14 Sep 2018 | 23:35 UTC — Insight Blog

Will 2020 be a game changer for bunker credit?

By Ben Notcutt

The twin pressures of tough financial times for the shipping industry and the likelihood of more expensive fuel in 2020 are bringing the issue of bunker fuel bills into focus for the industry.

Many shipowners and operators have gone through difficult times since the global economic crash of 2008. There have been numerous bankruptcies, heavy losses, and the revaluation of assets on balance sheets across the industry.

This has not just affected small companies. Perhaps the most prominent failure of recent times was the Korean liner company Hanjin Shipping which some regarded as too big to fail, but which was ultimately declared bankrupt in early 2017.

2020 will be yet another pitfall for ship operators. Bunker fuel represents the most prominent voyage cost, and bills are set to increase substantially overnight, presenting a further stress point.

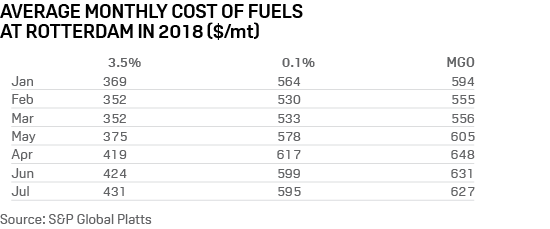

At present 3.5% sulfur, 380 CST fuel oil makes up the lion’s share of bunker fuel sales. Once the IMO’s sulfur cap of 0.5% comes into effect in January 2020 the majority of ship operators will have to turn to more expensive fuels such as marine gasoil and very low sulfur fuel oil to remain compliant.

Based on costs in July at the European bunkering hub of Rotterdam, this would mean a price increase of around $196/mt if a ship operator were to switch to MGO and $164/mt if they switch to 0.1% (ultra low) sulfur fuel oil.

CRUCIAL CREDIT

A large proportion of bunker fuels sales are made on credit. Where this occurs, bunker sellers contribute to the working capital and liquidity of ship operators, and this financing has become an important part of the operators’ financial structure.

For sellers, 2020 is a huge shake-up of their business, not only in terms of products sold and bunkering infrastructure, but also from the perspective of credit. They will face a sudden and substantial increase in demand for credit from customers turning to more expensive fuels.

This could present a period of heightened customer credit risk, and also test their own resources as they are asked to finance the increased credit requirement.

It raises the questions, will the bunker suppliers and trading houses be willing, or even able, to finance this sudden credit demand shock?

TWO APPROACHES TO CREDIT

Bunker sellers come in all shapes and sizes, ranging from oil majors and the largest independents, through suppliers and traders of varying means, all the way down to one man bunker trading businesses.

Understandably these players have differing capabilities, roles, and attitudes to risk. Given this, there are likely many different answers to the questions posed.

Those at the top of the bunker seller’s pyramid may continue to play it safe. The credit manager of a large independent supplier said their company had been increasing volumes with a top tier of ship operators, mentioning some top liner companies, dry bulk, and tanker operators. It had reduced business with a perceived riskier tier of small shipowners and operators.

2020 was a factor in this strategy, but was not the only driver. Difficult market conditions for bunker sellers had also dictated some revision of operations. Nevertheless, this supplier had already increased credit lines for the top tier operators with 2020 in mind. In some cases multi-million dollar credit lines had more than doubled.

An alternative perspective was provided by the credit manager of a bunker trading company. They acknowledged that 2020 could result in heightened credit risk, but thought that it was likely a short-term phenomenon. In the medium-term they envisaged that ship operators would manage to pass bunker costs to their own customers.

Credit management is a continual process and sales are monitored case by case, but the manager indicated that in the higher price environment special attention would likely be paid to the bottom 10% of the customer base, customers which were already making late payments.

It was not that credit would necessarily be cut for such customers, but perhaps that the trader would decline to increase credit lines initially. A suggested solution was to offer a mixture of credit and secured terms, but it was acknowledged that in the latter scenario the customer may prefer another provider that would offer credit.

The credit manager said it remained unclear what solutions its customers would be using in 2020, whether they would be using low sulfur fuels or utilizing scrubbers, and this meant that overall decisions about credit lines were yet to be taken. Some credit lines were increasing, but this was because bunker prices have been rising.

However, this company did have 2020 in mind. Its main focus had been on strengthening its own balance sheet, so that when the call for extra credit inevitably arrives it will be ready to provide it should it wish to.

A RETURN TO HIGHER MARGINS?

For the last few years the bunker seller’s market has been characterized by intense competition.

In mid-2014 the price of oil plummeted and bunker prices soon followed. Low prices meant sellers of all types were able to stretch working capital further, and took advantage of this by aggressively chasing business. Further, the barriers for entry to the sector have remained low, encouraging more to join.

Broadly the result has been greatly diminished margins for all. To illustrate this, one source indicated that presently you might see 10 traders competing to stem one ship, and said about five years ago the margin for a single deal might be $10/mt, whereas today it could be a matter of cents.

This situation is viewed as unsustainable, and in this environment some sellers have experienced losses, and several have even had to reorganize operations.

Change could be coming, as high prices could conceivably alter competitive advantage among sellers. Bunker prices have already been trending upwards, placing more demand on seller’s working capital. This would only be intensified in 2020.

Returning to the bunker seller’s pyramid, those at the top will be best placed to meet the challenge, having greater existing resources to draw on, often sizeable bank credit lines in place, or being part of big organizations able to offer support.

Moving down the pyramid players may begin to see their resources stretched, but those at the bottom could suffer most. Higher prices could curtail their spending powers and reduce their competitive abilities.

We found this to be a common view among market participants we have spoken to. For some it would likely be a welcome development, but for others not so much.

SHIP OPERATORS ALSO CHOOSE

The collapse of the bunker supply and trading company OW Bunker in November 2014 was a seismic event for the market. Some ship operators were caught in the uncomfortable position of having to pay for bunker stems twice in cases where OW had acted as a trader, once to OW’s bank, and again to the physical bunker supplier involved.

In the aftermath some operators chose to source bunkers directly from suppliers where possible, cutting out traders, and the perceived risk of exposure to a similar event. To this day where an operator uses a trader, it is understood to be quite common for them to ask for confirmation a supplier has been paid before paying the trader.

As bunker sellers could also feel some pressure from 2020, we asked our contacts if they thought operators may also be reviewing their suppliers. Those we spoke to thought it likely, but not necessarily for the same reasons as after OW.

The bunker supplier credit manager was of the view that many ship operators would opt to use a narrow range of bunker suppliers because of concerns over fuel compatibility, which will be a more pressing issue post 2020.

The bunker trader credit manager agreed this was possible, but thought that with their own balance sheets to think about, not all bunker suppliers would want to shoulder an increased credit burden alone.

On occasion bunker traders are already asked to insert themselves into a deal in order to be the credit provider. This was said to be high volume, low margin business, but was thought one way traders might offset a possible reduction of business.

Further, it was pointed out that many companies working in tramp trades or on projects will still require traders, so any thoughts of the demise of bunker trading are premature.

It was believed that given concerns about fuel compatibility ship operators would increasingly seek out trusted traders and suppliers, with the focus more on product and service quality, where it may have previously been on price. The current reports of contaminated bunkers were highlighted as a case and point.

TO SUM UP

We are only scratching the surface here, but it seems that bunker sellers will be prepared to increase credit lines for 2020, in some cases having done so already.

However, credit decisions continue to be judged case by case, and while there could be a more flexible credit scenario for the largest ship operators, there could be a more pressured environment for smaller, riskier market participants.

Inevitably, the largest bunker suppliers will be best placed to meet the increased requirement for credit. Small sellers are expected to come under pressure, as they may not have the resources to compete for the volumes they have managed in a low price market.

This could go some way to reshaping the bunker seller’s market, which some would welcome, especially if it alleviates low margins. Fuel compatibility and quality are also factors that could do this.

2020 doesn’t just present risk for bunker sellers and buyers: risks extend to the whole market. Everyone needs to pay attention to their counterparties, whether they are extending them credit or not. It pays to remain vigilant.