11 Oct 2021 | 12:03 UTC — Insight Blog

Commodity Tracker: 4 charts to watch this week

Gas prices in Europe are experiencing wild swings, while analysts keep an eye on how prices could impact inflation. In China, ongoing power curbs means lower chances for another round of oil product export quota allocation.

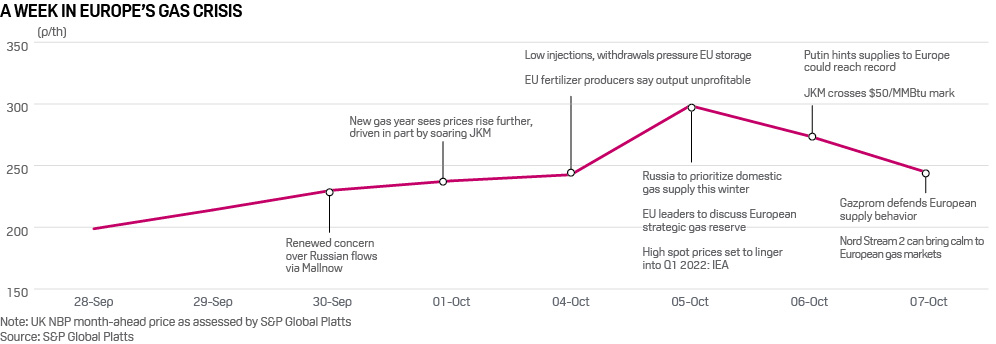

1. All eyes on Russian gas supply behavior

What's happening? European gas markets have experienced unprecedented volatility since the start of October, with prices hitting record highs on intensifying winter supply concerns, before easing late last week. The market reacted to the rapid news flow throughout Europe, with wild intra-day price swings. All eyes are on Russia, which some hold responsible for the overheating gas market, after President Vladimir Putin hinted that Russian exports to Europe could rise.

What's next? It remains to be seen whether Russian exports to Europe will increase in the coming weeks. Demand in the Russian domestic market remains high after a cold start to the winter, while Gazprom is still working to complete its storage injection program by November. Russian deliveries via Belarus having been erratic in recent months, while exports via Ukraine are still low. Any indication of additional flows via these two routes would be key, while an early startup of Nord Stream 2 would almost certainly see more gas come to Europe.

2. … and what price movements could mean to Europe's consumer price index

What's happening? The most recent assessment of Dutch TTF natural gas has breached Eur100Mwh, a record high at the equivalent of about $35/MMBtu. By comparison, Dated Brent at around $82/b is equivalent to only about $14MMBtu. Eurostat reports that inflation at a consumer price level reached 3.4% on year in September, with core inflation (ex-energy) rising to 1.9% on year. The European Central Bank has an inflation target of 2%, but it also focuses on financing conditions in setting interest rates and policy. The consumer price index for natural gas is estimated to have risen over 16% on year in September.

What's next? S&P Global Platts Analytics expects European natural gas prices to remain highly elevated over the winter heating season. Platts Analytics' monthly average peak for prices is still only slightly lower than the levels current being seen for spot gas and that expectation may have to be revised higher still. The pass-through impact of natural gas prices into consumer prices will first impact energy, both gas and electricity. Double-digit increases are certain to continue over coming months. However, based on analysis of Europe, Japan and the UK, which are all facing the prospects of higher natural gas and electricity prices, the pass-through to overall inflation is muted and diluted. While overall inflation in Europe is like to remain elevated above the ECB target and the energy component is likely to remain a problem, it should not trigger a policy shift by the ECB unless wage pressures rise appreciably and other considerations come under adverse scrutiny.

More on this topic: Europe energy price crisis

3. China's energy crisis lowers possibility of oil product export quota allocations

What's happening? China is suffering from energy shortage in Q4, reducing the possibility of another batch of oil product export quota allocation for rest of the year. Beijing has allocated a total of 37 million mt of oil product export quotas for 2021. In 2020, the allocation volume was 59 million mt, with 45.75 million mt of actual exports.

What's next? Beijing intends to cut the country's oil product exports to cap emissions and crude imports, and sources indicated since early September that the government plans to eliminate the outflow by 2025. Only 5.87 million mt or 1.47 million mt/month of quotas are available for exporting gasoline, gasoil and jet fuel from September to December, compared with 31.13 million mt or 3.89 million mt/month from January to August. A Beijing-based trader said the country has sufficient crude stocks, but "increasing oil product exports can lead to bad social impact" at a time when China is implementing power rationing and particularly ahead of winter.

More on this topic: China's power crisis

4. Global tankers freight rates poised to rise in Q4

What's happening? The VLCC tanker market has been suffering from a period of negative earnings since the second half of 2020, with oil demand significantly affected by the lockdowns and economic impact of the coronavirus pandemic. With global demand approaching pre-COVID levels and the OPEC+ alliance continuing with the gradual 400,000 b/d monthly production increases, the tanker market is starting to see the light at the end of the tunnel.

What's next? Freight levels are expected to see an uptick in Q4, but high bunker prices could erode tanker owner earnings. Crude tanker tonnages are facing more pressure than clean tanker market due to slower demolition and higher vessel deliveries of the former. This means the crude tanker market will continue to face a tougher recovery path compared to the product tanker market. Long term, crude tanker fleet growth is expected to peak in 2024 before scrapping takes centerstage ahead of the IMO 2030 decarbonization goals.

Reporting and analysis by Stuart Elliot, Alan Struth, Vickey Du, Sameer C. Mohindru.