22 Jul 2019 | 11:00 UTC — Insight Blog

Commodity Tracker: 5 charts to watch this week

S&P Global Platts editors’ pick of unfolding commodities trends. This week, tight US gasoline supply incentivizes imports, high-tech industries drive tin demand and Iranian oil exports hit new low. Plus impacts of Europe's heatwave and China key economic data on energy and commodities.

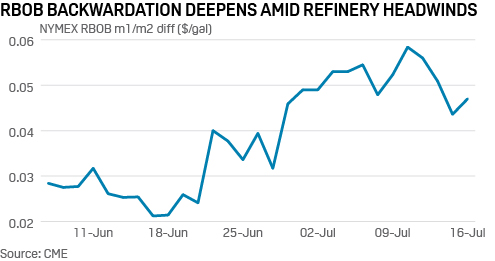

1. US gasoline output curbs driving NYMEX RBOB backwardation

What’s happening? RBOB gasoline structure has firmed in recent weeks amid refinery issues on the US Atlantic Coast that are limiting local gasoline production and adding stress to regional supply during the high-demand summer driving season. Philadelphia Energy Solutions announced it would shutter its 335,000 b/d refinery outside of Philadelphia after back-to-back fires in June resulted in the destruction of the facility's alkylation unit. In early July, the fluid catalytic cracker at Phillips 66's 238,000 b/d Bayway refinery in Linden, New Jersey was taken offline for a week for unplanned maintenance.

What’s next? Widened arbitrage spreads to Northwest Europe should incentivize an influx in gasoline imports, mitigating the long-term impact of the local refinery slowdown. But in the short term the region remains vulnerable to supply shocks.

2. Tin supply deficit opens up as high-tech uses proliferate

What’s happening? The tin market is set to continue in deficit on recent lack of investment in new mine capacity. Tin fell out of favor with investors after its price collapsed during the international tin crisis of the 1980s, when the US sold off strategic stocks and Brazil flooded the market. Now demand is growing for tin as a high-tech solder: it’s used in 5G, battery, robotics and other electronic applications and it’s back on the US strategic metals list.

What’s next? Of a 357,000 mt/year global demand foreseen this year by the International Tin Association, around 20% comes from recycling. UK-based mine developer Strongbow Exploration expects lower amounts from recycling in future, meaning new mine and smelting capacity will be needed as demand is seen growing 2-3% a year. Major existing mines in Asia face depletion and upwards price pressure may intensify after a price surge early this year, followed by a more recent dip attributed to ore quality factors. New mines and smelting capacity are emerging in countries including the UK, Kazahkstan and Rwanda.

3. European power markets brace for heatwave

What’s happening? What a difference a year makes. The 50% decline in gas price over the last 12 months is clearly evident in UK day-ahead power prices. The UK increasingly relies on gas-for-power not only to balance wind but also to replace coal. Summer to date we’ve seen much lower power prices on year, but also more volatile pricing as reduced baseload nuclear has been replaced by a mix of intermittent wind and greater use of flexible gas.

What’s next? Throw a low-wind heatwave into the mix, as forecast in France this week, and we are likely to see northwest European power prices ramp up on air conditioning demand. An extended heatwave last year saw operating restrictions on French river-based nuclear reactors, reversing power flows on the UK-France IFA interconnector at times and supporting prices both sides of the Channel.

4. Iranian oil exports fall to historic lows on US sanctions

What’s happening? Iran's oil exports slumped to under 500,000 b/d in June, the lowest in modern history, as US sanctions squeeze the OPEC producer to fill a growing flotilla of tankers with nowhere to go. Shipments of Iranian oil fell to 448,633 b/d in June from 901,134 b/d in May, data from S&P Global Platts trade flow software cFlow shows. Iranian crude and condensate exports, which averaged about 2.50 million b/d in June last year, have now fallen by just over 2 million b/d in the past year, data from shipping sources and provisional tanker tracking shows.

What’s next? Iran’s oil production could slide further once its storage options fill up. Complicating the picture of Iran’s export flows, a number of its state-owned oil tankers have stopped broadcasting their geographical positions over recent months. S&P Global Platts Analytics expects Iranian exports to average 450,000 b/d in the second half of 2019.

5. Weak property data spells trouble for Chinese steel mills

What’s happening? Property construction accounts for roughly one-third of China’s steel consumption, and drives demand for a host of other metals and raw materials. As such, government data released last week showing that land area (for housing) purchased over the first half of this year was down 27.5% indicates the demand pipeline could be thinning out. Further, floor space of houses sold was also weak, while infrastructure investment – viewed by many as the likely saviour of steel demand in 2019 – barely grew at just 4%. Prices of rebar – the key construction steel product – were down around 10% on a year earlier in June.

What’s next? Beijing has said it wants “manageable” property sector growth and will support it to ensure stability. Construction activity is robust, up 10% on last year, but any slowdown from those levels could have an adverse impact on steel prices. With iron ore prices still high, Chinese mills could come under intense pressure if the property construction sector weakens further.

Reporting by Chris van Moessner, Diana Kinch, Henry Edwardes-Evans, Robert Perkins, Paul Bartholomew, Oceana Zhou and Jing Zhang

Edited by Emma Slawinski