15 Jan 2020 | 14:30 UTC — London

European Power Purchase Agreement price report: Platts/Zeigo

Welcome to the first in a series of European Power Purchase Agreement price reports based on data and analysis from London-based renewable energy platform Zeigo. The report is also available for download by clicking here.

As renewable energy subsidies are withdrawn, Power Purchase Agreements are emerging as the main investment driver in the energy transition.

First in the US and now in Europe, PPAs are being used to underpin renewable energy projects that no longer have the security of a feed-in tariff or a Contract for Difference.

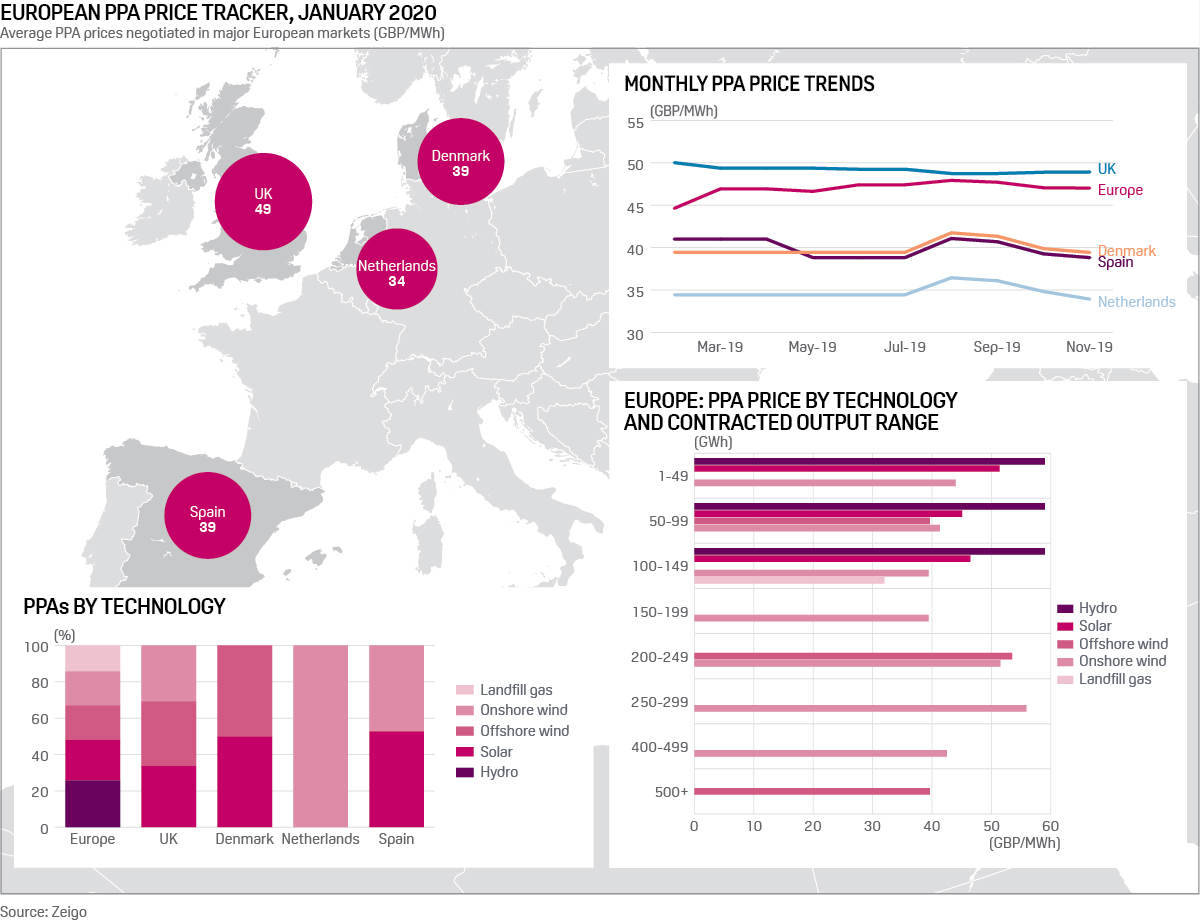

Confidentiality between counterparties makes it hard to assess shifts in PPA pricing, but S&P Global Platts news has partnered with renewable energy data platform Zeigo to shine a light on aggregate bid pricing in four of the most advanced European PPA markets.

The analysis uncovers indicative trends for corporate renewable energy procurement, and some notable average price differences between countries across calendar 2019, with the UK a clear premium market.

Click to see the full-size image

3 GW registered

"The prices shown reflect an average of what developers are seeking in order to proceed to financing," Zeigo CEO Juan Pablo Cerda said.

The data reflect "everything that is live across the platform," with volumes of around 3 GW currently registered with Zeigo, Cerda said.

"For every project a developer uploads, we ask for a minimum and maximum price range. The main point of using a range is to cover different scenarios, from length of the PPA to credit rating. For example, the shorter the term and the lower the credit rating, the higher the price versus a 25-year PPA with the best credit rating, which would give the lowest price," he said.

The disparity between UK and continental PPA prices to some extent reflected the difference in value of renewable energy Guarantees of Origin, Cerda said.

"Although there is a noticeable disparity between prices in the Netherlands and the UK for example, Guarantees of Origin in the Netherlands are trading around Eur7 and with strong subsidies in place, appetite for corporate PPAs from the developer side is not very strong," he said.

UK

The UK is a well-established market for PPAs, with the first corporate agreements appearing more than a decade ago. Significant new deals were announced in 2019, including a consortium of UK universities that will buy directly from UK wind farms, and a 2.5-year agreement between E.ON and RWE Renewables for E.ON to buy close to 3 TWh/yr from RWE wind farms.

Outlook, supply and demand

Wholesale market volatility continues to drive demand for new energy price hedging mechanisms. Wholesale market prices are generally high, with some forecasts suggesting they could double by 2040.

The UK government's phasing-out of subsidies has encouraged developers to focus on corporate PPAs while prompting innovation and the creation of new structures that reduce counterparty risk.

De-industrialisation has left industrial and commercial energy demand fragmented in the UK.

There are very few large single users of power, with the largest businesses being in the financial sector where demand tends to be more distributed -- sometimes complicating procurement.

Denmark

Though Denmark is a well-established market for renewables investment, the country saw its first corporate PPA signed in 2018 between Vattenfall and Novo Nordisk. While deal activity has increased, the Danish market remains a relative laggard in the distribution of relevant PPA negotiation skill sets and access to data.

Outlook, supply and demand

While PPA deals in the Nordics have been dominated by onshore wind, the Danish government's plans for capacity expansion and making future offshore wind projects subsidy-free could drive further growth in offshore wind PPAs.

As in the UK, the phasing-out of subsidies is encouraging more developers to focus on corporate PPAs and prompting market players to create innovative structures to reduce counterparty risk.

Denmark has a concentration of buyers and sectors with significant energy demand.

The Netherlands

The Netherlands has been one of Europe's leading markets for renewable energy, launching its Energieakkoord national energy transition program in 2013. Since then Dutch utility Eneco has opened its largest onshore wind farm, with Google committed to purchasing its total output of 175 GWh for 10years. Meanwhile AkzoNobel, DSM, Google and Philips formed a consortium in 2016 for joint power purchase directly from Dutch renewable projects.

Outlook, supply and demand

Regulatory support continues to be a substantial factor in mitigating risk and supporting corporate PPA uptake. The government's SDE+ program, for example, compensates for differences between minimum regulator-set reference prices, and the market value of energy supplied. The subsidy can be granted in conjunction with a corporate PPA.

Renewable subsidies for new large scale plants that do not fix wholesale energy prices have spurred generator demand for a pipeline of "uncontracted" big projects.

The Netherlands has a concentration of buyers and sectors with significant energy demand.

Spain

Spain has been an important location for renewable energy investment for many years, with an expanding pool of clean energy procurement skill sets, plus growing expertise in PPA design and negotiation. Utility PPAs have led the way for corporate PPAs in Spain, with several subsidy-free projects coming online in 2019.

Outlook, supply and demand

Spain's incomplete integration into the EU energy market and supply pressure from coal mine closures have kept wholesale market prices in Spain between five and six euros per MWh higher than in core continental markets like Germany.

Installed renewable power capacity was relatively stagnant between 2013 to 2016. However, forecasts from SolarPower Europe point to an additional 3.5 GW-4 GW/year of new Spanish clean energy capacity in the next five years.

Demand from corporate off-takers is on the rise, attracted by favourable daytime power prices for solar PV.

Wind prevalent, solar numerous

Wind is the prevailing source in the project selection, "which is consistent with a survey among the companies part of the RE100 initiative," said Bruno Brunetti of S&P Global Platts Analytics.

"Solar, however, is becoming a more important source in PPAs generally, and it is interesting that there are slightly more solar projects on the platform than for wind, although solar projects are for smaller volumes," he said.

This coincided with the recent pick up in solar PV installations and projects across Europe.

"PPA terms of 10-15 years represent the vast majority of projects, but terms of 0-5 years and 5-10 years are also emerging, in line with buyers demand to avoid locking into excessively long-term deals," Brunetti said.

Zeigo's four market price averages reflect the dominance of GB, Dutch, Nordic and Spanish projects in the data. The need for agreements is much less marked in Germany, Europe's largest renewable energy market.

"Results in recent renewables auctions have been quite elevated in Germany, guaranteeing stable remuneration and revenues," Brunetti said.

That might be one of the factors preventing plant developers' demand for long-term coverage or revenue hedging, he concluded.