Metals & Mining, Ferrous, Non-Ferrous

April 01, 2026

TRADE REVIEW: Indian ferrous scrap market remains sluggish as Middle East war makes imports costlier

Editor:

HIGHLIGHTS

Turkey, Pakistan, Bangladesh outbid Indian buyers in Q1

Indian scrap import prices see best month since April 2025

This report is part of the S&P Global Energy's Metals Trade Review series, where we dig through datasets and digest some of the key trends in iron ore, metallurgical coal, copper, alumina, cobalt, lithium, nickel and steel and scrap. We also explore what the next few months could bring, from supply and demand shifts to new arbitrages and quality spread fluctuations.

The Indian ferrous scrap import market has seen prices of key grades improve steadily through the first quarter of 2026, after a feeble end to 2025, supported by risks associated with the war in the Middle East and some sporadic improvement in demand, market participants told Platts, part of S&P Global Energy.

However, market activity has remained largely sluggish for most of this period, as Indian buyers were held back by concerns over volatility in a rapidly weakening exchange rate, uncertainty over domestic downstream demand, and freight risks linked to the ongoing Middle East conflict since it began in late February.

The Indian rupee sank to an all-time low of Rupee 94.74/$1 on March 27, according to Platts data, which made imports more expensive for Indian buyers, and has recovered only marginally since then.

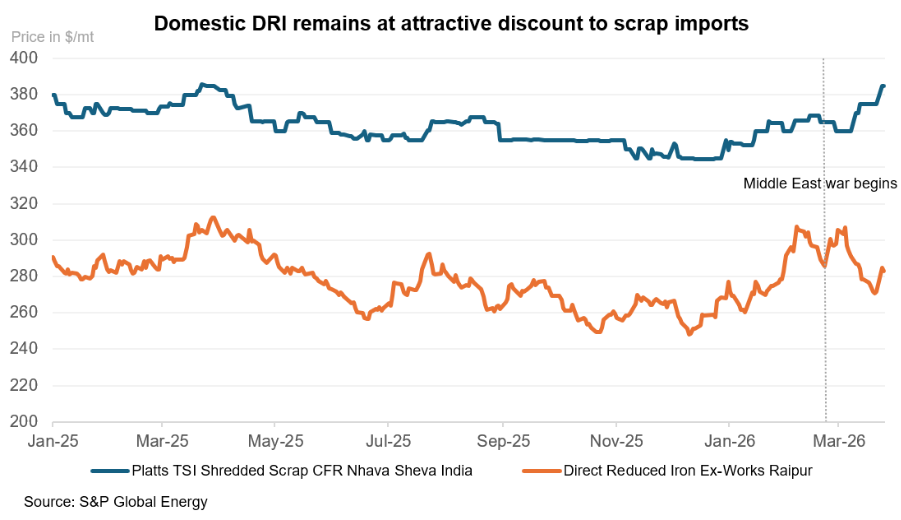

The adequate availability of domestic scrap and direct-reduced iron, a less expensive alternative feedstock, has also allowed mills to limit their reliance on imports. However, the use of Indian domestic DRI hit a ceiling earlier this year.

In December 2025, Indian imported containerized shredded scrap prices averaged $345.95/metric ton CFR Nhava Sheva. In January and February 2026, prices averaged $355.90/mt CFR Nhava Sheva and $365.08/mt CFR Nhava Sheva, respectively, supported by some positive demand sentiment.

In the wake of the war, prices rose to an average of $369.32/mt CFR Nhava Sheva in March, their best month since April 2025.

Tradable values and reported deal levels for imported containerized HMS 1/2 (80:20) rose from $320-$345/mt CFR Nhava Sheva in the first two months of 2026 before the war to $345-$370/mt CFR Nhava Sheva in March.

Domestic DRI prices have risen significantly in 2026. Prices rose from an average of Rupee 23,320/mt ex-works Raipur in December 2025 to Rupee 24,590/mt EXW Raipur in January this year.

In February, domestic DRI jumped to an average of Rupee 26,781/mt EXW Raipur, its best month since October 2024, and remained relatively unchanged at an average of Rupee 26,748/mt EXW Raipur in March.

Middle East war hits key Indian imports

Iran restricted the movement of freight through the Strait of Hormuz after the conflict began, reducing the supply of several goods to India, including several steelmaking raw materials and liquefied petroleum gas. As a result, the Indian government has moved to prioritize domestic and other essential uses of LPG over industrial production, amid continuous negotiations with Iran to allow Indian shipments of the fuel.

Market sources have told Platts that some producers may need to cut production due to reduced LPG availability for industrial use.

Historically, March is a relatively good month for demand, but this year that trend has been broken with Indian buyers choosing to be conservative due to the war, leading to very few import deals for ferrous scrap, a trader said.

Sellers look elsewhere

Indian buyers, hamstrung by a floundering exchange rate and slow downstream demand, cannot keep up with other import markets willing to pay higher rates, bringing imports to a near standstill, participants said. The more attractive import markets for sellers include Turkey, which is the world's largest importer of scrap, and India's neighbors, Pakistan and Bangladesh.

"Why even bother offering to India?" a second trader said.

Offers from various origins have been driven up by increased freight and fuel costs in the wake of the Middle East war, and a steady stream of demand from the above countries has helped meet those increased prices in March.

Pakistan and Bangladesh have had to turn to alternative sellers after losing access to some regular sources of scrap and other raw materials for steel in the Middle East due to the war.

In January and February, containerized shredded scrap was offered to Pakistan at prices ranging from $370/mt CFR Port Qasim and $395/mt CFR Port Qasim. Since the war, offers for containerized shredded scrap rose to $410-$420/mt CFR Port Qasim in March.

Participants said that with no exchange rate volatility to worry about, Pakistani buyers have been able to reliably price in the extra costs associated with the war and consistently pay higher prices than before for containerized shredded scrap imports. Deals for Pakistan were reported at $405-$420/mt CFR Port Qasim throughout March.

Bangladeshi importers held off on most scrap purchases for several months in the lead-up to the highly anticipated national elections in February, and following an encouraging outcome, returned to the market.

Deal values and tradable levels for containerized shredded scrap reported by participants rose from about $375-$382/mt CFR Chittagong before the war to $383.50-$405/mt CFR Chittagong in March, clustered above $395/mt CFR Chittagong.

Uncertainty could define the months ahead

Toward the end of March, there have been a very small number of concrete bids from buyers in the market, with insufficient demand to justify the cost and risk of importing in the current global environment, and significant improvement in the near-term is unlikely, participants said.

"The market is in a chaotic situation with way too many variables, and unless the rupee stabilizes, no one has any idea what is going to happen," a third trader said.

"Finished steel prices need to go up for imports to be viable," he said.

Platts assessed the IS1786 Fe500D/Fe550D 12-25 mm diameter rebar at Rupee 51,400/mt ex-works Raipur on April 1, unchanged from its highest level since June 2024 set on March 31.