Agriculture, Maritime & Shipping, LNG, Biofuels, Wet Freight, Grains, Dry Freight

April 07, 2026

COMMODITY TRACKER: 4 charts to watch this week

By Staff

Editor:

Strait of Hormuz disruptions are tightening tanker availability and lifting clean freight rates, while LNG bunker pricing dynamics shift between Singapore and Rotterdam. India explores ethanol as a cooking fuel to secure supply and Asian corn prices hit 35-month highs as freight rates and fertilizer costs climb.

1. War in the Middle East drives clean tanker volatility higher

What's happening? The Platts Global Clean Tanker Index increased past $72,000/d in early March amid the war in the Middle East, then retraced to the high $50,000s before re-testing $70,000 resistance by month-end, compared to February's average of just under $40,000/d. Strait of Hormuz disruptions collapsed vessel traffic, tightening availability and lifting risk premiums. More than 50 LR2s migrated from clean to dirty employment to capitalize on record crude tanker returns, draining the clean tanker supply. Europe imported almost 3 million b/d of seaborne clean products in 2025, according to S&P Global Commodities at Sea data, with meaningful volumes from the Persian Gulf. The intra-Bollinger band gap widened to over $55,000/d in early March, up from below $13,000/d in February. Platts is part of S&P Global Energy.

What's next? Refinery closures in the Atlantic Basin, flagged by owners and industry groups as a 2026 theme, will mechanically increase product tonne-miles by shifting supply toward import dependence, particularly for Europe and the US West Coast markets. This structural lengthening collides with compliance-constrained fleets as sanctions reduce effective supply and concentrate market power among owners controlling compliant tonnage. However, higher cargo costs risk demand destruction through inflation and compressed refinery margins, potentially curtailing product exports and moderating freight eventually.

2. Singapore LNG bunker fuel commands premium over Rotterdam

What's happening? Platts assessed LNG bunker fuel in Rotterdam at $19.20/MMBtu on March 31, while Singapore was assessed at $20.749/MMBtu, establishing a $1.55/MMBtu premium to the Dutch port. This marks a sharp reversal from January through February, when Singapore averaged a $1.86/MMBtu discount to Rotterdam due to softer Asian demand and ample regional supply. The spread flipped to premium territory on March 3, reaching a high of $6.42/MMBtu as geopolitical tensions and QatarEnergy's March 2 force majeure on LNG supplies reshaped regional dynamics.

What's next? The premium structure is expected to persist as structural factors support Asian pricing. Platts JKM, the Northeast Asia LNG benchmark, surged to $25.412/MMBtu on March 19--the highest since Dec. 30, 2022--as Asia competed for US and West African cargoes amid absent Qatari volumes, according to Platts data. Market participants attribute the volatility to supply concerns, shifting arbitrage flows and stronger bunker demand in Asia relative to Europe, with the evolving spread continuing to influence vessel routing decisions and LNG bunkering economics across key global shipping corridors.

3. India explores ethanol for cooking fuel security

What's happening? Indian biofuel industry bodies, Indian Sugar and Bio-energy Manufacturers Association, Grain Ethanol Manufacturers Association and All India Distillers' Association, alongside petroleum leadership, are pushing to expand ethanol into domestic cooking to address energy security concerns. Nearly 60% of India's LPG demand relies on imports, with 90% of those imports transiting through the Strait of Hormuz, according to ISMA's white paper submitted to the Prime Minister's Office on March 19. GEMA reports grain-ethanol plants operate at 40-90% capacity utilization, with 20 billion liters of domestic capacity available and expected to reach 24 billion liters by 2026-27. Platts assessed Asian fuel ethanol at $685/cubic meter CIF Philippines April 6.

What's next? AIDA proposes a four-pronged roadmap, including 30% petrol blending, flex-fuel vehicles, ethanol cookstoves and diesel-ethanol blends, which was presented to the Ministry of Road Transport and Highways March 21. ISMA estimates 20% LPG substitution with ethanol could reduce annual imports by 6 million metric tons and save about $1 billion in combined direct subsidies and oil marketing company loss compensations. Industry bodies await formal government notification of ethanol as an approved clean cooking fuel and integration into the Pradhan Mantri Ujjwala Yojana ecosystem by 2026-27, with early stage testing of supply logistics underway.

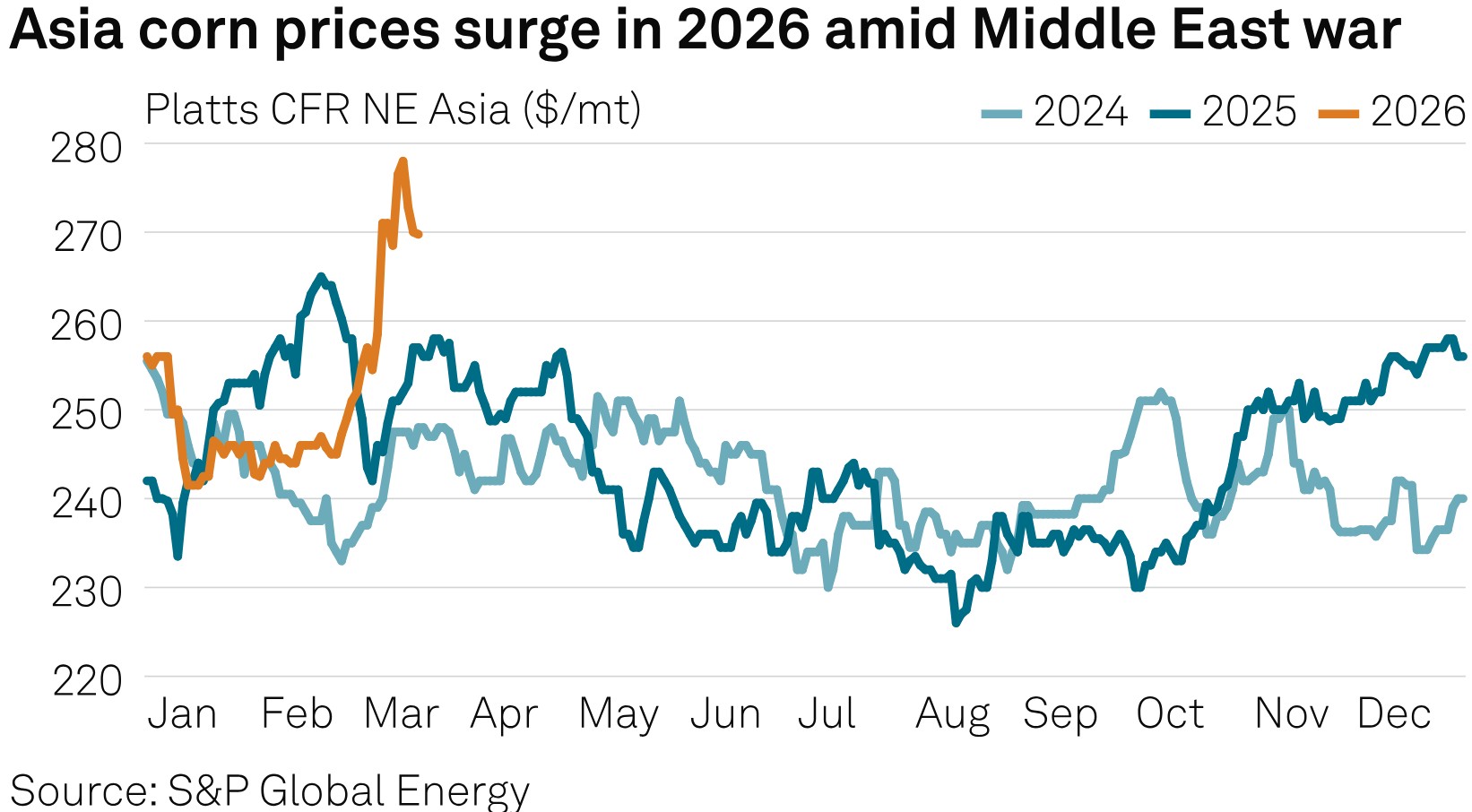

4. Middle East conflict drives Asian feed grain price volatility

What's happening? Platts assessed Asian corn prices at a 35-month high of $278/mt CFR on March 13, retreating to $264.5/mt CFR on March 19 and $266/mt on March 27. Regional grains traders reported a near $10/mt rise in freight rates since the conflict began Feb. 28, with US Pacific Northwest to South Korea June shipment freight reaching a record high of $51/mt and Argentina to South Korea May loading freight hitting $76/mt on March 13, before declining to $37/mt and $56/mt respectively on March 27. Strait of Hormuz disruptions reduced fertilizer exports, with FOB Middle East granular urea prices jumping 58% since the conflict began to $625/mt March 27, according to Platts data.

What's next? Asian buyers are unlikely to materially reduce overall feed grain demand, but procurement will become more opportunistic and fragmented, with a partial pivot toward alternative and closer origins, according to Vladimir Zinkovski, senior principal analyst and head of Asia-Pacific crops at S&P Global Energy CERA. Feed millers may optimize formulations through substitution and adjust inclusion rates, meaning demand destruction remains limited and the more likely outcome is demand deferral as buyers delay purchases and diversify origins. If tightness extends into later planting cycles, reduced or delayed fertilizer application could lower yields and impact quality, skewing downside production risk toward prolonged disruption scenarios.

Reporting and analysis by Nikolaos Aidinis Antonopoulos, Marina Ledakis, Alara Tizer, Megan Gildea, Atsuko Kawasaki, Samyak Pandey, Vivien Tang and Edward Low.