16 Jul 2020 | 21:02 UTC — Denver

US working natural gas volumes in underground storage rise by 45 Bcf: EIA

By Brandon Evans and Eric Brooks

Highlights

US power burn demand hits year-to-date high

Smaller builds likely for weeks ahead

Denver — US natural gas stocks increased nearly 20 Bcf less than the five-year average due to year-to-date high gas-fired power demand, but the NYMEX Henry Hub balance-of-summer strip remained relatively static despite even smaller builds likely in the weeks ahead.

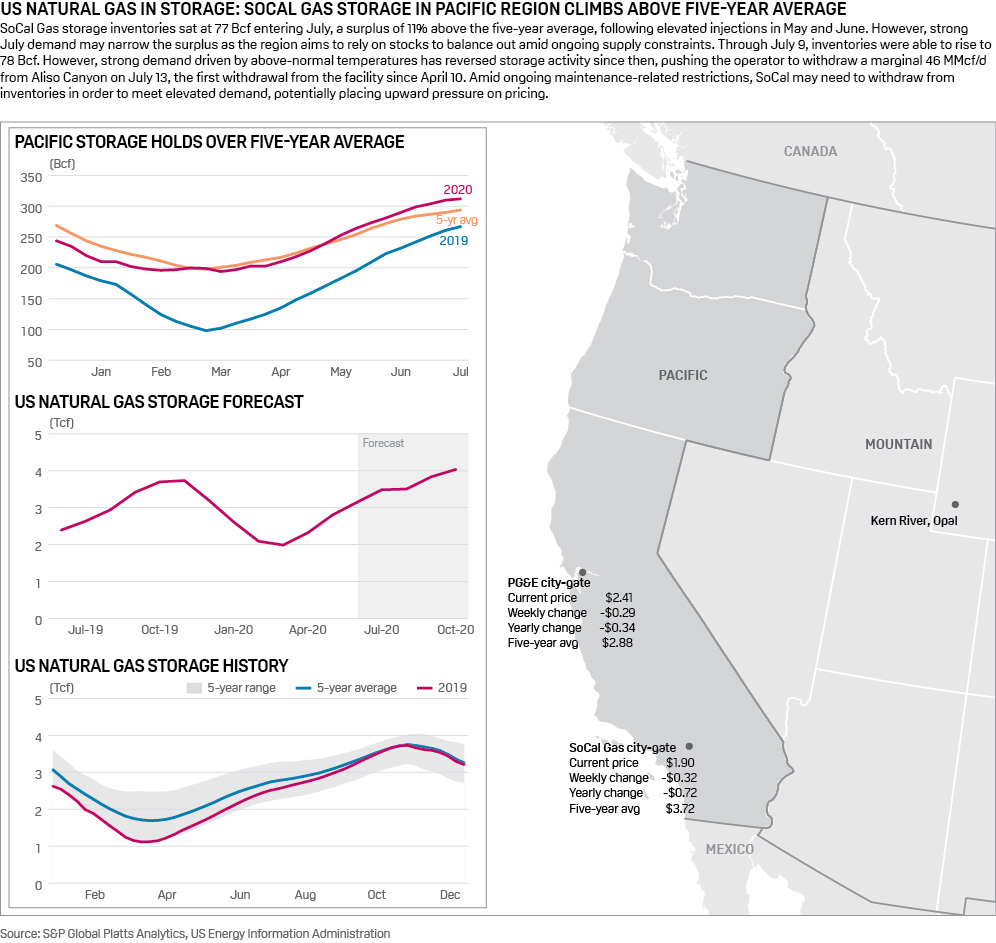

Storage inventories rose 45 Bcf to 3.178 Tcf for the week ended July 10, the US Energy Information Administration reported July 16.

The injection was below an S&P Global Platts' survey of analysts consensus that called for a 50 Bcf build. Wider responses to the survey ranged from injections of 42 Bcf to 65 Bcf. The build was also less than the 67 Bcf injection reported during the same week last year and the five-year average injection of 63 Bcf, according to EIA data.

It was the third consecutive weekly build that was below the five-year average.

Storage volumes now stand at 663 Bcf, or 26.4%, more than the year-ago level of 2.515 Tcf and 436 Bcf, or 16%, more than the five-year average of 2.742 Tcf.

Total demand rose by 1.4 Bcf/d during the week after 2.6 Bcf/d of power burn increases were reduced by a 1 Bcf/d drop in LNG feedgas demand and another 500 MMcf/d of declines from the residential and commercial sector, according to S&P Global Platts Analytics.

Upstream, supplies rose slightly on an increase in onshore production and an increase in net Canadian imports, pushing total supplies higher by 400 MMcf/d and leaving US supply-demand balances tighter by 1 Bcf/d week on week.

The NYMEX Henry Hub balance-of-summer contract, August through October, remained relatively static to average $1.846/MMBtu in trading following the release of the EIA's weekly storage report. Spreads to next winter have remained stable as well. The November-through-March contract strip is priced at $2.71/MMBtu, leaving spreads from balance of summer to next winter in the high 80 cents/MMBtu range.

Platts Analytics' supply-and-demand model currently expects a 36 Bcf injection for the week ending July 17, which would be 1 Bcf below the five-year average.

The week in progress has seen markets tighten by another 2 Bcf/d week on week, as supplies have held mostly steady while each downstream demand sector has posted small gains. Total demand this week is averaging 2 Bcf/d above the week ended July 10, led by a 700 MMcf/d increase in the power sector, where growth has slowed. There was also a combined 1 Bcf/d increase in residential-commercial and industrial demand relative to the week before. Upstream, total supplies have held firm, rising only 100 MMcf/d overall, led mainly by further small increases in net Canadian imports into the US.

Click here for full-size image

{kind=link}