13 May 2021 | 20:38 UTC

US EIA reclassifies gas in South Central region resulting in 71 Bcf storage injection

Highlights

Survey called for 70 Bcf injection

Henry Hub summer strip tops $3/MMBtu

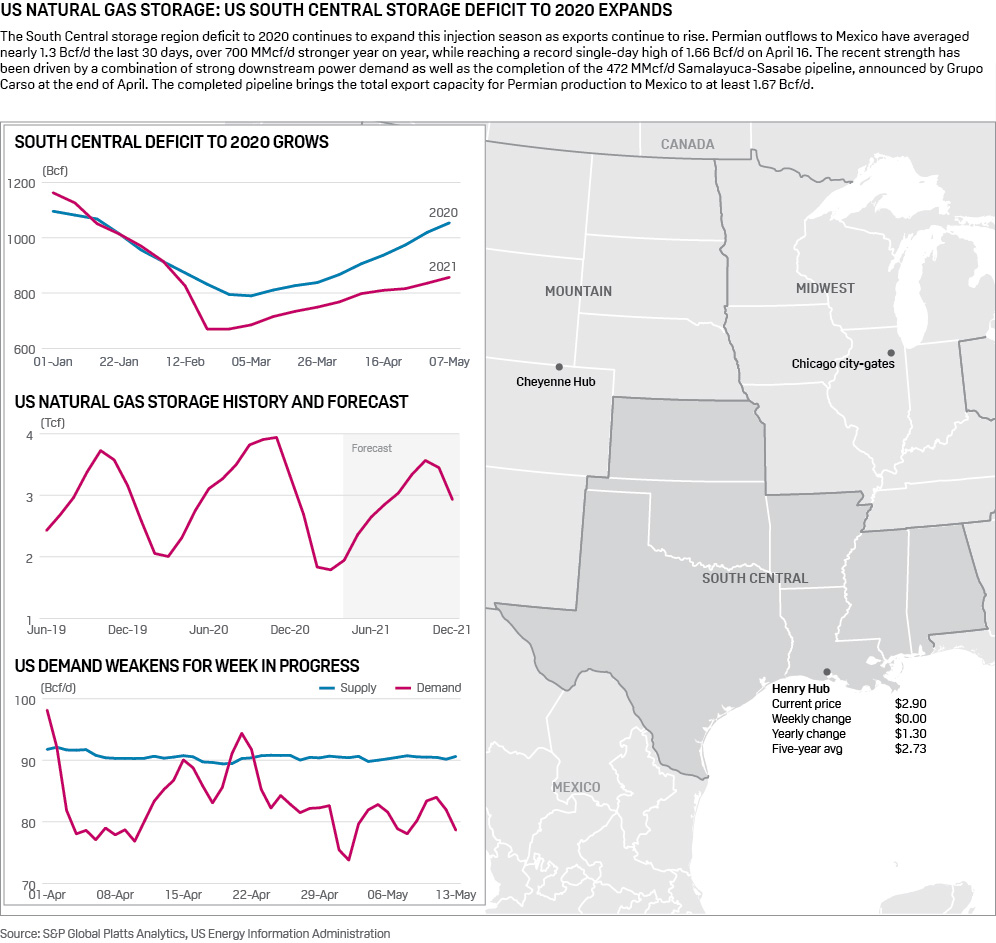

US natural gas storage volumes expanded by 71 Bcf, or 1 Bcf more than an S&P Global Platts' survey expected, as 4 Bcf of working gas stocks in the South Central region were reclassified to base gas.

Storage inventories increased to 2.029 Tcf for the week ended May 7, the US Energy Information Administration reported May 13. The build measured less than the five-year average of 82 Bcf and the 104 Bcf addition reported in 2020. Storage volumes now stand 378 Bcf, or 15.7%, less than the year-ago level of 2.407 Tcf and 72 Bcf, or 3.4%, less than the five-year average of 2.101 Tcf.

The South Central region is driving the largest portion of the mounting deficit, with stocks 197 Bcf lower year over year. This is due in part to substantial demand growth that has accrued in the area. Total demand for the week ended May 7 averaged 8 Bcf/d higher than a year earlier, according to S&P Global Platts Analytics. Much of the growth stems from higher feedgas deliveries to Gulf Coast LNG facilities and stronger exports to Mexico.

The NYMEX Henry Hub June contract was static at $2.97/MMBtu in trading on May 13. The balance-of-summer averaged $3.01/MMBtu, or 14 cents below the upcoming winter strip, November through March.

Platts Analytics' supply and demand model currently forecasts a 55 Bcf injection for the week ending May 14, which would measure 31 Bcf less than the five-year average.

Residential and commercial loads are up by roughly 3 Bcf/d week over week. The spike in home heating demand was softened somewhat by a 1.9 Bcf/d drop in power burn demand. Overall, total demand is up 1.3 Bcf/d week over week, averaging 87.1 Bcf/d.

Upstream, supplies have been notably flat, with the largest change coming from a 200 MMcf/d increase in net Canadian imports to meet rising res-comm demand, followed by a 100 MMcf/d increase in onshore production, bringing total supplies up by about 400 MMcf/d on the week to an average 95.1 Bcf/d.

Lower US gas yields have tightened supply just as Mexico and LNG exports have been rising resulting in tighter balances and increased gas-to-coal switching. With stocks heading into summer on the low side the outlook looks bullish especially if the weather turns hot. However, Platts Analytics believes the current forward curve is a little overdone and production will grow at these prices as wind and solar will increasingly offset gas-fired power demand.