being lifted, but have been diverted since last year due to Chinese tariffs.

Oil

**The International Energy Agency Thursday slashed its oil demand forecast for 2020 by 480,000 b/d to 100.97 million b/d.

**The outbreak is expected to reduce world oil demand by 1.1 million b/d in Q1 and by 345,000 b/d in Q2, the IEA said.

**Russia has yet to inform its OPEC partners whether it will commit to new cuts that were recommended by an advisory committee last week.

**The recommendation calls for the alliance of OPEC, Russia and nine other countries to tighten production quotas by 600,000 b/d through the second quarter -- more than a third greater than the current 1.7 million b/d cut accord already in place, which should be extended through the end of the year.

**Russian oil companies support an extension of the OPEC+ production cuts through to the end of the second quarter, but at current production levels.

**Demand for Chinese mainstays such as Russian ESPO Blend crude and medium sour Oman is expected to take a hit this month, with trade and economic activity declining.

**Platts Analytics worst-case scenario shows a drop of 4 million b/d in oil demand in February; its best-case scenario shows a drop of 1.5 million b/d in oil demand for February.

**Platts Analytics worst-case scenario shows a drop of 1.125 million b/d in global jet demand in February; its best-case scenario shows a drop of 876,000 b/d in for February.

**Key international airlines have suspended or reduced flights due to the virus.

Shipping

**With the coronavirus outbreak coinciding with the Lunar Year holidays, a lack of demand from China has been putting pressure on tonnage requirements out of the West African region. China is a major buyer of WAF crudes.

**Delays in loading and delivery of cargoes in the tanker, dry bulk and container shipping segments are being reported due to ships being forced to sit idle amid a lack of crew availability.

Metals

**Inventories of major metal commodities have increased substantially in China in recent weeks amid falling demand from China, leading to depressed prices.

**The rise in stocks in China is mainly due to transport restrictions, although there is also an element of seasonality due to a typical fall-off in production during the Lunar New Year period, analysts from BMO Capital Markets and ING Economics said.

**Chinese steel market inventories surged 35% from end-December to 12.38 million mt on January 17, the China Iron and Steel Association said.

**Market sources said depressed demand would see inventories exceed last year's peak of 22.32 million mt by the end of this month, even as some mills announced steel production cuts of 20%-30% from March, partly due to the bringing forward of maintenance.

**Chilean exports of copper to China are continuing unheeded, the country's Foreign Relations Minister said Wednesday.

**Henan province produced 10.96 million mt of alumina in 2019, the third largest after Shandong's 25.68 million mt and Shanxi's 19.96 million mt, according to government data. Henan's output accounted for about 15.1% of the nation's total.

**China's finished steel consumption in February could be up to 43 million mt lower than a year ago due to the outbreak closing down construction and manufacturing activity. This equates to a reduction in pig iron consumption of up to 38 million mt.

**Even if the spread of the virus stops accelerating in February, work at factories and construction sites is unlikely to resume to any great extent until February 24.

**In this case, finished steel consumption is likely to be dented by 31 million-43 million mt this month, equating to 28 million-38 million mt of pig iron. The pig iron demand loss is equivalent to around 47%-64% of last February's output of 60.08 million mt.

**China is the world's biggest steelmaker, producing 996.3 million mt of crude steel in 2019, up 8.3% on 2018 and accounting for 53.3% of global output, a growing share, according to the World Steel Association.

**China's car production and sales will be impacted by the coronavirus in the first quarter, denting demand for auto sheet -- but the widespread closure of public transport during the crisis could incentivize new car purchases once things return to normal, S&P Global Ratings analysts said.

Editor: