20 May 2021 | 20:22 UTC — Houston

US oil, gas rigs fall 12 to 543 on week, as industry focuses on recovering oil demand

Highlights

Permian loses 4 rigs; Eagle Ford down 3

Most basins lost 1-2 rigs on week

Oil and gas rigs each decrease 6

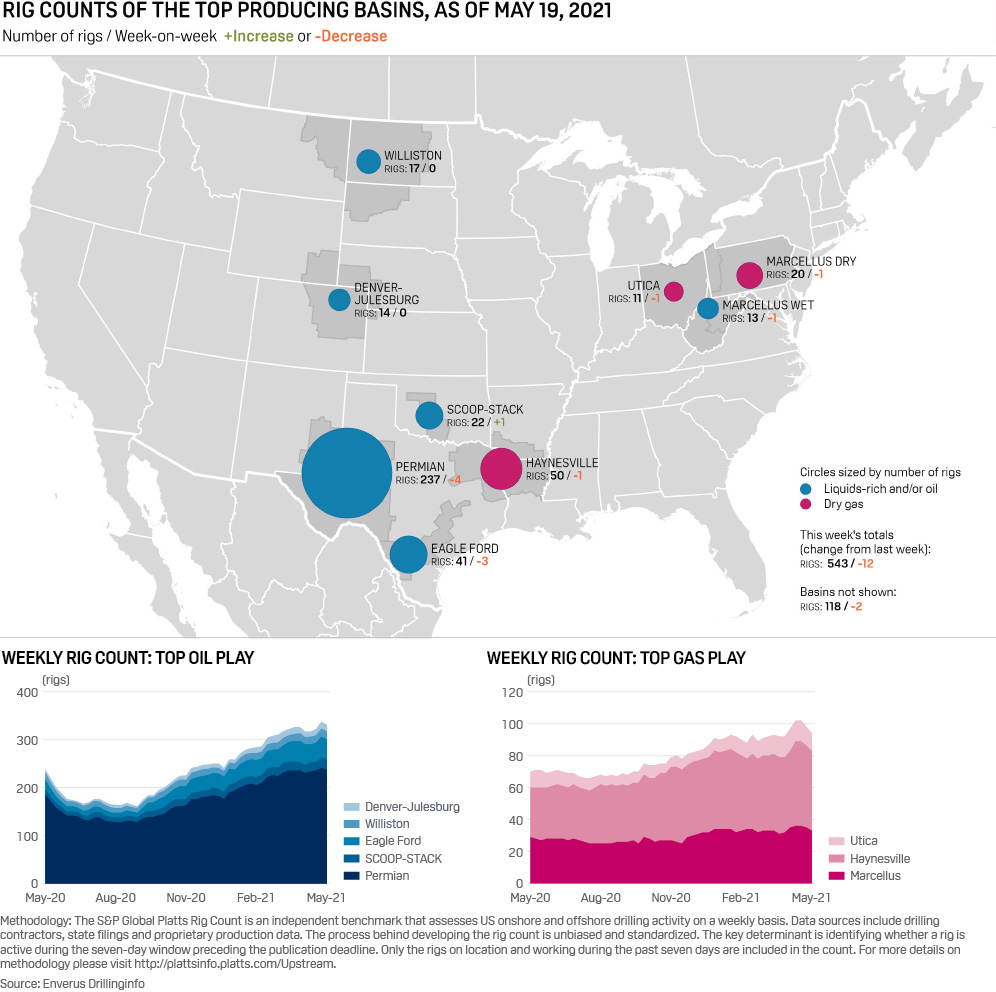

Houston — The US oil and gas rig count fell 12 to 543 on the week, rig data provider Enverus said May 20, despite oil prices that have persisted above $60/b and drilling activity that has generally headed up in 2021.

Analysts are painting a generally optimistic picture for the rest of the year as oil demand continues to recover from the coronavirus pandemic.

But for the week ended May 19, rig losses prevailed in most of the eight largest domestic basins, with the Permian Basin of West Texas/New Mexico down four to 237 and the Eagle Ford Shale of South Texas down three to 41.

The natural gas-prone Marcellus Shale, mostly in Pennsylvania, lost two rigs to 33, while the Haynesville Shale, a dry gas play in east Texas/northwest Louisiana, and the Utica Shale, largely sited in Ohio, each shed one rig for respective totals of 50 and 11.

The natural gas rig count lost six units in the past week for a total 120 – four in the Haynesville and two in the Marcellus. The total domestic fleet was also down six oil rigs to 423.

"We do expect rig activity to continue to rise – something we've stood by for about a year," S&P Global Platts Analytics analyst Taylor Cavey said.

"At $60/b, a lot of operators have gained confidence and feel much better about [the E&P landscape]," Cavey added. "That said, the theme of capital discipline remains unchanged, especially among the majors and public" upstream operators.

SCOOP-STACK gains rigs

The only major domestic basin to gain rigs this week was the SCOOP-STACK in Oklahoma, which pushed the play's total to 22 – the highest level of activity for that play since mid-April 2020.

Both the Bakken Shale of North Dakota/Montana and the DJ Basin mostly in Colorado were unchanged for the week at 17 and 14 rigs, respectively.

For the same week ended May 19, crude prices remained strong, although down a bit, while gas prices were largely static, according to S&P Global Platts estimates.

WTI averaged $64.86/b, down 32 cents, while WTI Midland averaged $65.17/b, down 20 cents and Bakken Composite, $62.84/b, down 81 cents.

Natural gas prices at Henry Hub averaged $2.90/MMBtu, up 1 cent, while at Dominion South, the average was $2.21/MMBtu, down 5 cents.

With Q1 results now in the hopper, the industry is now focused on the remainder of 2021 and a generally improving economy on the back of oil demand recovery.

"Importantly, the industry continues to message a greater attentiveness to the role US shale plays in the global macro" – notably, the fiscal conservatism of E&P operators and their intent to grow production only when the market needs more supply, RBC Capital Markets analyst Scott Hanold said in a May 14 investor note.

RBC's updated outlook reflects the investment bank's raised oil price forecast for 2021 of $64/b.

"We think this is supported by development plans that are unchanged and capital spending that is trending better than anticipated," Hanold added.

Goldman Sachs noted that producers on Q1 calls reiterated full-year production guidance that suggested relatively flat (around 1%) production growth collectively from Q4 2020 to Q4 2021.

Potential 'call on shale'

If strength in oil prices is sustained and incremental OPEC-plus barrels are absorbed through July, then the next few months provide insight on how best to address the "call on shale'" – if it comes, Evercore upstream analyst Stephen Richardson said in a May 17 investor note.

"The central thesis underpinning all of energy (and crude markets for that matter) remains US producer behavior and whether the lessons of past cycles (and a shift in incentives) are sufficient to make this cycle different than what came before," Richardson said.

Looking to the rest of the year, oil markets appear tight on supply, Evercore analyst James West said in a separate May 14 investor note.

Moreover, a number of positive data points suggest the "reopening trade is just getting started," West said.

Evercore's E&P analysis foresees that a stronger-than-anticipated demand rebound in second-half 2021 demand could leave the market "materially undersupplied" and requiring additional OPEC-plus supply adds above the 2 million b/d currently anticipated to be eased back onto the market from May to July.

"Travel is picking up quickly ... US consumers are excited to get back to pre-pandemic life," West said. "I encourage you to go for a stroll through Central Park over the weekend in order to truly appreciate how the Roaring 2020s will be unlike any other."