26 Nov 2018 | 16:47 UTC — Insight Blog

Insight: EU carbon market stages comeback in 2018

By Frank Watson

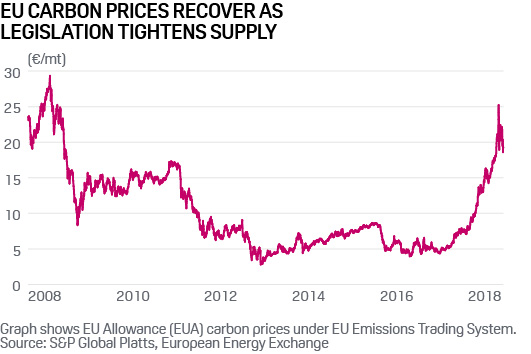

The carbon market in Europe made a big comeback in 2018 after years of stagnation, with prices of European Union allowances more than quadrupling to above €20/mt ($23/mt) after lawmakers overhauled the system’s rules for the period after 2020.

Higher carbon prices are likely to boost the profitability of companies operating nuclear, wind, solar and hydro-electric power plants, driving further growth in renewable energy capacity in Europe. They also signal a long-term drop in the use of the most emissions-intensive fuels for power generation, hard coal and lignite, and provide a stimulus for innovation in low-carbon industrial goods and processes.

After years of being flooded with surplus carbon allowances, sharp supply cuts starting in 2019 look set to reposition the EU Emissions Trading System as the principal tool to decarbonise Europe’s economy over the long term.

The overhaul of Europe’s carbon market not only tilts the economics of electricity generation away from fossil fuels and towards cleaner power, but it also puts wind in the sails of carbon markets in general. That sends a clear message to other regions grappling with the same pervasive energy trilemma: making energy secure, sustainable and affordable.

The road to 2019

The road to 2019 has not been an easy one. The very idea of carbon markets came close to redundancy along the way, as low prices persuaded some EU member states to go it alone on carbon pricing policies.

From a pre-financial crisis high of over €30/mt in 2008, carbon prices crashed during the downturn that followed. That’s because the supply of carbon allowances was fixed under the scheme, while demand was linked to actual CO2 emissions, which fell as demand for electricity and CO2-intensive products collapsed. Carbon prices dipped to as low as €3/mt in 2013 in the wake of a second economic slowdown in Europe, threatening to make the ETS irrelevant as a driver of decarbonization.

This problem of excessively low carbon prices was not just the result of global economic conditions. It was further compounded by overlapping EU energy and climate policies, including targets for increasing renewable energy and energy efficiency for 2020 and 2030. Far from pulling in the same direction, some of these energy and environmental policies directly undermined the price signal produced by the ETS.

Under a cap-and-trade system, CO2 emissions fall as a result of a declining annual carbon cap, not as a function of the carbon price. In a free market for rights to emit CO2, the environmental benefit is delivered through the cap, with the price determined by market forces. Still, for the European carbon market to send meaningful investment signals, a better balance was needed between supply and demand.

Major interventions

A series of major market interventions followed as Europe’s lawmakers tried to avoid a complete collapse of the system. Early examples of this included “back-loading,” a move to postpone the release of 900 million EUAs in government auctions from 2014 to 2016. While this measure avoided carbon prices falling to zero, it only addressed a symptom, not the underlying problem: prices are vulnerable in a market in which supply cannot react to demand.

Brussels authorities understood that to make the ETS future-proof, ad-hoc supply-side interventions would not be enough – the market needed a mechanism that would make it resilient to future demand shocks by controlling supply automatically.

Cue the second major intervention: the Market Stability Reserve. The MSR is a mechanism to withhold surplus EUAs from the market, reducing any current or future oversupply. The MSR was agreed by the EU’s co-legislature in 2015 and strengthened under legislation passed in 2017. It is set to curb the volume of EUAs in circulation, which represents 1.655 billion mt of CO2 equivalent, by 24% per year starting in January 2019. Going forward, the MSR is expected to react to any factor that might increase the volume of carbon allowances in circulation by withholding a fixed proportion – 24% of the surplus – from government auctions in the following 1−2 years.

The MSR’s expected impact on supply has led some analysts to forecast a supply crunch in 2019−2022, as net supply in the market falls below the volume needed for power generators to hedge forward power sales, forcing CO2 abatement. Anticipating this cut to supply, buyers increased their activity in 2018, while sellers had little reason to offload volume. This pushed carbon prices to well above €20/mt by August, and the gains were further compounded as the looming supply cuts attracted financial players back into the market following a long absence.

In addition to the MSR, EU lawmakers agreed on other changes for the period 2021−2030, including a steeper 2.2% reduction in the annual carbon cap, as well as other rule changes including more targeted free allocations for companies in trade-exposed sectors. The EU’s carbon market legislation also includes provisions that allow for a future review, opening the way for further intervention to ensure the market functions as intended.

Looking ahead

What does the future hold for the European carbon market? In the power sector, it has widely been assumed that coal-to-gas switching would arise as a result of higher carbon prices – but as 2018 demonstrated, this hasn’t always been the case.

Coal-to-gas switching has not been happening so far in 2018, quite the opposite. European gas prices were high in late 2018 due to volumes going into storage ahead of winter, declining Dutch production and strong Asian markets for LNG. Those high gas prices squeezed profit margins on gas-fired power plants, helping keep emissions-intensive coal-fired plants ahead of gas-fired units in the merit order for power generation.

In effect, instead of coal-to-gas fuel switching, the European power market has been experiencing coal-to-renewables switching. Wind power is increasingly pushing coal plants off the grid on windy days, while coal plants come back onto the grid on cold, still, winter days when heating demand is high and wind fails to materialise.

This trend is likely to become more pronounced as solar and wind capacity increase across Europe, with weather playing a larger role in pushing older coal and gas units out of the money.

In general, higher carbon prices have several implications: expect to see renewable energy taking a bigger slice of the electricity market in Europe; higher wholesale power prices; a long-term drop in the use of hard coal and lignite for power generation; greater innovation in low-carbon industrial processes; and increased investment in energy storage and energy efficiency.

While the MSR will tighten the supply side of the carbon market, demand-side factors could yet weigh on carbon prices and keep any severe price increases in check.

“The MSR itself does not raise EUA prices, but it makes the market shorter,” said Jeff Berman, director of emissions and clean energy at S&P Global Platts Analytics. “This should lead to higher EUA prices, but if emissions reduction costs fall, then EUA prices could also remain low,” he said.

On the demand side, Germany – the largest power market in Europe – has appointed a commission to work on ways to move away from coal and lignite. This is expected to result in a managed closure process for its most CO2-intensive power plants.

However, Germany cannot achieve this goal quickly. The country is already phasing out low-carbon nuclear power for other environmental and safety reasons. This means any move away from coal must happen on a gradual timeline, allowing renewable energy to fill the gap left by nuclear, keeping coal in the mix for several years to come. Other downside factors include a potential fall in natural gas prices, which could allow coal-to-gas fuel switching to happen at a lower carbon price, thereby cutting CO2 emissions and demand for allowances.

There are also other potential challenges for the carbon market in the wider international context: if other countries outside Europe fail to press ahead with ambitious climate policies, high carbon costs in Europe could become problematic for the EU to sustain. Clever diplomacy and careful rule-making may be required to avoid European businesses facing undue competitive distortions.

But could the carbon market again suffer a major price crash – for example, if another economic crisis occurred? That’s unlikely. When drafting the MSR legislation in 2017, EU lawmakers designed the reserve to react automatically to quantitative demand-side fundamentals. In effect, the MSR future-proofs Europe’s carbon market by controlling the volume of allowances available to regulated companies. This makes it very unlikely that a future carbon price crash could occur, and is a key reason why banks and other financial players become confident enough to move back into the market on the buy-side in 2018.

That the carbon market has survived political opposition among some industries and EU member states, as well the global financial crisis, is remarkable. But it is also testament to the resilience of the core idea: Europe wants to build a low-carbon economy by the second half of this century without breaking the bank. This long-term effort needs coordinated policies that can deliver emissions reductions at the lowest cost. It also requires long-term price signals that have the power to shift capital investment on to a sustainable track at scale. Overcoming the tension between those two goals has been a fundamental issue for the EU carbon market since it became operational in 2005.

After years of oversupply and prices that were too low to be meaningful, the carbon market has now been strengthened and positioned to play a key role in achieving the EU’s goals. The direction of travel is clear.