25 Mar 2021 | 18:58 UTC — Houston

US oil, rig count jumps 11 to 513, as Permian keeps adding: Enverus

Highlights

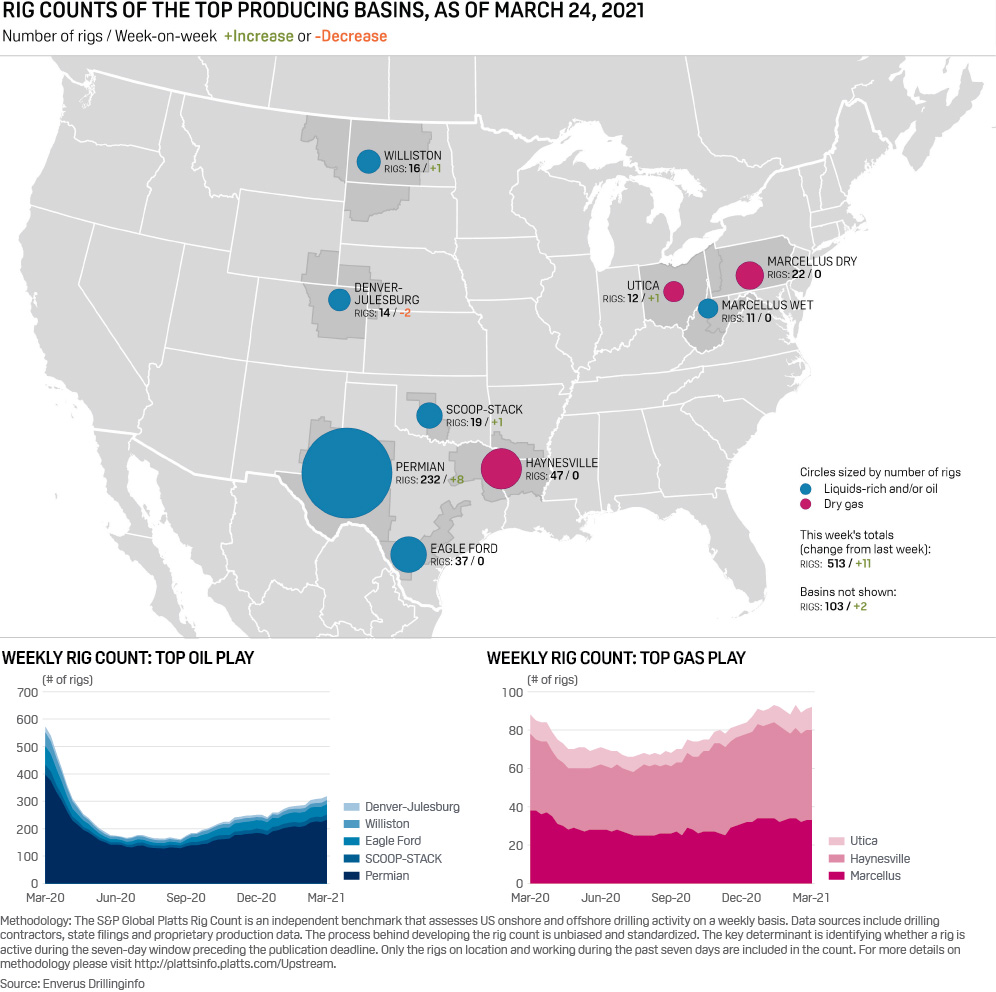

Permian Basin rigs up 8 to 232

Oil rigs add 12 for total 387

Rig counts highest since April 2020

Houston — The US oil and gas rig count jumped 11 to 513 in the week ending March 24, rig data provider Enverus said, as the prolific Permian Basin of West Texas and southeast New Mexico continued to add rigs amid lower but still robust crude prices.

Permian rigs were up eight to 232 on the week. So far this year, the basin has added 56 rigs.

Oil-directed rigs accounted for the week's jump, with counts up 12 to 387. Gas fields lost one rig, leaving 126.

The Permian and nationwide US oil and gas rig counts are the highest they've been since April 2020, when totals began falling fast as crude prices plummeted amid the pandemic's initial spread.

But that was a year ago, and since then WTI oil prices, which plummeted from just under $50/b in early March 2020 into the teens, have not only recovered but are now hovering around $60/b and well above breakeven levels of the $30s-$40s/b.

"The longer crude prices stay above $55-$60/b, the more confidence operators will have in bringing rigs back," said Parker Fawcett, North American supply analyst for S&P Global Platts Analytics. "But we think rig additions will continue to be slow and steady throughout the year."

The past week's rig additions were largely driven by privately held operators which have led the rig count recovery, Fawcett said.

"Privates are now only 34% below pre-pandemic levels, publicly traded companies near 50%, and majors still lagging at 79%," he added.

Most large US basins gained a rig or remained stable week on week, although the DJ Basin largely in Colorado lost two rigs, leaving 14.

Up a rig each were the Bakken Shale (16 rigs), mostly in North Dakota; the SCOOP-STACK (19), of Oklahoma; and Utica Shale (12), largely in Ohio.

Unchanged on week were the Haynesville Shale (47), of East Texas/Northwest Louisiana; the Eagle Ford Shale (37), of South Texas; and the Marcellus Shale (23), largely in Pennsylvania.

Flat spending

Producers have budgeted for 2021 generally at a $55/b Brent price, RBC Capital Markets Scott Hanold said. Industry generally agrees upstream operators will stay at current spending levels that compare roughly flat to last year, as oil price volatility remains during an uneven recovery period from the pandemic.

By contrast, E&Ps spent 34% less in 2020 as they quickly cut back on rig and activity levels in response to plummeting oil prices.

Hanold noted US E&P budgets for 2021 are flat year on year, while national oils, integrateds, Canadian and international spending "ticks up from trough levels," which averages out to a 10% increase overall.

"The market will scrutinize any activity increase from here, in our view," Hanold said in a March 24 investor note. "There could be capital creep if the macro shows fundamental sustainability, but that likely shows up more in 2022."

In addition, US midstream budgets on average are down 29%, while refiner budgets are "modestly" unchanged year on year, with capacity remaining overbuilt.

Oil production from companies Hanold tracks worldwide is likely up 7% in 2021, year entry to exit, implying year-end 2021 crude output near 99 million b/d globally.

"Growth largely comes from restored OPEC+ barrels and returning from sub-maintenance production levels," he said. "We peg US oil [up] 500,000 b/d (entry to exit) in 2021," he said.

$70/b Brent?

That said, thoughts of $70/b Brent are still out there, despite a roughly 10% lower price than earlier in the month.

Tudor Pickering Holt said its assessment of inventory draws is largely intact, and sees "robust" draws in 2021 on the current pace of demand recovery and OPEC+ supply cuts.

"What has changed is our assessment of the willingness for OPEC+ to enable price appreciation, considering the largely artificially tight market" it created through additional production cuts, TPH said in a March 23 investor note.

"We'd previously envisioned a more cautious approach to balances as prices rose toward our $60/b Brent outlook, with clear comfort from the OPEC camp, at least, if not the 'Plus' camp at $70/b," it said. "As such, we see room for Brent prices to return north of $70/b, should OPEC remain accommodative in that price band as inventories normalize and demand recovers."

According to S&P Global Platts oil and gas prices dipped during the week ended March 24.

WTI fell to $60.36/b, down $4.92 week on week, WTI Midland crude dropped to $60.61/b, down $5.34 and Bakken Composite fell to $60.54/b, down $5.02.

For natural gas at Henry Hub, prices averaged $2.47/MMBtu, down 8 cents on week, while at Dominion South prices averaged $1.87/MMBtu, down 20 cents.

(Corrects weekly oil rig change and total in bullets)