31 Oct 2018 | 17:09 UTC — Insight Blog

Insight: Steel, aluminum and coal reveal a 'Trump premium'

Almost two years since it began, what has been the impact of the administration of US President Donald Trump on commodity prices? Joe Innace takes a look

If higher commodity prices reflect US presidential campaign promises kept, then President Donald Trump has already delivered on three fronts as he approaches two years in office.

The president campaigned hard on promises to help directly the US coal and steel industries and American manufacturing. It worked. Trump won key steelmaking, mining and manufacturing states like Ohio, Pennsylvania, West Virginia, Michigan, Indiana and Wisconsin.

It took a good year or so for Trump to settle in. Until November last year, most commodity prices had struggled to see their averages match, or surpass, the levels on the last day President Barack Obama held office. But with the passage of US tax reform legislation, an “America First” trade agenda in place and on full global display, manufacturing expanded and the domestic economy saw 4.2% GDP growth in the second quarter of 2018. In turn, this created more demand for energy commodities.

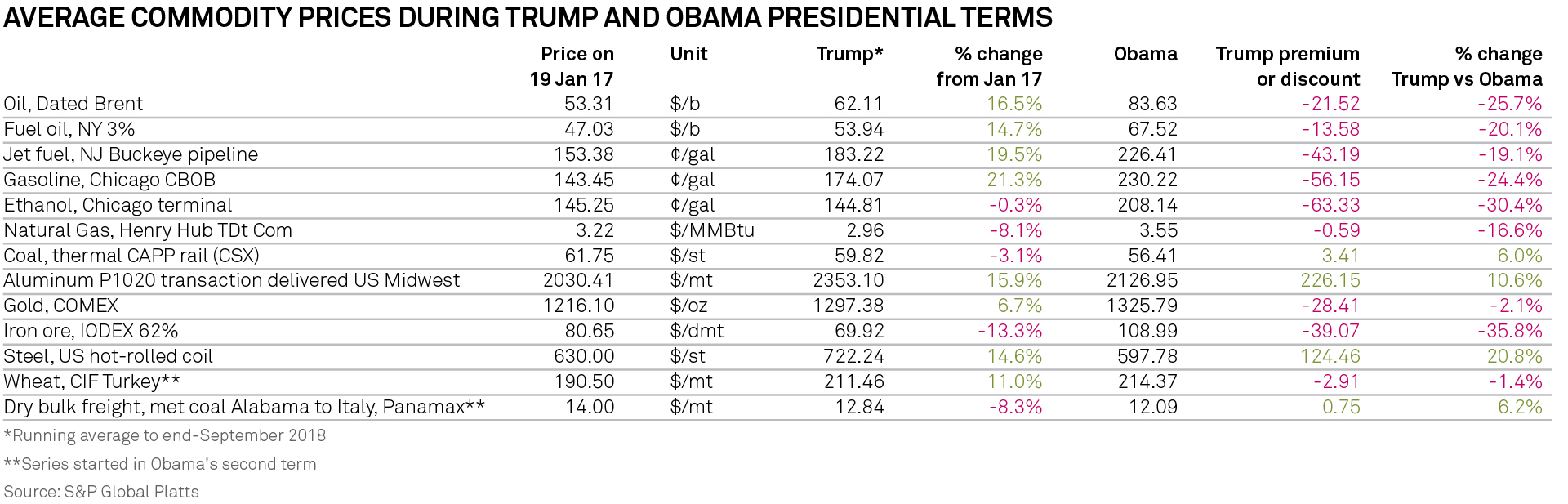

A group of 13 commodity benchmarks has been used by S&P Global Platts to track pricing performance during Trump’s term versus Obama’s eight years in office. Although fundamentals and a range of other factors have greater influence on commodity prices than US presidential policy alone, the exercise is intended to shed light on how prices and politics often intersect, where they’ve been, and perhaps to get a handle on where they might be going.

Ferrous, coal set the pace

After a slow start for most of 2017, steel, aluminum and coal benchmark prices were all averaging higher for the Trump period (January 20, 2017−September 30, 2018) than during Obama’s two terms in office. Largely because of an aggressive trade policy marked by the imposition of tariffs on steel and aluminum imports to the US, prices of both metals in the US market are up considerably compared with their average during the Obama years.

It’s not a stretch to acknowledge the metals price increases as a “Trump Premium.”

The price of US-made steel hot-rolled coil averaged $722/short ton through September 2018 under Trump, while it averaged $598/st during Obama’s two terms – a boost of nearly 21%.

The “all-in” price of primary aluminum in the US market is up almost 11% since Trump became president. This includes both the underlying, global London Metal Exchange price plus the S&P Global Platts US Midwest Premium that reflects regional supply/demand fundamentals and local logistics costs. It averaged $2,353/mt through September 2018 under Trump, compared with $2,127/mt under Obama.

And while coal prices in the US have not benefited from such direct trade policy as the tariffs implemented for steel and aluminum, the commodity has been buoyed by a president who embraces a pro-coal ideology. The benchmark price of railed Central Appalachian thermal coal through September 2018 has averaged nearly $60/st while Trump has been in office, compared with an Obama-era average of $56.41/st – about 6% higher.

Surging energy prices

Most energy prices with Trump in office still lagged the average prices posted during the Obama years by about 22% at end-September 2018. But energy prices started to gain during Trump’s second year –with the exception of natural gas – to the point where they are now about 18% higher on average than the day before Trump took the oath of office.

Unlike the Trump premium in coal, steel and aluminum, however, these other commodities in the US market went along for the ride – more recently getting swept up by strong economic growth and manufacturing activity.

Leading the way — to the chagrin of American drivers — is CBOB gasoline, Chicago. From January 2017 to September 2018, this benchmark was up more than 21% to an average of 174.07 cents/gal. This compares with the day before Trump took office, when Obama left it at 143.45 cents. Chicago gasoline, however, averaged 230.22 cents/gal during Obama’s eight years, so it remains 24% lower under Trump.

With Trump as president, New York fuel oil through September 2018 was averaging $53.94/b, up nearly 15% since the day before he took office. But it also lags the Obama two-term average of $67.52/b by some 20%. Similarly, jet fuel (New Jersey Buckeye pipeline) is up 19.5% since Trump became president to an average for his term through September of $183.22 cents/gal, up from the 153.30 cents/gal contrails of Obama’s last day as president. Jet fuel pricing, nonetheless, averaged 226.41 cents/gal during Obama’s eight years, so recent Trump-era pricing still lags by about 19%.

Average prices for ethanol and natural gas through September 2018 under Trump have yet to exceed Obama-era pricing, mostly owing to abundant supply. But going forward, ethanol will be one to watch because Trump has directed the US Environmental Protection Agency to authorize year-round E15 sales. E15 is gasoline blended with 15% ethanol, currently restricted in the summer months because of gasoline volatility rules. The EPA aims to adopt final rules for fuel economy standards by March and year-round sales of higher ethanol blends by May 2019.

2019 growth in doubt

The US economy’s 3.5% GDP growth in the third quarter follows 4.2% growth in Q2, which was loudly trumpeted by the US administration. The latest GDP data came on October 26, just days ahead of the US midterm elections, and positive economic news is also good news for Trump-backed House and Senate candidates. Steel and other commodities benefit from such a rate of economic expansion. Steel demand, for example, tends to increase substantially when GDP grows at a rate greater than 3%.

“You’re seeing GDP and now wage growth; this drives consumer demand and gets you in a virtuous cycle, and that’s where we want to stay,” said Thomas Gibson, president and CEO of the Washington-based American Iron and Steel Institute.

But staying there may prove tricky in 2019, as the trade tensions of 2018 have the potential for a delayed reaction on the downside in a global economy. The International Monetary Fund in October lowered its forecast for US growth in 2019 to 2.5%, while leaving its projection for this year unchanged at 2.9% – after factoring in the potential impact of tariffs imposed by the US and retaliatory actions by other nations.

S&P Global Market Intelligence reported on the IMF forecast, noting the organization’s view that short-term risks to the financial system had increased, and that those risks could increase significantly if vulnerabilities in emerging markets and global trade continued to rise.

It’s the economy, stupid

There are eight full years of commodity price data for Obama’s two terms, compared with just two years for Trump. The past two years, many would agree, have been far more tumultuous than tranquil. Will we have like-period price data sets to continue comparing? Trump will indeed run for re-election in 2020, and many pundits are already citing Bill Clinton’s campaign advisor James Carville’s oft-quoted phrase, “it’s the economy, stupid,” as the determining factor.

Trump’s executive actions to impose import tariffs on steel and aluminum are likely to remain in place – although there may be country- and product-specific deals negotiated between now and the next presidential election, as he continues to use the trade hammer to forge new pacts. This America First trade and manufacturing policy played well on the campaign trail in 2016 among many voters in the Midwest states where steel and aluminum is produced and consumed.

Ensuing tax, trade and regulatory reform energized the US manufacturing base to the point where the National Association of Manufacturers’ monthly index reached an all-time high of 63.6 in June 2018. But it has been slipping ever so slightly since then. Might this reflect some waning enthusiasm on the part of steel and aluminum end-users that have seen their manufacturing costs rise – either by paying tariffs or higher prices for domestic material? “The tariffs are starting to take a bite out of profitability,” one purchasing manager in the chemical sector said.

In October the NAM’s Outlook Survey, which indicates the percentage of small-to-large manufacturers who are upbeat about their own company’s outlook stood at 92.5%, after posting an all-time high of 95.1% in June. That’s still a very strong positive indicator, despite some very minor erosion.

The early consensus is that if the US economy remains strong in 2019–2020, growing at a rate of 3% or more, then Trump should win another term. But sustaining such an economic growth level – or anything close to it – over the next 24 months ahead of the November 3, 2020 election is a big ask.

As such, US commodity prices will be among the interesting indicators to keep watching.