13 Jul 2020 | 15:08 UTC — Insight Blog

Commodity Tracker: 5 charts to watch this week

Revisions of future oil and gas price assumptions by oil majors are in focus this week, along with the outlook for European power demand and sales on Gazprom’s ESP platform. In Asia, we take a look at South Korean refiners’ crude preferences and the prospects for commodity demand in China.

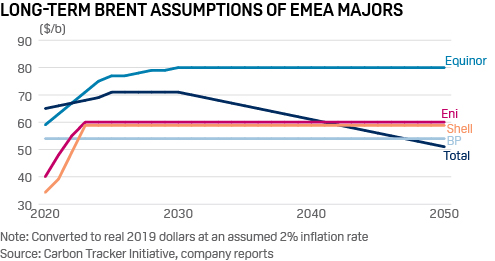

1. Oil majors rethink future price decks over pandemic squeeze

What’s happening? Europe’s biggest oil companies have been cutting their future oil and gas price assumptions over the expected long-term impact of the coronavirus pandemic on the global economy. BP got the ball rolling last month by announcing it would write off up to $17.5 billion worth of assets after cutting its long-term price assumptions for oil and gas to reflect expectations that the coronavirus pandemic will accelerate the shift away from fossil fuels. Two weeks later, Shell also slashed its near-term oil and gas price assumptions to reflect a more bearish, post-pandemic market outlook, and Eni last week became the third European oil major to revisit its price outlook.

Go deeper: Oil demand seen recovering to above 100 million b/d

What’s next? Although annual price deck revisions are a standard accounting revision for oil majors, the latest moves have sparked concern over a wider industry recognition of the potential for more stranded assets as the energy transition hits the long-term value of oil and gas. The material downgrades to asset values also cast a shadow over IOC finances at a time their balance sheets are being stretched by collapsing cash flows and rising debt levels to meet capex and dividend commitments. Markets watchers expect both Equinor and Total to make similar changes to their price outlooks as they are both running higher long-term commodity price assumptions than their European oil major peers.

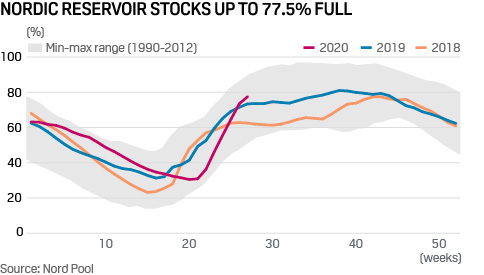

2. European power demand recovery outpaced by supply-side improvements

What’s happening? Demand across Europe's five largest electricity markets in the second quarter of 2020 fell 12% year on year as coronavirus lockdowns restricted activity. At 367 TWh, Q2 electricity demand across Germany, France, Italy, Spain and Great Britain was 52 TWh lower year on year, preliminary system operator data show. German Q2 power demand was seen 9% lower on year at 101 TWh, while the other markets registered double-digit declines.

What’s next? While lockdown measures are easing, a west European recession is expected to keep power demand significantly below last year’s levels into Q3. Platts Analytics expects demand losses of 4%-8% versus pre-COVID-19 levels in Q3 in western mainland Europe, and 10% in Great Britain. A year-on-year drop in French nuclear supply would go some way to offsetting the downside price impacts of lower demand, but French generator EDF has just issued an improved outlook, taking the edge off baseload supply concerns. With Nordic hydro reservoir stocks pushing up towards 100 TWh two months ahead of multi-year schedule norms, Northwest Europe could be awash with cheap supply this summer.

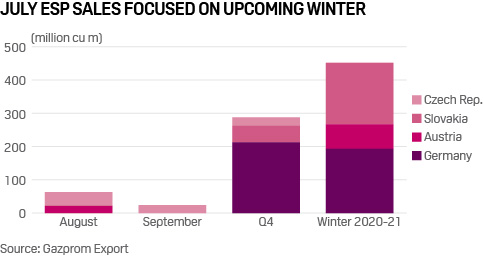

3. July ESP sales reflect appetite for winter volumes

What’s happening? Russian gas sales on Gazprom Export's Electronic Sales Platform (ESP) have slowed so far in July, while the volumes sold have been predominantly for delivery in the upcoming winter. No gas is being offered on the platform for shorter-term delivery given the very low European gas prices, so the ESP has now become a tool for traders to buy Russian gas for delivery much further down the curve, even out to calendar year 2022.

What’s next? The ESP has been used successfully by Gazprom Export to sell additional gas into Europe outside of its traditional long-term contract model. But with the European gas market still faced with oversupply, stocks nearing capacity and prices still low, traders are likely to be looking to the ESP to secure volumes for much later delivery, with little appetite for short-term buying. Changes in selling and buying behavior on the platform in the coming weeks will depend largely on the evolution of prices.

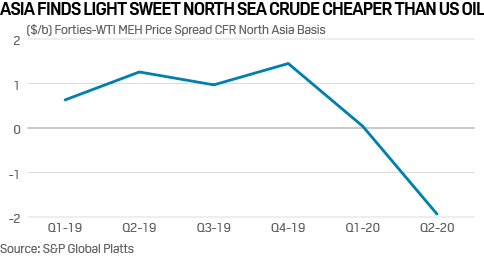

4. S Korea shifts focus to North Sea from US for light sweet crude imports

What's happening? The spread between Forties crude on a CFR North Asia basis and WTI Magellan East Houston on an Asia delivered basis averaged minus $1.94/b in the second quarter, Platts data shows. The spread flipped to a discount after commanding an average premium of 4 cents/b in Q1 and $1.45/b in Q4 2019. In addition, the Brent/Dubai Exchange of Futures for Swaps – a key indicator of Brent's strength or weakness against the Middle Eastern benchmark – averaged minus $1.09/b in Q2, falling from 41 cents/b in Q1 and $2.93b in Q4 2019. A weaker EFS makes crude grades produced in the North Sea that are priced against Brent more attractive than Dubai-linked Persian Gulf grades as well as US crudes. Many Asian refiners purchase US cargoes on Platts Dubai pricing basis.

What’s next? South Korean refiners look set to increase North Sea crude purchases at the expense of light sweet US crude imports as the narrow Brent-Dubai price spread lowers the procurement cost of Forties crude, while the North American benchmark WTI remains relatively expensive. South Korea's combined crude imports from the UK and Norway are estimated at around 5 million barrels in the second quarter and the shipments could reach at least 6 million barrels in Q3, up sharply from 750,000 barrels in Q1 and 730,000 barrels in Q4 2019, according to trading desk managers at major South Korean refiners surveyed by Platts.

5. China’s demand for commodities could be poised to disappoint

What’s happening? Total Chinese social financing, a broad measure of credit and liquidity in the economy, rose 12.8% in June, the highest monthly growth rate since December 2017. The Chinese authorities have been boosting lending and lowering borrowing costs in an attempt to offset the economic impact of the coronavirus pandemic. Previous injections of liquidity in 2012 and 2016 fed straight through to infrastructure and more importantly the housing sector, boosting demand for everything from industrial metals to diesel.

Go deeper: China's infrastructure push and global steel demand

What’s next? In China cheap money boosts commodity demand. What’s not to like? But this time it might be different. Alongside the usual slew of major projects, the government is prioritizing among other things the construction of “new infrastructure” – data centers, 5G networks and clean energy vehicle charging infrastructure. While supporting the development of the emerging digital and clean energy economy is probably a good thing, they aren’t as commodity-intensive as good old-fashioned housing. In the first five months of 2020 floor space started and floor space sold were both down 13% year on year. And when it comes to infrastructure it’s getting harder to find decent projects to invest in. In the absence of solid support from infrastructure and housing, commodity demand may disappoint this time.

Reporting by Robert Perkins, Andreas Franke, Henry Edwardes-Evans, Stuart Elliott, Mark Tan, Philip Vahn, Avantika Ramesh and Sebastian Lewis.