24 Jun 2021 | 20:13 UTC

US oil, gas rig count jumps 10 to 577, amid more signs of oil demand recovery

Highlights

Oil rigs, horizontal oil rigs up 16 each to 448/335

Bakken Shale gains four rigs, for total of 23

Upstream optimism may be greater than forecast

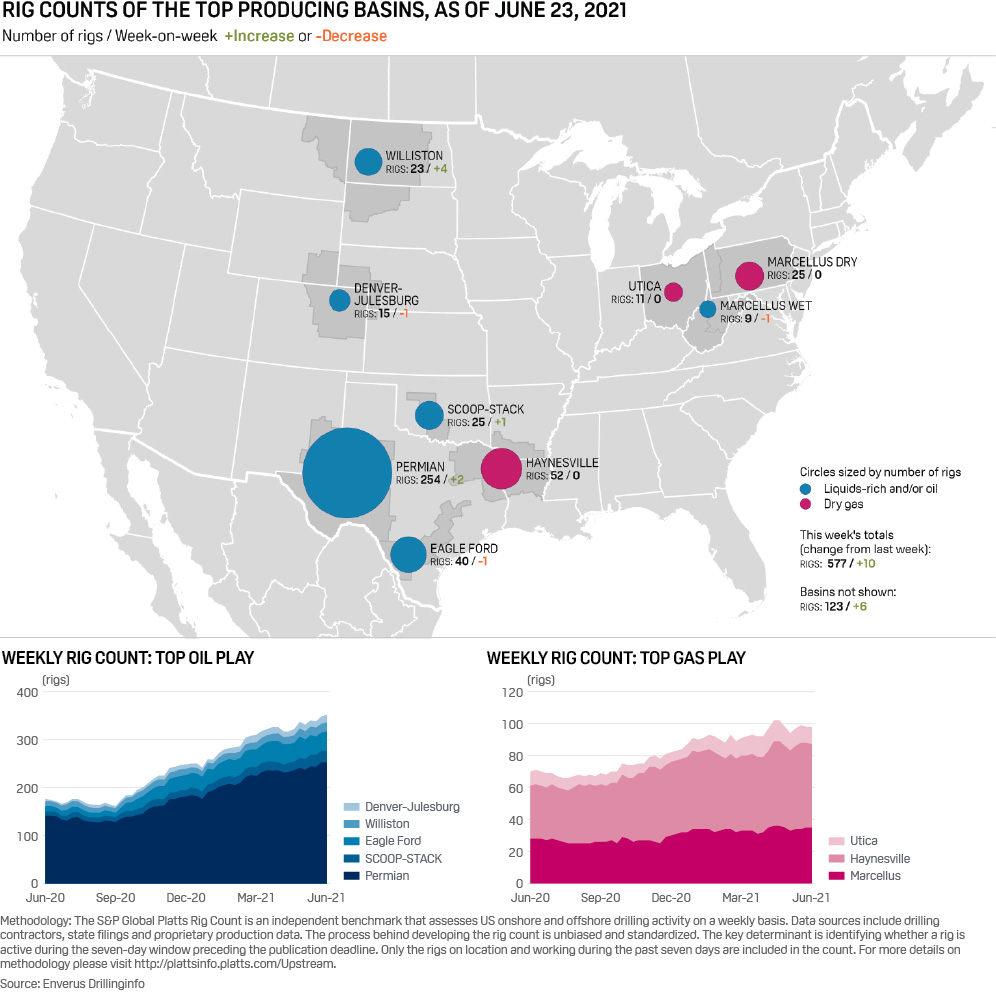

The US oil and gas rig count jumped 10 to 577 in the week ending June 23, Enverus data showed, amid continued lofty oil prices, still-rising oil demand and fresh signs of recovery following the roughly 18-month pandemic.

The Bakken was the star of the week, gaining four rigs for a total of 23, while the Permian Basin was up two rigs to 254.

Losing a rig each for the week ended June 23 were the Eagle Ford, the Marcellus and DJ Basin, leaving respective totals of 40, 34 and 15 rigs.

The SCOOP-STACK play in Oklahoma gained a rig, for a total 25, while the Haynesville and the Utica were unchanged at 52 and 11 rigs, respectively.

Oil rigs rose 16 for a total 448, as did the horizontal oil rig count, which also rose 16 to 335. Natural gas rigs and horizontal gas rigs were each down six, to 129 and 115, respectively.

Horizontal rigs, a rough measure of shale activity, are up 22% year to date in Q2 2021, or 77 rigs on average, compared to Q1.

Higher horizontal activity seen

"Moving forward, we still expect to see horizontal activity continue to grind higher in the coming months," investment bank Tudor Pickering Holt said in a June 21 investor note.

Despite the slight weekly rig movements in larger basins, signs are shaping up for 2022 to be a stronger year than many have predicted.

"With oil prices firmly in the $70s per barrel range, oil market tightness expected to continue as economies reopen, and OPEC likely to gradually return barrels to the market, we now expect North American E&P spending to rise about 20% in 2022," compared to its previous estimate of a roughly 10% increase, Evercore ISI analyst James West said in a June 23 investor note.

For the week ended June 23, WTI averaged $72.54/b, up $1.27, according to S&P Global Platts; while WTI Midland averaged $72.41/b, up 86 cents; and Bakken Composite averaged $70.33/b, up $1.22.

At Henry Hub, gas prices averaged $3.21/MMBtu, unchanged on week, while at Dominion South the average was $2.37/MMBtu, up 31 cents.

West said E&P companies entered 2021 estimating WTI around $45/b and have mostly kept to initial spending plans.

However, "we anticipate budgets will be based on $55/b-$60/b WTI next year," he said. "While E&Ps and majors are highly likely to maintain capital discipline, the industry will have a lot more capital at its disposal. When budgets reset early in 2022, large operators will increase their drilling and completion activity."

Evercore is "now doubling down on North American growth and market tightness," West said.

At the same time, the industry is also quickly running out of spare hydraulic fracturing or frack capacity, he said.

The frack count now hovers around 230. While West noted the "massive retirement cycle" for frack equipment in 2020, he said industry is likely down to around 250 available spreads.

Optimism

Some of industry's strains of optimism could be heard in recent June analyst conferences, where presenters agreed upstream producers are demonstrating a continued resolve to live within their means and build value rather than production growth, unprecedented in recent decades.

"A more constructive backdrop [was showcased] at this year's conference," Scott Hanold, upstream analyst for RBC Capital Markets, said in a June 10 investor note about the investment bank's annual Global Energy, Power & Infrastructure conference.

"[Upstream] business models were pruned of costs, growth appetites ... shed and a focus on free cash flow generation emerged," Hanold said.

In addition, a key topic of discussion at the RBC virtual gathering and also two other conferences separately sponsored by Wells Fargo and J.P. Morgan, was how E&P companies regard production growth given continued oil price strength.

Overall, "we see US E&Ps still yielding a higher post-dividend free cash flow and enterprise value today on consensus estimates than we did at the end of Q3 2020," Wells Fargo analyst Nitin Kumar said.

Kumar said Wells Fargo also continues a positive stance on natural gas.

"Although acknowledging weather/seasonal risks to demand over the summer, we see US gas supply fundamentally constrained and set to decline until 2023 while demand should remain relatively resilient," he added.