12 Aug 2021 | 20:05 UTC

US oil, gas rig count jumps 14 to 617 on week as companies sound upbeat note

Highlights

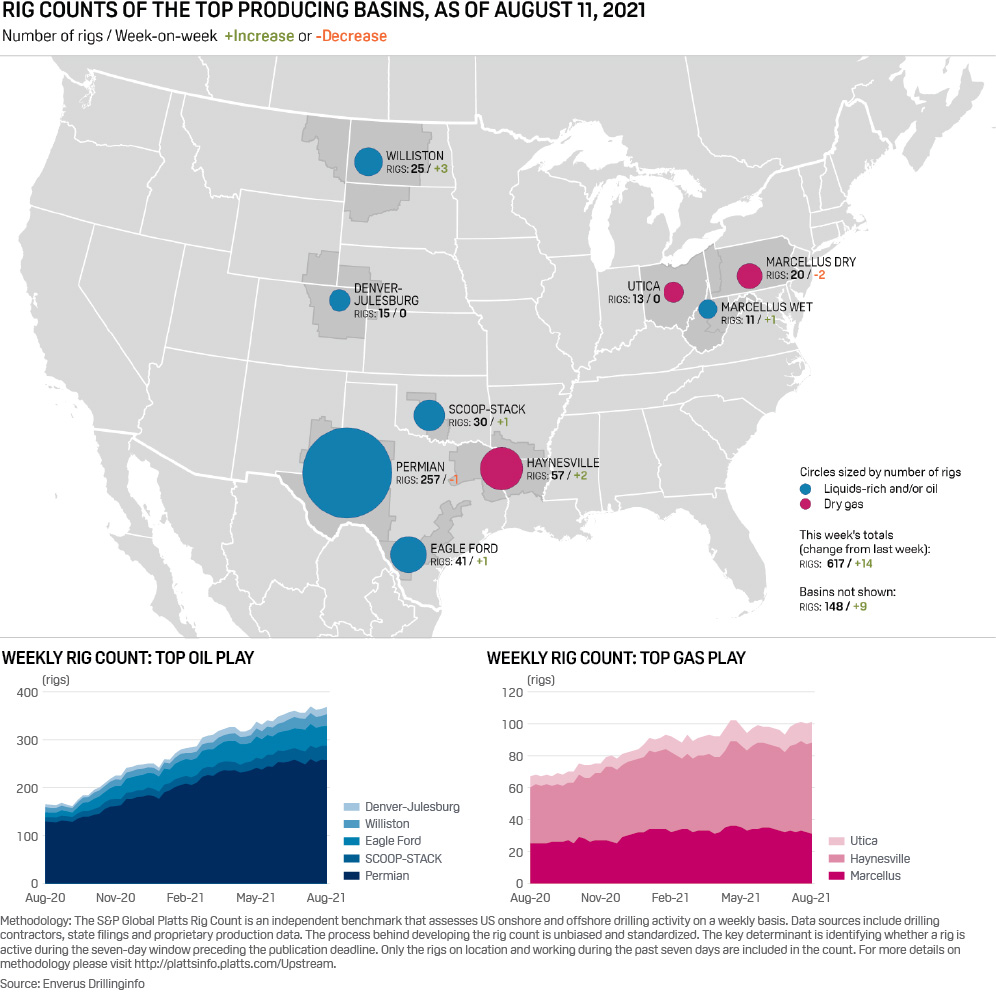

Bakken sees biggest weekly change, up 3 to 25

Permian Basin down by 1 rig, leaving 257

2022 operator thought suggests caution on oil markets

The US oil and gas rig count jumped 14 to 617 on the week, energy analytics and software company Enverus said Aug. 12, the highest activity level since early April 2020 as upstream companies concluded second-quarter earnings calls on an upbeat note.

Oil rigs landed at 474, up 11, while natural gas-directed rigs were at 143, up three for the week ended Aug. 11. Horizontal rigs leaped forward by eight to 469 – also the highest that rig classification has been since mid-April 2020.

"Looking ahead, we continue to expect relatively modest incremental horizontal activity improvement over the balance of Q3 2021, followed by a stronger ramp-up over the course of Q4," boutique investment bank Tudor Pickering Holt said in its Aug. 9 daily investor note.

Geographically, the basin with the biggest weekly change was the Bakken Shale of North Dakota/Montana, which gained three rigs for a total 25. That is the highest activity level in that play, where the rig count has been fairly rangebound in recent weeks, since late April 2020.

The gas-prone Haynesville Shale of East Texas/Northwest Louisiana picked up two rigs in the past week, for a total 57 rigs. And gaining a single rig were the Eagle Ford Shale of South Texas and the SCOOP-STACK play in Oklahoma, making totals of 41 and 30, respectively.

In addition, the giant Permian Basin of West Texas/New Mexico lost one rig, as did the Marcellus Shale, mostly sited in Pennsylvania, leaving totals of 257 and 31, respectively.

DJ, Utica basins unchanged

The DJ Basin of mostly Colorado and the Utica Shale were unchanged, at 15 and 13 rigs, respectively.

E&P operators' quarterly earnings calls for Q2, most of which wrapped up over the past week, reflected a growing confidence in continued oil price strength and stability. Producers appeared not to be tempted by higher oil prices in recent months – even though those prices came down a bit in the last week.

For example, WTI NYMEX oil prices averaged $68.28/b, down $3.23, while WTI Midland averaged $68.39/b, down $3 and Bakken Composite prices averaged $67.56/b, down $2.93, according to S&P Global Platts.

But natural gas prices gained strength, averaging $4.14/MMBtu, up 15 cents, while at Dominion South they weighted in at $3.72/MMBtu, up 55 cents.

Overall, E&Ps spent around 25% of their full-year budgets in Q2, or around 47% in the first half of 2021, while completing roughly 30% higher planned onshore wells (about 51% in H1 2021), Credit Suisse analyst William Janela said in an Aug. 11 investor note.

"At current strip prices, we estimate E&Ps will spend just about 41% of cash flow this year," Janela said.

Early E&P company commentary on 2022 signals continued discipline, Janela said, and operators seem to be taking a conservative approach with several framing a "base-case" around a maintenance scenario at this point.

Oil markets artificially supported?

A number of operators suggested oil market fundamentals remain artificially supported, with demand uncertainty from coronavirus variants, he added.

"We continue to forecast total US crude volumes of around 11.5 million b/d in 2022, up 5% year on year, driven by the Permian (up 11% year on year), including a robust 20%-plus year-over-year growth from private E&Ps," said Janela.

Credit Suisse's 2022 forecast is 2% below the US Energy Information Administration's projected 11.8 million b/d target (which the agency lowered another roughly 80,000 b/d in its August Short-Term Energy Outlook) and 3% below the International Energy Agency's roughly 11.9 million b/d.

"We think [both agencies] are still underestimating the ability of public E&Ps to uphold capex discipline next year," said Janela.

In addition, hydraulic fracturing activity is also back after two consecutive flattish months, TPH said.

"We now believe we're essentially at a [frac] spread count levels that will allow E&P operators to toe the line on crude oil production year on year in 2021 (i.e., maintenance levels)," the bank said. "Looking ahead, we now model around 230-240 average active spreads in 2022 versus about 220-230 previously."

Primary Vision, which tracks fracturing counts in the US, estimated 235 frac "spreads" or equipment/crew units, were active the week ended Aug. 6, down four from the previous week although the frac count has generally risen in the past month or so.

"While supply (around 350+ spreads) still remains well above demand (north of 210 spreads), we believe that net frac pricing should begin to get its back off the mat when we start to approach about 230-250 active spreads which likely comes to fruition in 2022 in our view."

Going forward over the year's second half, James Williams, president of energy consultancy WTRG Economics, expects growth in both rig activity as well as fracking.

"Two of the big constraints right now is getting employees back and getting truckers to drive materials for the industry," Williams said. "There's a heck of a need for truckers."