22 Oct 2020 | 15:28 UTC — London

Feature: EU carbon market to move into fourth gear from 2021

By Frank Watson

Highlights

EU ETS to reflect strengthened 2030 targets

Tighter market may address industrial emissions

EU regulators eye potential market expansion

Europe's flagship Emissions Trading System is about to shift into a higher gear when a fourth trading phase starts in January.

The 16-year old carbon market has begun to play a more significant role in decarbonizing Europe's economy in recent years, helping prompt a shift from emissions-intensive coal to natural gas and renewable sources for electricity generation.

But the system has failed, in its current form, to cut carbon emissions in the industrial sectors at anything approaching the same degree. That may start to change during the next 10-year trading phase, as the market's rules begin to tighten the supply of allowances available to those sectors.

Click here to see full-size infographic

"Industrial sectors like steel, cement and refining have typically received more allowances for free than their actual compliance needs," said Jeff Berman, director of emissions and clean energy at S&P Global Platts Analytics.

"However, free allocations are declining in Phase 4 and these sectors have historically had a difficult time in cutting their emissions. This means that these entities could soon be in a position where they will need to regularly buy allowances for compliance," he said.

The EU ETS is a major engine of the energy transition in Europe, and the carbon price signal it generates will be critically important for investments in clean energy and industrial processes. Those investments will help determine the EU's success in reaching its longer-term target to reach net-zero emissions by 2050.

"Higher reduction targets means lower EU ETS supply, which all else equal can lead to higher carbon prices," said Berman.

"We will also need a sense of how the Commission might revise mechanisms like the Market Stability Reserve in order to account for stronger climate ambition," he said.

"We are also looking for what types of incentives and policies the EU and member states will put in place outside of the EU ETS to encourage the energy transition, as that can deeply impact EUA prices," said Berman.

"For example, national governments offered considerable assistance through feed-in tariffs and government auctions to encourage wind and solar development in the last 10-15 years, meaning that the EU ETS had to do less of the heavy lifting. We could see a similar situation as the EU moves to encourage hydrogen development," he said.

Tighter caps

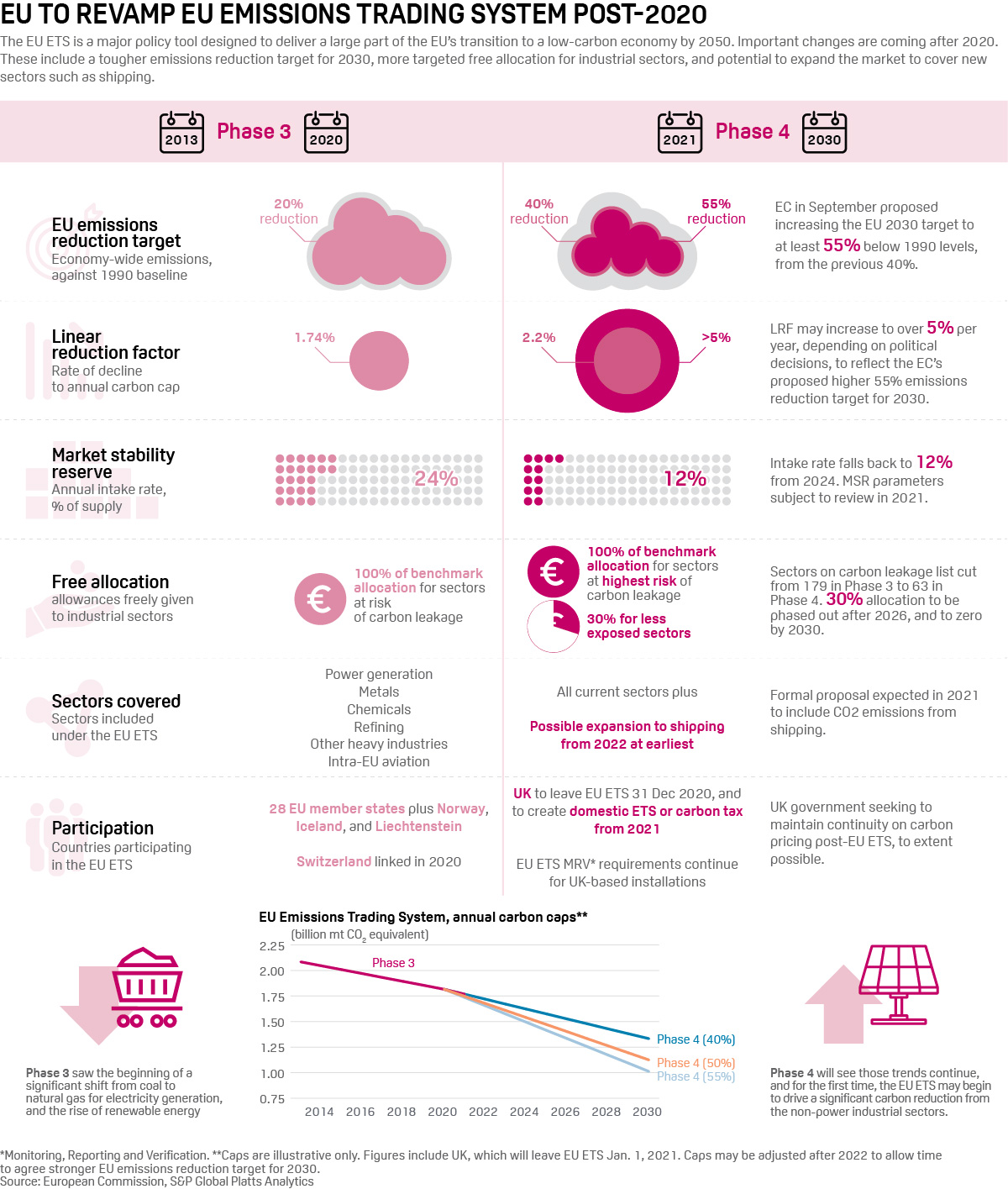

Most of the regulatory changes coming in Phase 4 were agreed years ago under a revision to the EU ETS Directive, but critical changes are coming that are yet to be nailed down – perhaps most importantly the rate of decline in the annual caps on carbon emissions that will drive the pace of emissions reductions out to 2030.

The European Commission in September unveiled its proposal to increase the EU's 2030 emissions reduction target to at least 55% below 1990 levels, from the previous 40%. This would translate into a sharper annual reduction in the carbon caps – the so-called Linear Reduction Factor.

The LRF was 1.74% per year from 2013-2020, and is already set to increase to 2.2% per year from 2021-2030 under the 40% emissions goal. Under a revamped 55% target, this figure will need to increase further, and may be as high as 5% per year, depending on when the steeper rate will apply.

Some analysts have said they expect a lower rate of just over 3% per year, but starting sooner than 2025, to avoid a sharp increase later in the decade.

Other important changes include rules on free allocation of carbon allowances, and a review of the Market Stability Reserve – a mechanism to keep surplus allowances out of the market, effectively tightening supply available to Europe's industrial companies.

More targeted free allocation

Under the EU ETS, carbon allowances are provided to industry according to a balance of 57% auctioning and 43% free allocation.

Free allocation of carbon allowances will continue after 2020, but will only be available to a much more targeted set of industrial sectors.

Free allocation will be available to sectors on the so-called carbon leakage list – a group of sectors and sub-sectors deemed at highest risk of relocating to avoid EU carbon costs. The list has been cut down from about 180 sectors in the period 2015-2020 to about 60 sectors from 2021-2030.

Companies in sectors on the list will continue to receive 100% free allocation according to their specific industry product benchmark, while those not on the list will receive 30% of the benchmark value, declining after 2025 to reach zero in 2030.

The sector benchmarks are based on the performance of the 10% most efficient installations in each sector, meaning only the most efficient plants will have their carbon needs fully met through free allocation.

More flexible rules have also been set to better align the level of free allocation with actual production levels. This is expected to mean allocations to individual installations may be adjusted annually to reflect increases or decreases in production.

This more targeted approach to free allocation suggests more industrial sectors will have to pay for their CO2 emissions after 2020, creating a greater incentive to switch to lower-carbon processes or close down or reduce running times at older, less efficient plants.

MSR review

The Market Stability Reserve – a major change in the functioning of the EU ETS – was brought into operation in January 2019 and works by removing 24% of the supply of carbon allowances in circulation each year.

The MSR's intake rate will continue at 24% until after 2023 when the rate will fall back to 12% per year, under current legislation.

However, the MSR is up for review in 2021 and its parameters may be adjusted if the mechanism is seen to be falling short of delivering its objective to return the EU ETS to a functioning balance between supply and demand.

For example, EU lawmakers could decide to extend the 24% annual withdrawal rate after 2023, cutting more quickly the supply of allowances available to market participants and limiting the downside for carbon prices in Europe, or potentially driving them to fresh highs.

Expanded coverage

EU regulators are looking to expand the EU ETS as they look for ways to deliver on the bloc's goals to decarbonize the economy by mid-century.

The system currently covers just over 40% of Europe's economy-wide CO2 emissions, and includes power generation, intra-EU flights, and heavy industries ranging from refining to production of metals, chemicals, cement, ceramics, bricks, glass and a host of other manufacturing activities.

The European Parliament in September voted to expand the system to include CO2 emissions from shipping, and the European Commission is expected to unveil a formal legislative proposal for this in June 2021.

Industrial emissions

The EU ETS has successfully started a process where natural gas and renewables have squeezed emissions-intensive coal out of the power mix in Europe, aided by low gas prices as well as unilateral political decisions by some EU member states to phase out coal-fired power plants.

The coming decade will be a test of whether the system can begin to replicate this success in the non-power emissions-intensive sectors, where emissions reductions have been more elusive to date.

The combination of tighter carbon caps to 2030, a smaller functioning surplus of overall allowances and more targeted free allocation for industry may allow the system to start to move the needle on CO2 emissions from the non-power industrial sectors in the fourth trading phase.

Switzerland links, UK leaves

The EU carbon market's fourth trading phase starting January 2021 will also see the UK leave the EU ETS as a result of its departure from the EU.

The UK has said it wants to maintain carbon pricing continuity for UK-based businesses and has said it is aiming to put in place a domestic UK ETS, or a carbon tax if a market is delayed. Recent speculation has suggested the UK may be leaning toward a carbon tax, although the official government position has been for both options to remain on the table.

The UK already has the expertise in place to run a domestic carbon market, having done so in the years up to the EU ETS starting in 2005, and will maintain the EU ETS CO2 emissions monitoring, reporting and verification requirements in the UK after 2020 to facilitate a domestic market.

"What is clear is that the UK government remains committed to carbon pricing in some form," said Berman at Platts Analytics.

The UK will be the first country to leave the 31-member trading system, while non-EU country Switzerland linked its domestic carbon market to the EU ETS in January 2020.

Overall, the regulatory changes coming after 2020 point to carbon prices holding their recent values, and potentially breaking higher into fresh territory, as the overall supply tightens and EU regulators look to the carbon market to deliver emissions reductions in new sectors on the long road to net-zero in 2050.