02 Dec 2020 | 17:40 UTC — Moscow

OPEC+ economic inequalities complicate knife edge oil diplomacy

By Rosemary Griffin and Herman Wang

Highlights

Economic disparity amplifying divides in OPEC+ say analysts

Ruble helps Russia perform better with low oil prices

Iran, Venezuela have highest fiscal breakevens

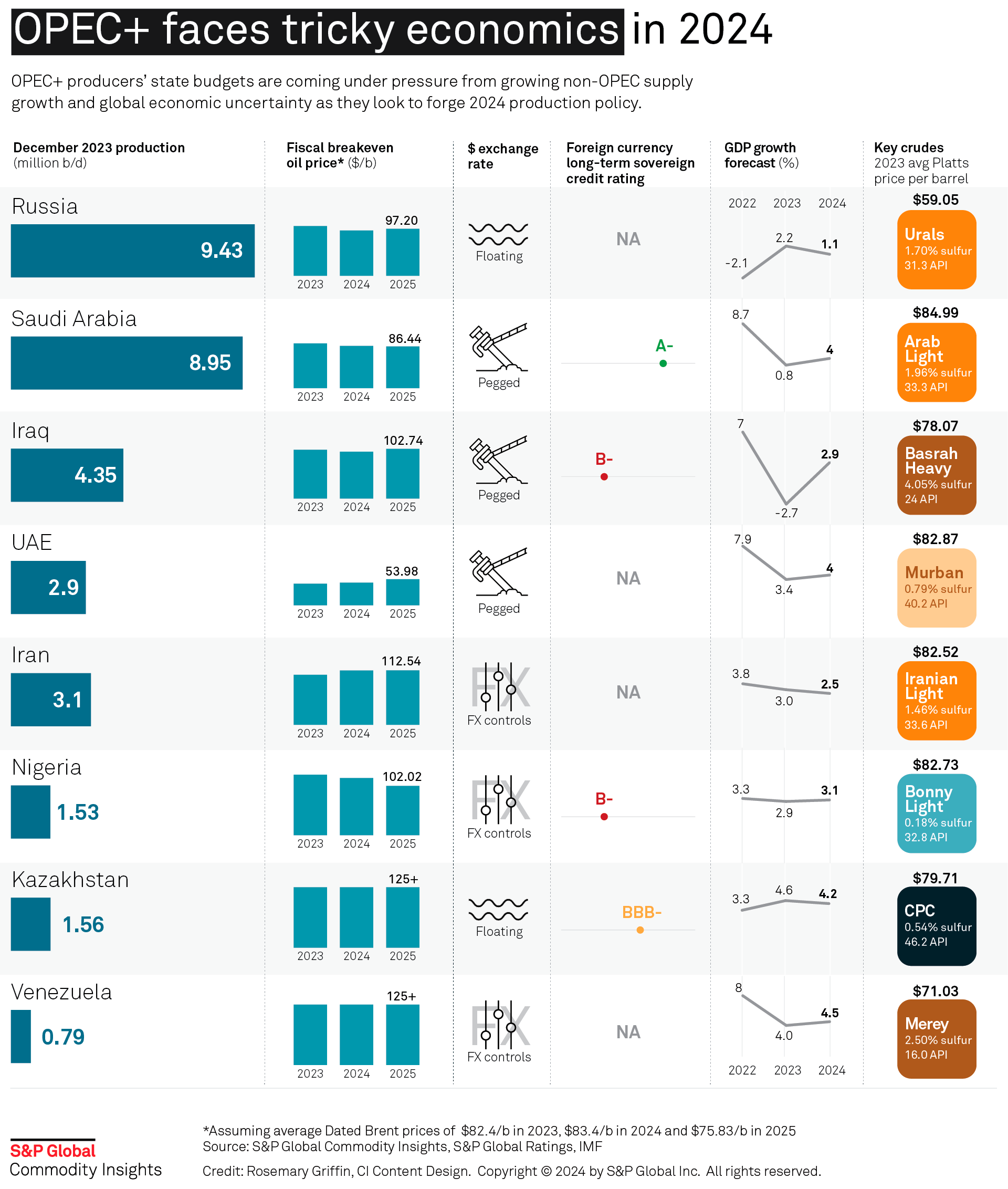

Agreeing on oil quotas isn't the only problem vexing the OPEC+ group. COVID-19 has amplified the economic disparity between poor and wealthy members of the producer alliance, adding to the challenge of finding a consensus to suit all their fiscal oil price breakevens.

Rich producers, such as Saudi Arabia and the UAE, still need oil prices around $80/b to balance their budgets and own large foreign exchange reserves or sovereign wealth funds to absorb economic shocks.

Weaker members including Iraq, Nigeria and Iran have fewer economic buffers and are more vulnerable to low prices.

Related infographic: OPEC+ economic divides complicate oil diplomacy

Meanwhile, Russia, the main non-OPEC partner in the coalition, can better absorb oil shocks than its Gulf Arab allies because of its flexible exchange rate to the US dollar, the currency used to price its crude.

OPEC+ producers have reached an impasse in talks on whether to extend deep production cuts into next year or allow restrictions to ease by close to 2 million b/d from January. At the heart of their dispute is a row over discipline to existing quotas, as some countries seek to restore their economic balance sheets by pumping more oil to compensate for lower prices caused by the global pandemic.

The coalition is scheduled to meet Dec. 3, two days later than originally scheduled, with to give members more time to negotiate.

While Saudi Arabia and many other members are in favor of extending the group's 7.7 million b/d in production cuts through the first quarter, the UAE has demured, insisting that a deal only go forward if countries that previously violated their quotas, such as Iraq and Nigeria, compensate with extra cuts.

That is a difficult ask of the more fiscally strained members, said Andy Brogan, global oil and gas leader of consultancy Ernst & Young, particularly as the world's recovery from the pandemic drags on longer than the alliance had hoped.

"Demand recovery has lagged and everyone has been anxious for some time to get back to pre-COVID production levels and generate more revenue," Brogan said. "In times like these, no one wants to make a disproportionate sacrifice. Unfortunately, after this much pain, any sacrifice starts to seem disproportionate. Pressure to increase production will be relentless."

As for Russia, its comparatively strong resilience to low oil prices compared to other producers may encourage the Kremlin's policymakers to seek smaller cuts for a shorter duration. Sources have told Platts that Russia favors a gradual lifting of quotas from January.

"I think 2020 proved that Russia's economic resilience is very high, not least because of very strong macroeconomic policy settings, including the flexible exchange rate, effective inflation targeting and prudent fiscal policies, which moderated the impact on oil price volatility on Russia's economy and budget," said Karen Vartapetov, lead analyst for CEE/CIS sovereign ratings at S&P Global Ratings.

OIL AND MONEY

OPEC+ ministers were engaged in a flurry of phone calls to try and reach a consensus before the meeting, which is scheduled to start at 2 pm Vienna time (1300 GMT).

A failure to agree would jeopardize the future of the coalition and potentially lead to another bruising price war. But traders appear to believe that a cut extension is the likeliest outcome, sending crude prices back up to their highest since the first week of March.

A key stabilizing factor for Russia is its free-floating currency, with the ruble's value tending to fall against the US dollar when oil prices drop. Russian producers can thereby minimize the impact of low prices on their operations, as their costs are primarily in rubles and export revenues are primarily in US dollars. In contrast, countries with currencies pegged to the US dollar, such as Saudi Arabia and the UAE, see costs remain similar when oil prices and export revenues fall.

S&P Global Platts Analytics' 2020 estimates for fiscal breakeven Brent prices are considerably lower for Russia, at $57/b, than for other OPEC+ producers, including Saudi Arabia, which is estimated at $89/b.

Meanwhile, OPEC's second-largest producer Iraq is proposing harsh austerity measures to cut public spending and a potential currency devaluation to head off an economic crisis caused by the prolonged period of weak prices. Iran and Venezuela -- isolated from global trade by sanctions -- are both suffering hyperinflation and chronic economic decline. According to Platts Analytics, both would both require prices above $180/b to balance their books.

Fiscal breakeven oil prices are not what OPEC+ aspires to, but they demonstrate fiscal strain and the need to find alternative ways to balance the budget.

Despite being better able to cope with lower oil prices, analysts do see Russia as willing to back some extension of cuts into 2021 due to ongoing uncertainty over the demand recovery and the political importance of the agreement.

"OPEC is about more than oil, it's about strategic power. In 2021, I don't think Russia is going to want to be misaligned with the key players of OPEC," said Helima Croft, global head of commodity strategy for RBC Capital.

That leaves OPEC's internal divisions to patch up if a lasting deal is to be made.