S&P Global — 21 Sep, 2022 — Global

Daily Update: September 21, 2022

By S&P Global

Start every business day with our analyses of the most pressing developments affecting markets today, alongside a curated selection of our latest and most important insights on the global economy.

China’s Gray Rhino Problem

For years, Chinese authorities have recognized that the scale and extent of domestic corporate debt is a "gray rhino" problem, meaning that a negative outcome is highly probable, and will have a great impact, but is mostly ignored. Over the past five years, the authorities have encouraged deleveraging in the corporate sector as a way of relieving pressure on banks from nonperforming loans. This gray rhino problem is particularly acute for state-owned enterprises, or SOEs, which make up a large segment of the Chinese economy.

For the first time, a group of analysts and researchers at S&P Global Ratings performed a comprehensive analysis of corporate debt in the Chinese market. The analysis, “Global Debt Leverage: China's SOEs Are Stuck In A Debt Trap,” was based on a dataset of 6,363 corporates drawn from the S&P Capital IQ database of S&P Global Market Intelligence. Of these companies, 85% are currently unrated by S&P Global Ratings.

To put the corporate debt challenge into perspective, in the first quarter of 2022, corporate debt in China reached nearly US$29 trillion, an amount roughly equivalent to the size of total U.S. government debt. While Chinese government debt is significantly lower than that of the U.S. or the eurozone, China's corporate debt leverage as a ratio to gross domestic product is 157%, compared with the U.S.’ 82% and the eurozone's 111%.

While publicly owned enterprises in China carry more debt than their Western peers, the debt overhang is particularly acute among a subset of SOEs. The S&P Global Ratings analysis shows the bottom 90% of SOEs are caught in a debt trap and will need outside help in the event of market stress. The ratio of debt to earnings before interest, taxes, depreciation and amortization, or EBITDA, for these SOEs is a rather shocking 18x, compared with a more reasonable 4.1x debt-to-EBITDA ratio for the top 10% of SOEs.

S&P Global Ratings performed stress tests by looking at slowing economic growth, cost inflation and interest rate changes. Its base case projects that 13% of Chinese corporates will be cash flow-negative by 2023, from 9% in 2021. In the worst-case scenario, that figure is 28%.

The problem of overleverage is well known in the Chinese real estate market. But this analysis shows real estate is not the only troubled sector. There are also potential problems for industrials, including construction and engineering, as well as consumer discretionary and consumer staples.

The Chinese government has plenty of tools at its disposal to confront the problem. It has the capacity to extend support to SOEs given comparatively lower government debt. In recent years, the Chinese government has favored market-driven initiatives to deal with overleverage. But the capacity of China's banks to weather an increase in nonperforming loans is uneven due to the lingering effects of the pandemic.

Today is Wednesday, September 21, 2022, and here is today’s essential intelligence.

Written by Nathan Hunt.

Economy

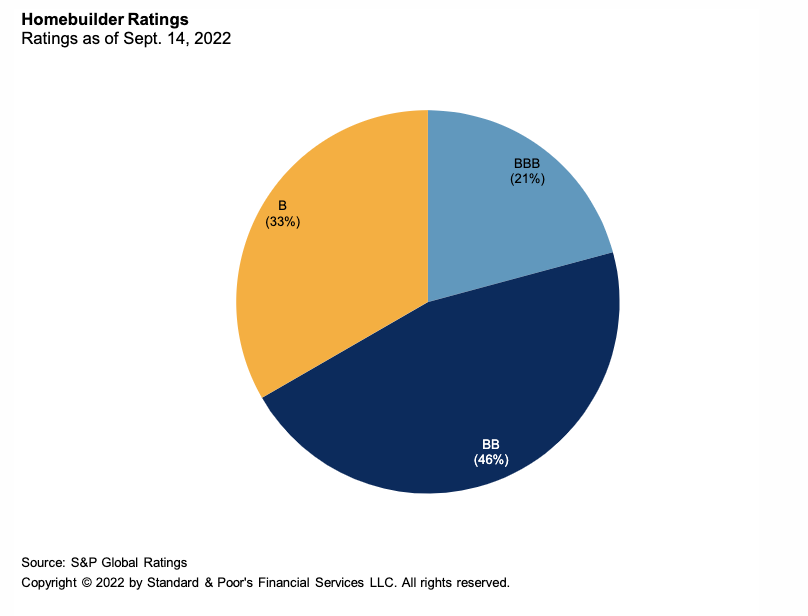

Real Estate Monitor: Negative Rating Bias Grows In The U.S. Real Estate Sector

Second quarter results showed a deceleration in operating momentum from the homebuilders rated by S&P Global Ratings. We believe the sector has reached peak gross margins and expect them to decline over the next several quarters, given slowing housing demand, an increase in cancellation rates, and persistent cost pressure from supply chain issues. Lately builders have been offering more incentives (from almost no incentives a year ago), such as a reduction in the sale price of the homes, pressuring profitability.

—Read the report from S&P Global Ratings

Access more insights on the global economy >

Capital Markets

Japan's Milestone Bill On Stablecoin Promises Tougher Rules For Foreign Players

A landmark law by Japan will make it tougher for foreign issuers of stablecoin to enter the local market and promises greater regulatory oversight following upheavals in the stablecoin market earlier this year. Only entities that are locally chartered will be allowed to issue stablecoins in Japan under the new regulation that comes into effect in June 2023, according to the Financial Services Agency, or FSA.

—Read the article from S&P Global Market Intelligence

Access more insights on capital markets >

Global Trade

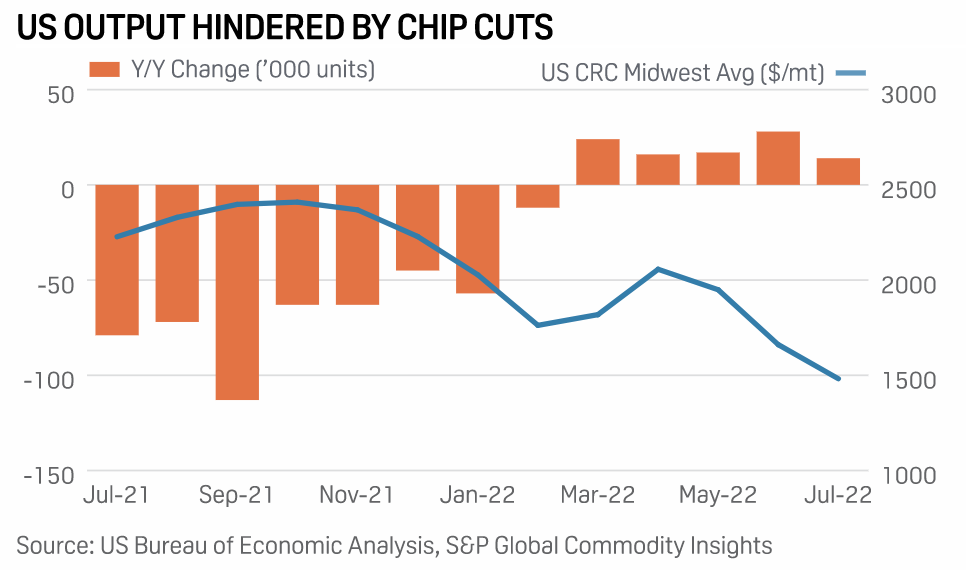

Around The Tracks: Vehicle, Chip Makers Cautious Despite Mostly Bullish Projections

After two years of shortages, the global chip industry's concerns continue to pile up. Chipmakers are now wary about weaker consumer demand, over-stockpiling by manufacturers and changes to US chip export policies. The automotive sector usually accounts for a small portion of a chipmaker's revenue. Take Taiwan Semiconductor Manufacturing Co., for example, which attributes only 3.31% of its 2020 revenue from the automotive segment.

—Read the article from S&P Global Commodity Insights

Access more insights on global trade >

Sustainability

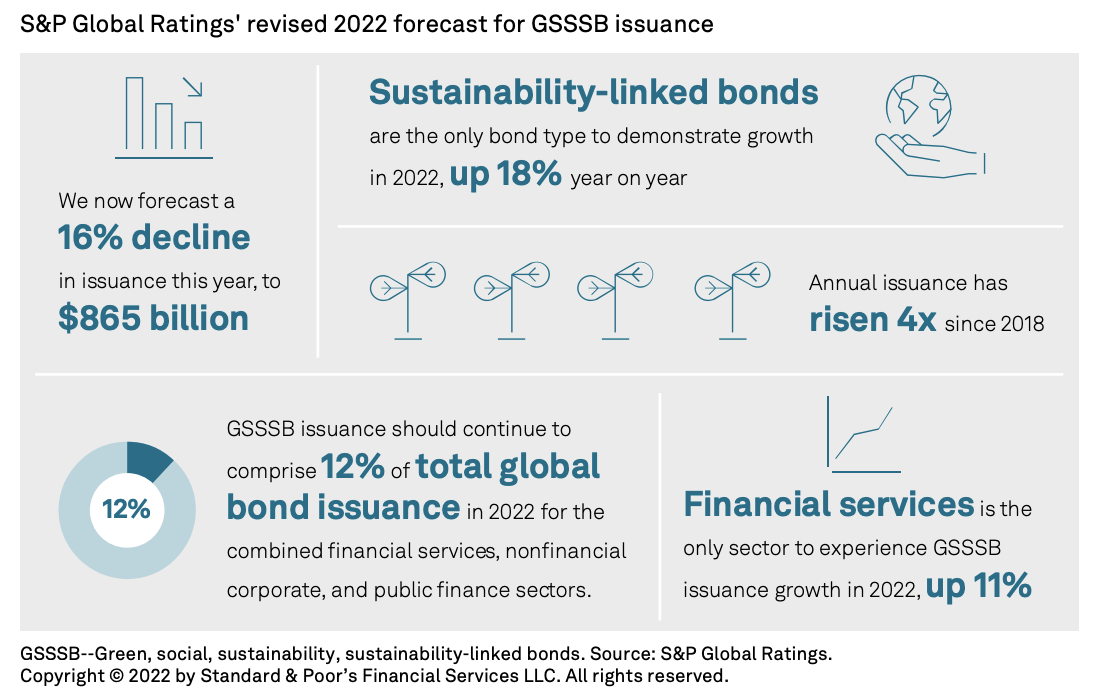

Global Sustainable Bond Issuance: Likely To Fall In 2022

We now forecast a 16% decline in GSSSB issuance this year, to $865 billion. Yet, it should continue to comprise 12% of global bond issuance for the combined financial services, nonfinancial corporate, and public finance sectors. Sustainability-linked bonds are the only GSSSB type to demonstrate growth in 2022, up 18% year on year. Financial services is the only sector to experience GSSSB issuance growth in 2022, up 11%. Annual issuance has risen 4x since 2018.

—Read the report from S&P Global Ratings

Energy & Commodities

U.S. Midterm Elections: What's At Stake For Energy

Democrats clinched a major climate victory this summer with the Inflation Reduction Act. The outcome of the November 2022 midterm elections could impact not only how that law is implemented but also the future of other pivotal climate and energy policies. Join S&P Global and leading industry experts on Oct. 13, 2022, to see how the elections may shift energy policy at the federal and state levels.

—Register for the webinar from S&P Global Market Intelligence

Access more insights on energy and commodities >

Technology & Media

Listen: Next In Tech | Episode 83: (Re)Building The Digital Workplace

The dramatic shift to remote work experienced over the last two years has changed employee expectations about not only where work gets done, but what tools are needed to work efficiently. Senior analyst Conner Forrest returns with study data showing just how attitudes have changed and analyze the impacts with host Eric Hanselman. People are no longer satisfied with the “minimum viable work experiences” driven out of the pandemic. They’ve seen the future and want it now.

—Listen and subscribe to Next in Tech, a podcast from S&P Global Market Intelligence