09 Sep 2021 | 20:13 UTC

US natural gas storage fields adds 52 Bcf, over market expectations

Highlights

Henry Hub futures continue rally

Winter strip pushes above $5/MMBtu

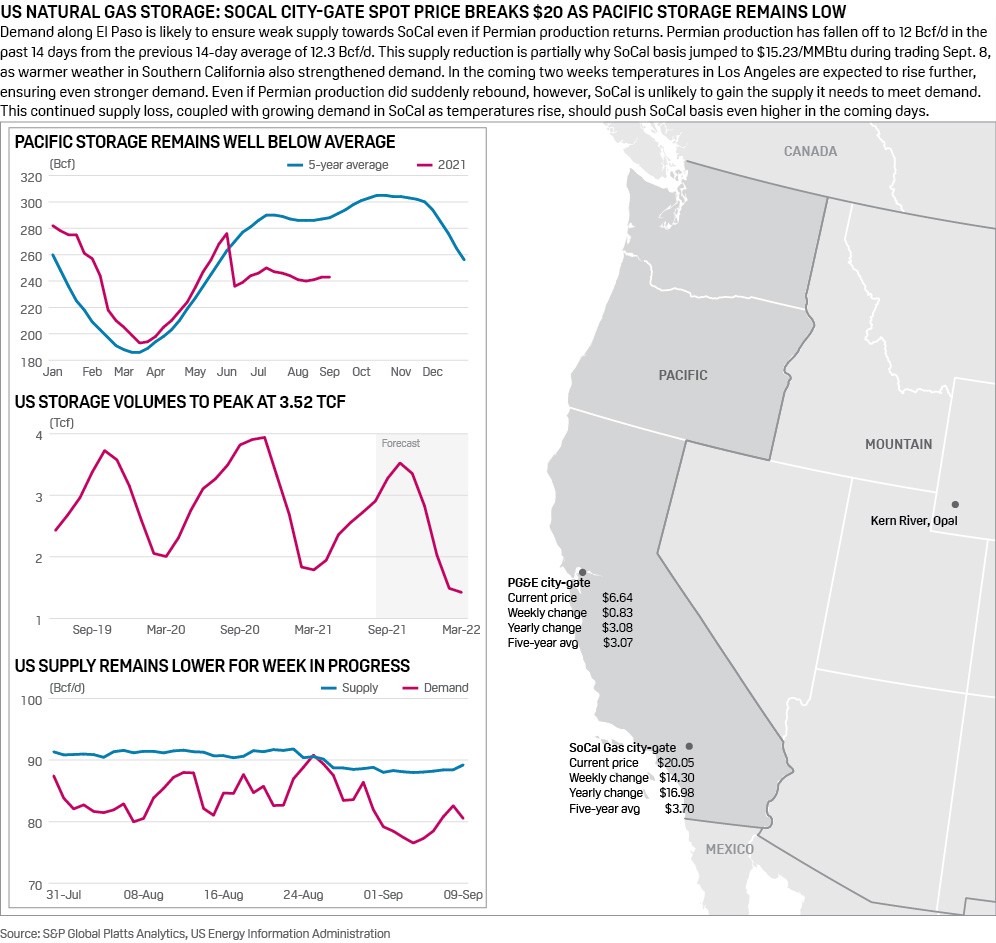

US natural gas storage fields added 52 Bcf of working gas for the week ended Sept. 3, according to an Energy Information Administration report released Sept. 9. The addition was much more than the market expected for the week, however, the report failed to quell the rally at Henry Hub as futures sustained highs not seen since 2008.

The addition was well above the 33 Bcf expected by an S&P Global Platts' survey of analysts and was completely outside the wide range of estimates that spanned from 24 to 48 Bcf. However, it still trailed the five-year average injection by 13 Bcf.

The working gas inventories stood at 2.923 Tcf following the addition, according to the EIA report.

US storage stands at 592 Bcf, or 17% less than previous year's level of 3.515 Tcf. It was also 7.4%, or 235 Bcf, less than the five-year average of 3.158 Tcf.

The injection was more than the 20 Bcf build reported in the previous week. Even as the inventory report painted a more bearish picture of US supply-demand balances week over week, bullish price momentum continued in the Sept. 9 trading session.

Henry Hub futures continued to build on prior gains following the release of the weekly storage report. The NYMEX Henry Hub October contract rose 8.5 cents to $5.00/MMBtu during trading Sept. 9. The prompt month contract in September has not averaged this high since 2008.

The winter strip -- November through March -- rose 7 cents to average $5.01/MMBtu, with only March trading below $5. This followed a massive rally Sept. 8 that saw winter gas prices rise by over 30 cents, propelling the benchmark to multiyear highs.

At the root of the increases is the decline in production, which stood at at 89 Bcf/d on Sept. 9 as offshore production levels remained below 800 MMcf/d, struggling to rebound following Hurricane Ida, according to S&P Global Platts Analytics. A heat wave throughout the Southwest is also pressuring an already tight market, pushing prices along El Paso South Mainline over $28/MMBtu.

While Ida led to a price spike in the near term, reliability concerns this winter are becoming more apparent, particularly in the Southeast and Texas as storage continues to be withdrawn from, widening the deficit to over 100 Bcf behind the five-year average and 300 Bcf below 2020.

Most regional hubs are at a premium to Henry Hub this winter, with prices in the mid-to-high-$5/MMBtu range. Prices can still climb higher as gas-to-coal switching reaches capacity. That would place fuel oil as the next possible switching channel. However, gas at above $12/MMBtu would be needed for that to happen.

Platts Analytics' supply and demand model currently forecasts a 55 Bcf build for the week ending Sept. 10. This would be 24 Bcf less than the five-year average with less than two months remaining in the injection season.