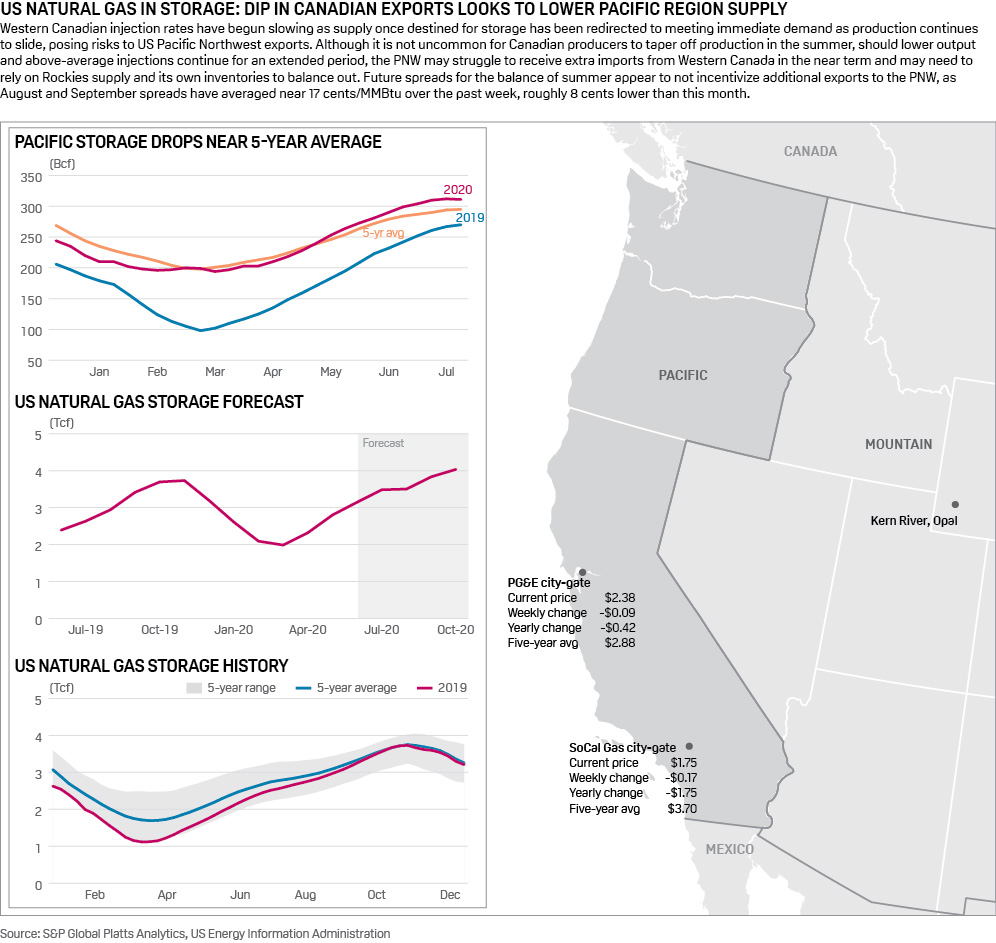

23 Jul 2020 | 15:44 UTC — Denver

US working natural gas volumes in underground storage rise 37 Bcf: EIA

Highlights

Build 4 Bcf above consensus analyst expectations

Henry Hub balance-of-summer nudges higher after decline earlier in week

Denver — US natural gas in storage inventories ticked up slightly more than expected last week, prompting slight gains to the NYMEX Henry Hub balance-of-summer prices, which remained nearly 10 cents lower than the week prior.

The amount of natural gas in US underground storage facilities increased 37 Bcf to 3.215 Tcf in the week that ended July 17, according to US Energy Information Administration data released July 23.

The injection was above consensus expectations of analysts S&P Global Platts surveyed, which called for a 33 Bcf build. The injection was 8 Bcf below the 45 Bcf build reported for the same week in 2020, but matched the five-year average injection, according to EIA data.

Storage volumes now stand 656 Bcf, or 25.6%, above the year-ago level of 2.559 Tcf and 436 Bcf, or 16%, above the five-year average of 2.779 Tcf.

The build was less than the 45 Bcf injection reported the week prior as total supplies averaged 91.4 Bcf/d, up only 100 MMcf/d from a week earlier, as nominal changes in production were boosted slightly higher by net Canadian imports, according to S&P Global Platts Analytics.

Downstream, total demand averaged 85.6 Bcf/d, with gains mostly centered on the power generation and residential-commercial markets, but widespread gains were limited across downstream sectors.

The NYMEX Henry Hub balance-of-summer contract — August through October — rose 2 cents to $1.76/MMBtu in trading following the release of the weekly storage report, although that was 8 cents below the week-ago close.

The gains have not extended into next winter, though, with the November-March contract strip holding flat at about $2.65/MMBtu as spreads between the two seasons are holding steady around 90 cents/MMBtu.

Platts Analytics' supply-and-demand model currently forecasts a 20 Bcf injection for the week ending July 24, which would be 13 Bcf below the five-year average.

The week in progress is seeing a 2 Bcf/d tightening of supply, and is again driven by gains in power burn demand, which outpaced a rise in onshore production. Total supply is averaging 91.7 Bcf/d, with most of the 300 MMcf/d net increase being driven by higher output in the US Northeast, which has added more than 500 MMcf/d of output from the week prior.

Downstream, total demand is up by 2.4 Bcf/d to an average 88.1 Bcf/d with most of the change occurring in the Northeast, where power burn demand is up by 1.3 Bcf/d on the week, followed by Texas, which has added 500 MMcf/d of power demand week on week.

Click here for full-size image

{kind=link}