Agriculture, Energy Transition, Maritime & Shipping, Biofuel, Renewables

December 17, 2025

COMMODITIES 2026: Singapore biobunker demand faces slow start as regulatory uncertainty, costs weigh

HIGHLIGHTS

Delay in IMO NZF clouds near-term outlook; EU, CII remain distinct drivers

High premiums and feedstock competition dampen voluntary uptake

Ethanol, methanol gain traction as progressively scalable alternatives for 2030s

This is part of the COMMODITIES 2026 series, where our reporters bring you key themes that will drive commodities markets in 2026.

Singapore, the world's largest biobunkering hub, is expected to start 2026 at a slower pace as elevated costs and regulatory uncertainty dampen shipowner demand, according to regional suppliers, buyers and market traders.

Shipping companies appear to be delaying biobunker procurement into early next year, adopting a wait-and-see approach as term contracts issued for 2026 supply decline year-over-year, a Singapore-based supplier said.

Regional regulations are expected to support demand recovery from Q2 2026, as Q1 will mark the start of compliance reassessment preparations following deferred procurement.

"Shipowners seem to prefer taking earlier action on biofuel rather than waiting until the last minute," a biobunker supplier said. "We can expect a surge in demand and rising prices in Q2, while Q1 acts as a preparatory period."

Singapore recorded steady growth in biobunker demand from 2024, with strong sales in the first half of 2025 before easing in recent months. Total biobunker sales from January to November reached just over 1.27 million mt, up 63.9% year over year, according to preliminary MPA Singapore data.

Feedstock competition drives cost

Singapore biobunker premiums against Platts benchmark FOB Singapore Marine Fuel 0.5%S cargo assessments for B24 LSFO grade, comprising 24% biodiesel blended with low-sulfur fuel oil, climbed through Q1 2025, exceeding $200/mt for the first time in mid-March.

"It is hard to say whether next year we will see a similar trend [in demand as this year], as there is a stark increase in price this year, compared to last year when fixing terms," a supplier said.

Platts, part of S&P Global Energy, assessed Singapore-delivered B24 and B30 low-sulfur biobunkers at $633.98/mt and $682.98/mt, respectively, on Dec. 16, reflecting premiums of $227/mt and $276/mt over Platts benchmark FOB Singapore marine fuel 0.5%S cargo assessment.

"With UCOME now facing competition with SAF, I don't think [term fixing levels] would go so low, unless suppliers have already locked in term contracts for UCOME," a trader said. Nevertheless, the trader noted the possibility of low offers distorting the market, as some suppliers aim to ramp up supply volumes for strategic reasons.

As limits on waste-based lipids loom, industry is increasingly looking toward alcohols. S&P Global Energy's Sustainable1 report identifies ethanol as "rising contender," noting that with favorable carbon intensity recognition, sugarcane ethanol could undercut B30 and bio-methanol prices by 2030-2035.

Also, major manufacturers, including MAN, WinGD, and Wartsila, have certified and conducted trials of dual-fuel and multi-fuel engines capable of operating on ethanol, methanol, and other fuels.

Clarence Woo, managing director of GCCF, noted the growth potential for maritime ethanol in the Asia-Pacific. "In APAC, the strongest growth signals are coming from B30 and alcohol fuels (Methanol-Ethanol). Singapore is already demonstrating scale, supplying over 1.2 million mt/year of marine biofuels. Thereby, a 20 million mt/year opportunity emerges progressively towards the early 2030s, in line with the delivery of more than 1,200 alcohol dual-fuel vessels to global fleets."

China UCOME pressured

The Chinese UCOME market was sluggish in the last quarter, as biodiesel buyers wound down year-end purchasing amid weak demand from Singapore, a Chinese producer said.

"Currently, tradable levels for UCOME are relatively low for producers, but raising offer levels would make it too high to attract buyers," the producer said.

Near-term upsides in China UCOME prices appear limited amid ample biodiesel output capacity and soft demand, a China-based trader said.

Market participants expect a quiet Q1 2026, with Lunar New Year holidays in February likely shutting biodiesel plants for nearly two weeks and delaying a pickup in inquiries until March.

Platts assessed UCOME FOB North China at $1,149/mt on Dec. 16, unchanged day over day.

Platts assessed UCOME FOB Straits at $1,259/mt on Dec. 16, unchanged day over day.

Biobunker demand mired by regulatory uncertainty

The International Maritime Organization's decision to delay the Net-Zero Framework vote has dented confidence among biobunker market participants, prompting shipowners to reassess near-term biofuel demand amid persistently high costs.

"Now with IMO NFZ delay, we foresee even less biofuels uptake for now. To brace for bad economics, there's a need to cautiously spend money," a bunker procurer from an Asian shipping company said.

NZF would have imposed sector-wide emissions limits and GHG pricing on ships with a gross tonnage above 5,000, covering roughly 85% of global shipping emissions, anchored to a fuel-intensity baseline of 93.3 gCO₂e/MJ and targeting reductions of up to 65% by 2040. The delay gives suppliers additional time to scale capacity and secure feedstocks, but weakens near-term economic signals for biofuel uptake.

Some shipping companies remain unfazed, citing vessel-level CII improvement requirements and internal sustainability targets as continuing demand drivers.

S&P Global Energy's Sustainable1 report highlights that while delays introduce uncertainty, they do not alter the sector's long-term decarbonization trajectory.

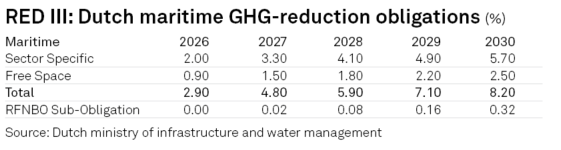

The delay refocuses attention on Europe, where the EU ETS and FuelEU Maritime remain in force, creating a bifurcated market. The pause also gives suppliers time to scale capacity and prepare alternative fuels for a $70–$80 billion marine fuel market, according to the report.