Refined Products, Jet Fuel

April 16, 2026

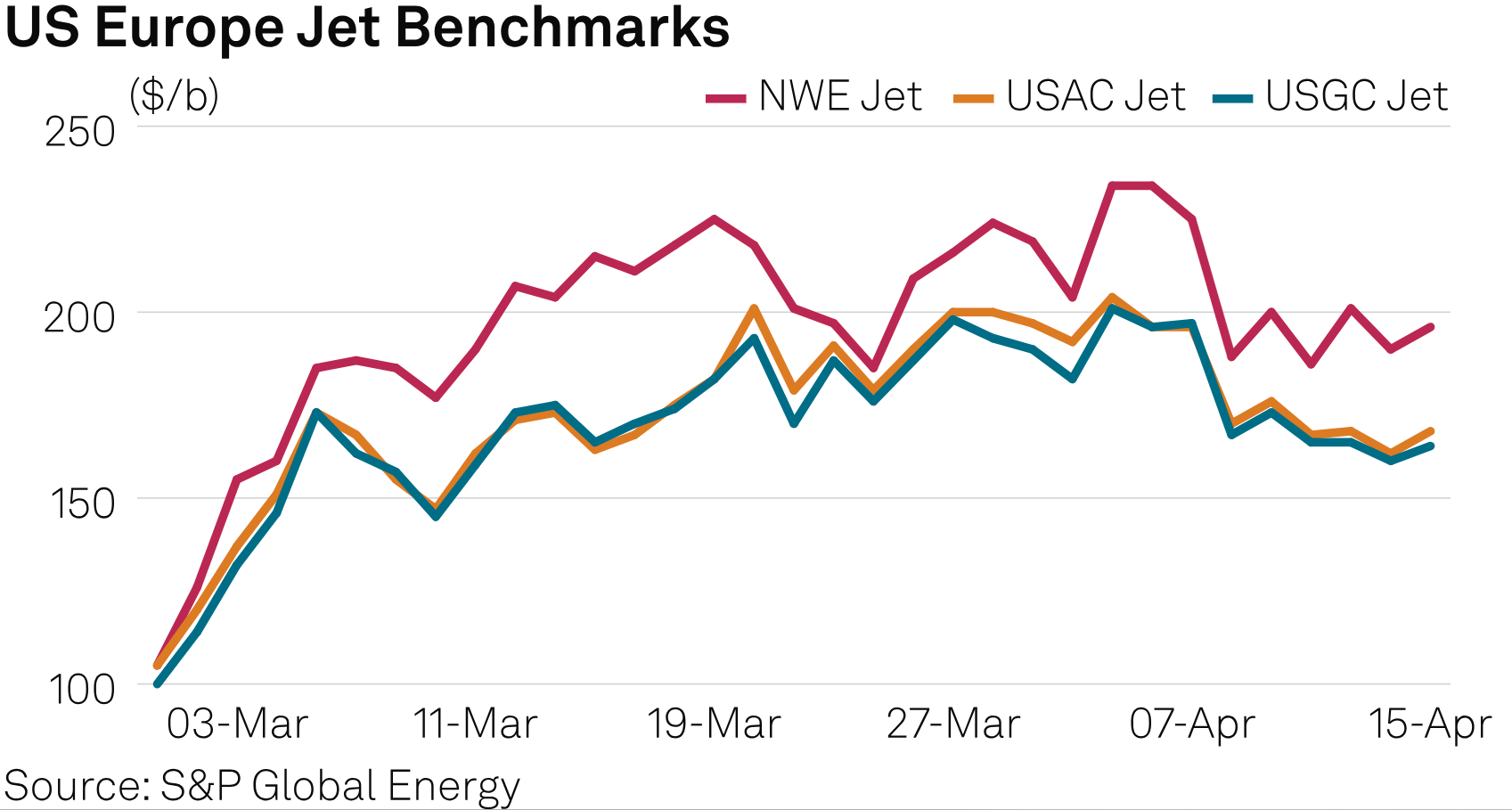

USAC-Europe jet arbitrage opens as NWE strength persists

Editor:

HIGHLIGHTS

First USAC to Europe jet cargoes since June 2020

US export premiums near record highs

US export loadings rise to all-time high

Europe is set to receive record volumes of jet fuel loaded on the US Atlantic Coast, according to S&P Global Commodities at Sea data.

Some 57,000 mt (about 450,000 barrels) loaded at New York Harbor in March is set to discharge in the UK in April, the data showed. This will be the first USAC-loaded jet arrival in Europe since June 2020, when 4,000 mt discharged at Skagen.

The arbitrage opened on the back of very strong European cargo pricing following the loss of Persian Gulf barrels in early April. The final Persian Gulf jet cargo aboard the STI Supreme before the near-closure of the Strait of Hormuz arrived April 6.

Jet cargo prices spiked to their highest level ever April 2, with the Platts-assessed CIF NWE cargo flat price reaching $1,842.50/mt. Prices have been volatile but remain 86% higher than before the outbreak of the war.

Open arbitrage between USAC and NWE is rare, as both regions are short jet fuel and typically import it. The USAC generally pulls volumes from the US Gulf Coast, a large jet producer, through the Colonial Pipeline, the country's largest products conduit, which moves about 2.5 million b/d from refinery centers in Texas and Louisiana to the East Coast, starting near Houston and ending near New York Harbor.

NWE usually pulls volumes from the East of Suez in Long Range tankers. In 2025, Persian Gulf volumes accounted for around 50% of jet fuel imports into Europe, CAS data showed.

US export demand rises

With Persian Gulf arrivals into Europe ending April 6, the US-to-NWE arbitrage has opened wider. In March, the average arbitrage incentive, the regional price spread minus freight, insurance and port fees, from the US Gulf Coast to NWE on MR tankers averaged $22.36/b, S&P Global Energy CERA data showed. In April, the arbitrage has averaged $17.73/b, narrowing on stronger freight and high USGC prices.

US export premiums for Jet-A and Jet A-1 cargoes were heard valued at premiums of 20-25 cents/gal to the USGC basis this week, at or near all-time-highs set on April 2.

USAC-to-NWE arbitrage has widened as US Atlantic Coast prices have flipped to rare discounts to the USGC seven times since the US-Israel war with Iran began. Before March, the USAC was last at a discount to the USGC in February 2023.

Platts assessed Colonial Pipeline Line Space, a secondary market for shipping rights, at minus 2.75 cents/gal for Line 2+3 Space on April 15. The discount generally indicates low distillate throughput on the pipeline, as international demand at the USGC outstrips domestic demand at the USAC.

"I think there is a good pricing incentive. There is a strong pull east from the US as expected given the loss of barrels from the Middle East," one source close to the European middle distillate market said. "The pricing is right at the moment but will depend on freight rates."

US jet exports spiked to 442,000 barrels/day in the week ended April 3, up by 62,000 b/d from the week prior and the highest in the Energy Information Administration's database from June 2010.