11 May 2020 | 20:29 UTC — Insight Blog

As lockdown alters food and fuel demand, is it ‘mayday’ for European sugar prices?

At the start of 2020 European sugar producers could have been forgiven for thinking the worst was behind them.

After falling to historic lows in 2018, European sugar prices were on an upward trend, fueled by tough growing conditions, continued contractions in planted area and consolidation in the industry.

There was a bullish sentiment in the air as the market departed the Dubai Sugar Conference in February: it had been confirmed that European planted area would fall again, stocks were tight and the NY No.11 May contract was trading at 15 c/lb. The world sugar market fell into a structural deficit following three successive years of surplus.

However, as the coronavirus spread to Europe and lockdowns were enforced across the continent, the outlook turned bleak for European sugar producers. Almost two years to the day since delivered white sugar in Western Europe fell to an all-time low of Eur312/mt, on May 1, Platts assessed the price at Eur449/mt in Western Europe and at Eur500/mt in the Mediterranean region.

But these assessments have fallen Eur13/mt and Eur18/mt respectively since the beginning of April. With coronavirus weighing on demand, a potential larger European crop on the horizon and imports continuing to flow in, fundamentals look bearish for the sweet foodstuff.

Consumption slides as Europe locks down

Sugar consumption has always been difficult to track, but in Western Europe, consumption of has been relatively flat, leading to a focus on the supply side of the sugar equation. However, the spread of coronavirus through the continent has turned this traditional assumption on its head.

As consumers rushed to supermarkets to stockpile, sugar demand was given an initial boost by retail sales. Such sales traditionally only make up 10-15% of European consumption, but there was a surge as consumers looked to fill their cupboards.

However, as the European lockdown became the “new normal” and the stockpiling relented, it became clear that European sugar consumption was going to fall. The hospitality sector has been decimated, with bars, restaurants and hotels forced to close, and sport and social events postponed.

The evidence has been seen along the value chain, with food producers having to limit the opening of their factories as well as more traditional spot buyers, such as bakeries, having to close their doors completely.

Well-known food and drink producers have started to report the impact of countrywide lock-downs on sales, confirming the trend.

Hugh Johnston, CFO of PepsiCo, said the company's operating margin was sure to be “negatively impacted by the weakness in immediate consumption channels”. He referenced not just the closure of bars and restaurants, but also the fact that consumers were not purchasing soft drinks at local shops or petrol stations. Rivals Coca-Cola said its global sales volume had declined 25% year on year for the first few weeks of April.

The European ethanol kicker

Aside from altered shopping and eating habits, sugar has also been hit through another demand outlet: fuel ethanol.

Fuel demand and prices have plummeted under coronavirus pressure as numerous countries banned or discouraged all but essential journeys. Platts’ T2 Ethanol benchmark assessment fell 46% from 647.5 eur/cu m on February 20, to an all-time low of 350.75 eur/cu m on March 24. Although the benchmark staged a recovery throughout April, it was assessed at 506 eur/cu m on Thursday May 7, at a significant discount to its trading level pre the European lock-down.

The opportunity for European producers to turn their feedstock into fuel ethanol instead of sugar was attractive before the global pandemic, but given the current value of fuel ethanol compared to sugar, it is no longer economic. Furthermore, if fuel ethanol demand is impacted in the longer term as the lockdown continues, less sugar could be diverted to its production in the new campaign.

Go deeper: Podcast - Global veg oils markets wrestle with COVID-19 disruptions

Import parity price trades lower

After trading above 15 c/lb for the first time in over 2 years, the NY No.11 raw sugar price recently traded below 10 c/lb. With the collapse in the international oil markets, Brazilian ethanol is now paying less than sugar on the spot and forward curves, and this has swung the sugar mix (the amount of sugar cane diverted to the production of sugar instead of ethanol) back to 45%, according to the latest S&P Global Platts Analytics estimates.

This is a move of over 10 percentage points from last season, which saw the sugar mix at all-time lows of 34.3%, and resulted in record ethanol production. Each percentage point equates roughly to 800,000 mt of extra sugar.

Combined with a weak Brazilian real that encourages sugar production and exports, at a time when global consumption is being revised down, the global supply deficit has been dramatically cut. Platts Analytics now forecasts a global 2019/20 deficit of 3.98 million mt raw value, having had a deficit of 8.33 million mtrv as recently as February, showing the huge shift.

As the balance sheet in Europe has become tighter over the last two campaigns, the need for exports weakened and domestic prices began to rise gradually. The pattern is shown by Platts’ assessed FAS Antwerp export premium rising from $10 over the front month ICE White Sugar contract in early 2019, to $45 as of Thursday May 7.

But this premium of European domestic prices to the world market, from tighter production, attracted imports and the 2017/2018 trade surplus turned into back-to-back years of trade deficits.

Crucially, it is this potential wave of imports that could put further pressure on European domestic prices.

There are several different types of import access to the European market:

- ACP/LDC Agreements – no duty and no maximum tonnage per country

- Tariff Rate Quotas (TRQs) – no duty with allocated tonnage per country

- CXL countries – Eur98/mt for raw sugar with allocated tonnage per country

- Full duty paid access – Eur339/mt for raw sugar

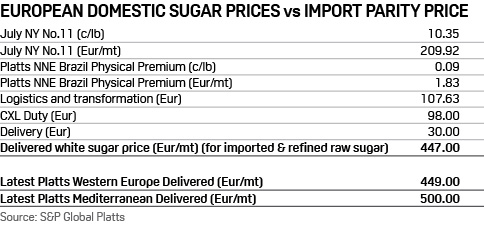

As shown in the import parity price model below, with the world market at 10.35 c/lb, raw sugar cargoes from CXL origins, with the Eur98/mt import duty paid, can theoretically be refined and delivered to customers for Eur447/mt, some Eur53/mt lower than the latest Platts Mediterranean delivered assessment.

While preferential origins that have duty-free access into the European market are always looking to export to Europe, the current premium of European prices to the world market will only attract them to maximise their quantities.

However, the key lies in the CXL producers. The latest data release from the European Commission shows that Brazil has not yet been allocated any of the 334,054 mt of raw sugar it can export to Europe with the Eur98/mt CXL duty.

In total, only 173,193 mt out of 790,925 mt of raw sugar under the CXL quota has been allocated so far, highlighting the volume of sugar that could theoretically be shipped into Europe from these CXL origins.

By locking in the futures contract, and the current NNE Brazil physical premium (assessed by Platts Thursday May 7 at 0.09 c/lb), refiners can fix the delivery of raw sugar for refining on a longer horizon, and with NNE Brazil having raw sugar ready for export as of September, cargoes could arrive just before the European beet harvest commences.

Europe’s sugar production set to rise

The sugar beet planting season has finished and small increases in acreage in the Netherlands and the UK could not outweigh lower acreage in the main producing countries of France and Germany. Platts Analytics forecasts European sugar beet area to fall by 1.6% on the year to 1.611 million ha, meaning European planted area will have fallen 7.2% since the peak in the 2017-18 season.

However, Europe is forecast to see no decline in sugar output. Platts Analytics forecast production in 2020-21 at 17.635 million mt white value (mtwv), slightly up from 17.540 million mtwv in 2019-20, on the back of closer to normal weather conditions and improving sugar beet yields.

In its April bulletin, the European Commission’s crop monitoring unit, MARS, forecast beet yields for the 2020-21 season at 75.9 mt/ha, 1.5% above the past five-year average, in line with Platts Analytics. The research unit noted that Western Europe had witnessed one of the driest spring periods since 1979, and that there was potential downside to yields if these dry conditions continued, but precipitation returned over the European beet belt later in the same week, to ease such concerns.

A European summer far from tradition, where there will be limited holidays and social events, is likely to continue to weigh on European sugar consumption. With the NY No.11 raw sugar contract trading just above 10 c/lb, imports can be locked in and this import parity should continue to put bearish pressure on the European market.

As European production looks to rise on the year, all these factors make bleak reading for European producers who were hoping low price environments were a thing of the past.