23 Jan 2020 | 21:32 UTC — Insight Blog

Nimble Singapore bunker market swiftly adjusts to IMO 2020

The Singapore bunker market recorded its highest monthly sales volume for the year in December 2019, and uptake of low sulfur bunker fuel finally brought some optimism back into the market as it falls in line with IMO 2020.

The International Maritime Organization’s global sulfur cap, which kicked in January 1, has been the major talking point in the oil and shipping industry for the past three years.

The release of preliminary December sales numbers for Singapore bunker fuel last week showed how the market adjusted physically to prepare for the new regulation.

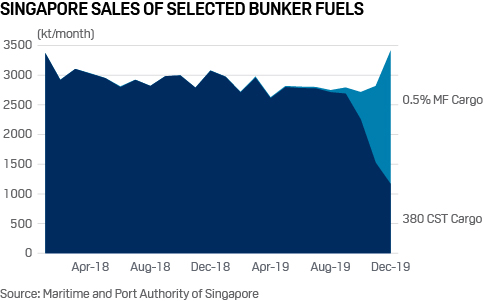

Bunker sales slip in 2019

Maritime and Port Authority of Singapore data for 2019 showed sales volume slipping 4.7% year on year to 47.46 million mt. This was a deeper fall than the 1.65% year-on-year decrease seen in 2018 from the record 50.64 million mt sold in 2017. The headline figure may have concealed an otherwise phenomenal transformation, not achieved at any other port at such scale.

On the surface it might look like Singapore is gradually ceding market share to ports elsewhere globally, as competition increases particularly from China's Zhoushan, which has a high-profile aspiration of becoming a bunkering hub.

Bunker sales from the Chinese port are believed to have reached the 4 million mt mark for 2019, representing about 10% growth from the year before. Bunker fuel prices in China are also expected to be more competitive following the implementation of tax rebates on fuel oil, supporting its push to be a bunkering hub, traders said.

However, a more thorough look at the Singapore bunker sales data shows the material change that happened in the Singapore bunker market during the last three months of 2019.

Traders ready for IMO 2020

Drastic changes in fuel requirements created challenges and new opportunities for many bunker suppliers in 2019, with some saying the last quarter was their best.

Fuel oil traders upped their game by stocking huge amount of compliant fuel or blendstocks on floating storages near Singapore, which are readily available for Singapore bunker demand. More than 25 VLCCs, holding more than five million mt equivalent of the products, were stationed near Singapore at the peak of this activity, according to trade sources. These barrels acted as a buffer to the switch that happened between December and January.

All 44 licensed bunker suppliers in Singapore are able to provide compliant fuels as of mid-January 2020, according to MPA data. Among them, all but two now supply MGO, 29 supply fuel oil with maximum 0.5% sulfur (LSFO), and 11 supply fuel oil with maximum 0.1% sulfur (ULSFO). Meanwhile, 29 suppliers are also hanging on to HSFO business, continuing to make the grade available for ships with scrubbers.

The sales volume of the mainstay fuel – high sulfur 380 cst – halved just between October to December, with its share in total bunker sales volume shrinking to a slender 26% in December, compared with an average 71% share of total sales in the first three quarters of the year.

On the other hand, sales of IMO 2020 compliant low sulfur 380 cst bunker fuel soared to 2.25 million mt in December, accounting for more than half of total bunker sales at Singapore, and about four times that of October sales of this grade. The December sales volume of the fuel was 50 times greater than that recorded in the first three quarters of the year.

The impact of these dramatic shifts in the grades demanded by vessels refueling at the biggest bunker hub in the world were also seen at a pricing level.

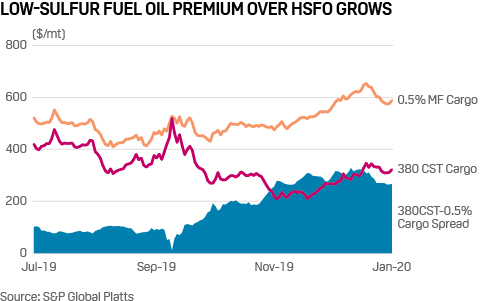

Low sulfur premium balloons

The changing balance of the two major grades was reflected in the wholesale cargo market, where the price spread hit a record average of $303.16/mt in December. This wider spread in turn attracted more low sulfur material into the bunkering hub, and reduced inward flows of high sulfur cargoes.

For comparison, the spread stood at $175.27/mt in October, and an average of $73.04/mt during the first three quarters of the year.

The more niche low sulfur marine gasoil grade, which can also be used as an IMO 2020 compliant fuel, saw a bump in demand, with 2019 sales doubling year on year to reach 3.09 million mt last year.

Total bunker sales of all grades in December came in at about 4.47 million mt, up 3.67% from the same month a year ago, the preliminary data showed. This was the second straight month of year-on-year increase after the 4.34% growth saw in November.

With the high premiums commanded by low sulfur bunker fuels at Singapore, supply of the grade is expected to continue to rise in the coming months. High sulfur 380 CST grade, which used to be the mainstay, is likely to continue to lose market share as the fuel can only be legally consumed by vessels with scrubbers.

The reversal of the roles between these two grades has taken place over a very short period of time at the world's largest bunkering port. That is a robust demonstration of the industry’s ability to adapt to changing market forces, along with the infrastructure it relies on.