S&P Global — 17 Apr, 2023 — Global

Daily Update April 17, 2023

By S&P Global

Start every business day with our analyses of the most pressing developments affecting markets today, alongside a curated selection of our latest and most important insights on the global economy.

Slow and Steady Works for Japan

Never let it be said that markets are immune to '80s nostalgia. “Top Gun” is back in movie theaters, Depeche Mode is back in concert and Japan is back for investors. After several challenging decades following the collapse of the Tokyo real estate bubble, Japan is earning a second look from risk-conscious investors. The Bank of Japan’s glacial pace of policy, well-capitalized banks and a resilient corporate sector create an attractive, if unexciting, recipe that is luring overseas investment. Despite the talk of change that preceded the appointment of new Bank of Japan Governor Kazuo Ueda, little has changed for Japan’s economy.

In late March, overseas investors began buying Japanese corporate and government debt at the highest level since tracking began in 2005. Turmoil in the U.S. and European banking industries spooked investors, and yen bonds appeared a safe harbor. The consistency of Japanese central bank monetary policy, previously a source of mild annoyance for foreign investors, provided a favorable contrast to the less predictable actions of the Federal Reserve and European Central Bank.

S&P Global Ratings anticipates only a modest adjustment to Japanese monetary policy for 2023. In December 2022, the Bank of Japan tweaked its yield curve control policy, allowing 10-year Japanese government bond yields to double to about 0.5% from 0.25%. While there was discussion of a potential change of direction under central bank chief Ueda, the adjustment was relatively restrained when compared with other developed economies. The Bank of Japan expects headline inflation to fall below 2% around 2023-end, accounting for subdued global growth. However, even this relatively low level of inflation is likely to stress household finances in Japan unless real wages rise.

Japan's real GDP is set to grow 1.2% in 2023, according to estimates from S&P Global Ratings. This would give Japan the highest growth rate among major developed economies due to relatively mild inflation, mild monetary policy and a mild slowdown in economic activity.

An increase in interest rates would be financially beneficial for most Japanese banks due to interest income from loans, according to S&P Global Ratings. The outlook for Japanese banks in 2023 remains largely stable. In contrast to many of its global peers, the Japanese banking industry has higher accumulated levels of capital, lower ratios of nonperforming loans and a better base-case forecast for the economy.

A stress test of 1,772 Japanese nonfinancial corporates, performed by S&P Global Ratings, also demonstrated resiliency for the Japanese corporate sector. Anticipated revenue growth of 4.4% and debt growth of 1.4% in 2023 should offset the challenges of higher interest rates and persistent inflation. Japan had a lower percentage of cash flow-negative companies under stress relative to the global average in the stress test.

Overall, terms like “relative,” “stable,” “moderate” and “mild” are unlikely to quicken the hearts of fickle investors. It is through market turmoil and economic uncertainty that the steady pace of the Japanese economy is getting a second look.

Today is Monday, April 17, 2023, and here is today’s essential intelligence.

Written by Nathan Hunt.

Economy

Week Ahead Economic Preview: Week Of April 17, 2023

A busy week for economy watchers culminates with flash PMI updates, which will provide important assessments of business conditions at the start of the second quarter for the U.S., Eurozone, U.K., Japan and Australia. Of primary importance is the degree to which stronger than anticipated growth in March, led by improving service sector performances, can be sustained in April given the headwinds of higher interest rates and banking sector stress. The PMI price indices will also be eagerly awaited for inflation signals.

—Read the article from S&P Global Market Intelligence

Access more insights on the global economy >

Capital Markets

GDP Flatlines In February, But Private Sector Activity Revives — Albeit With Uncertain Outlook

The U.K. economy stagnated in February but once allowance is made for public sector strikes, the official data add to survey evidence to suggest that private sector economic activity has revived so far this year after a difficult end to 2022. However, the official data also corroborate some of the concerns flagged by the PMI data, which suggests that growth could falter again in the coming months.

—Read the article from S&P Global Market Intelligence

Access more insights on capital markets >

Global Trade

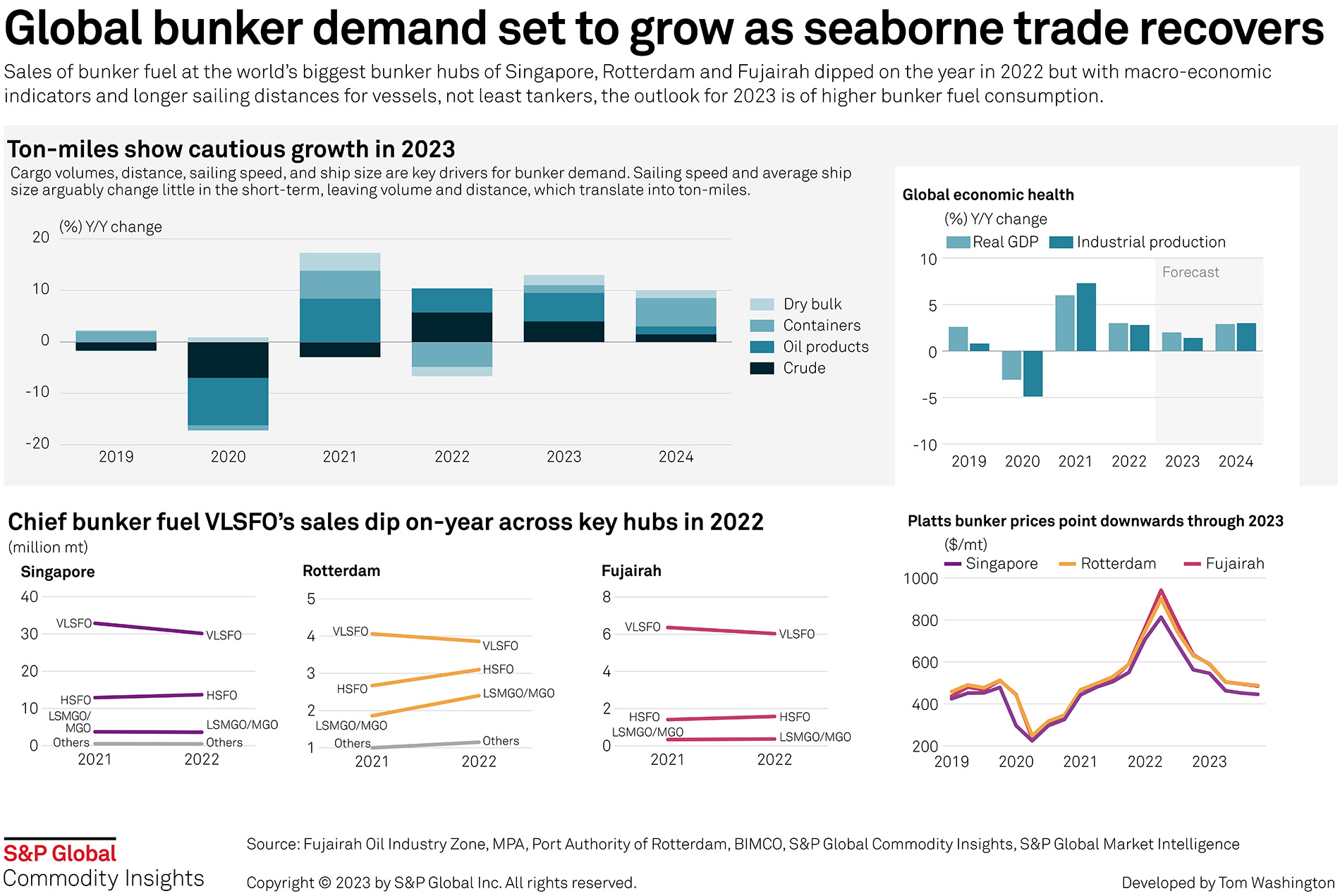

Global Bunker Demand Set To Grow As Seaborne Trade Recovers

The outlook for 2023 is for higher global bunker fuel consumption on the back of longer expected sailing distances for vessels after sales at the key bunker hubs of Singapore and Fujairah fell in 2022.

—View the full infographic from S&P Global Commodity Insights

Access more insights on global trade >

Sustainability

Renewables Firms Await Tax Credit Guidance For Turbocharging Decarbonization

Some renewable project finance developers are putting investment decisions on hold until the federal government provides better clarity on how to monetize tax credits for wind and solar projects in the Inflation Reduction Act, known as "transferability." "It's hard to actually put a deal together when you don't really understand how and when those transfers occur and what is cash when it says it needs to be transferred for cash," Baker Botts LLP project finance attorney Ellen Friedman said in an interview.

—Read the article from S&P Global Market Intelligence

Access more insights on sustainability >

Energy & Commodities

Impact Of OPEC+ Cuts On E&Ps Likely A Top Topic Of Q1 Upstream Earnings Calls

The impact of the surprise OPEC+ production cuts in early April that immediately boosted oil prices will likely take center stage in upstream companies' Q1 earnings calls, as they have the potential to affect capital spending, rig count and output levels. Mergers and acquisitions may also be a target for questions analysts pose to E&P executives as Q1 calls roll out later in April and extend through early May, analysts said.

—Read the article from S&P Global Commodity Insights

Access more insights on energy and commodities >

Technology & Media

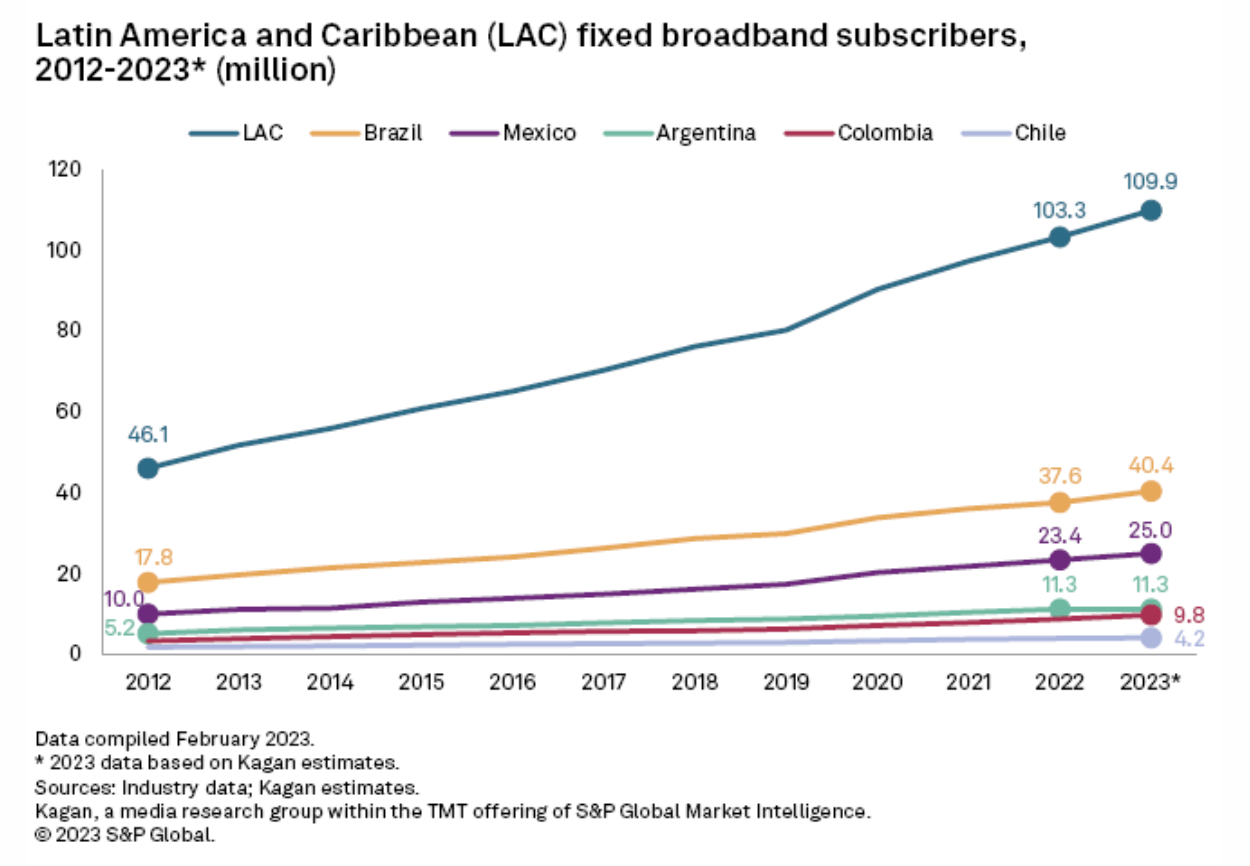

Latin American Multichannel, Broadband, 5G Markets: 2023 Outlook

The expansion of the fixed broadband market remained unabated in the Latin America and Caribbean region during 2022, driven by increased demand for fast and reliable connectivity as well as the continued impact of the COVID-19 pandemic in the form of enduring hybrid work schemes by many companies and the multiplication of streaming services' offerings.

—Read the article from S&P Global Market Intelligence