22 Jul 2020 | 14:47 UTC — Insight Blog

Despite renewed rhetoric, a 'Gaspec' cartel still faces big challenges

By Andrew Hill

As gas producers worldwide struggle to deal with low prices and weak demand, the idea of market management, OPEC-style, has reared its head again.

Recent comments by Yury Sentyurin, head of the Gas Exporting Countries Forum (GECF), have reignited speculation that an OPEC equivalent gas producers cartel may emerge. Sentyurin in late June stated his view that OPEC was a “model” for the GECF and “Maybe now it’s high time that the gas and oil industry implements the knowledge and solutions of the oil industry.”

He went on to describe a recent meeting with his OPEC counterpart to continue discussions from last October’s bilateral memorandum of understanding as “a new chapter in our collaboration.” This latest rhetoric is in stark contrast to past GECF policy, which had consistently ruled out an OPEC-style approach to supply-side management.

This speculation is nothing new. Since its formation in 2001, the issue of the GECF’s metamorphosis from mere debating forum to fully fledged OPEC equivalent has cropped up with almost predictable regularity. However, the emergence of a gas cartel has never appeared to be a particularly likely development, though it now appears more feasible than ever before due to the evolving nature of the global gas sector.

Go deeper: Explore S&P Global Platts insights and events with Platts LIVE

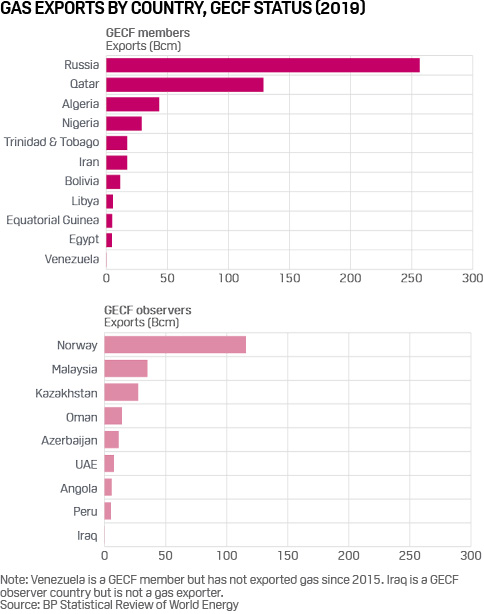

On paper, the GECF is a credible force given that its members control around 58% of global gas reserves and 35% of production. When observer members are factored in, the figures rise to over 67% of reserves and 44% of production. However, sheer weight of numbers is no guarantee of either effectiveness or supply-side cohesion, as the 60-year history of OPEC testifies.

The ongoing double-edged sword of record-low gas prices and stagnant demand growth faced by gas producers has been exacerbated by the coronavirus pandemic. As such, the incentive for producers to engage in supply side management to raise prices has never been stronger. Two key factors that had previously thwarted the GECF’s supply side management ambitions have diminished markedly in recent years, thus theoretically boosting the prospects of a gas cartel.

- Globalization of the global gas market – for decades the global gas sector was defined by distinct geographic supply bubbles – what happened in one bubble had little, if any, impact on the other bubbles elsewhere in the world. However, in recent years, the continued evolution of global gas market dynamics has resulted in market (and more recently price) convergence which has created one single global gas market. With LNG now meeting 12.3% of global gas demand, and close to 50% of trade flows, the global rather than regional credentials of the gas market are self-evident. As such, any form of production programming or supply side management would be easier, and more effective, in a more globalized market than in a series of regional markets.

- Oil indexation – while by no means extinct, oil indexation has long ceased to be the primary mechanism for gas pricing. This is in stark contrast to the situation at the birth of the GECF in 2001 when long-term contracts of up to 25 or 30 years in duration were commonplace. A more flexible, hub-based set of wholesale markets around the world facilitates much greater flexibility in production programming compared with long-term, inflexible contracts.

However, despite the latest rhetoric from the GECF, significant obstacles remain present that are likely to considerably thwart its ambitions.

- Differing agendas and difficulties in reaching consensus – the membership of the GECF is both diverse and disparate. In terms of both reserves and production, Russia is by far the largest member of the GECF, controlling 19.1% of global gas reserves and 17% of global production, making it to the GECF what Saudi Arabia is to OPEC. Conversely, the eight smallest members (of 11 full members) collectively control just 10.1% of global gas reserves and 7.4% of production. As such, an inevitable tension between the smaller members with a price maximization incentive, and the larger members who may prefer a “volume over value” strategy, has the potential to emerge. This has repeatedly been seen within OPEC over the past 60 years. Finding consensus among a gas cartel would likely be similarly challenging.

- Allocating production quotas – another key challenge for the GECF would be in finding a way to allocate production quotas. Securing consensus on an overall production quota would be problematic, as would the allocation of individual quotas among members.

- Consumer backlash – it is unclear how consuming nations would react to the formation of a gas cartel, however strong opposition is highly likely. Given that Europe is a net gas importer, and very dependent on many of the GECF members, the European Union is likely to object ardently, potentially leading to the threat of trade sanctions or anti-cartel legislation.

Despite a pressing need among producers for higher gas prices, and the changing structure of the global gas market, considerable challenges to the formation of a gas OPEC remain, making it unlikely in at least the short to medium term.