10 May 2021 | 10:06 UTC — London

Colonial Pipeline closure seen boosting European clean products

Highlights

Gasoline market could be biggest beneficiary of pipeline closure

Cracks remain seasonally high, demand poised to inch higher

Transatlantic freight rates start to firm, seaborne imports like to surge

London — The Colonial Pipeline closure in the US has boosted sentiment in some European refined products, potentially encouraging higher flows into the world's largest oil consumer while also impacting diesel and clean tanker freight markets, trading sources said May 10.

The US is a key importer of European gasoline and vacuum gasoil, and some trading sources expect this arbitrage to see increased activity if the pipeline closure continues to last throughout this week.

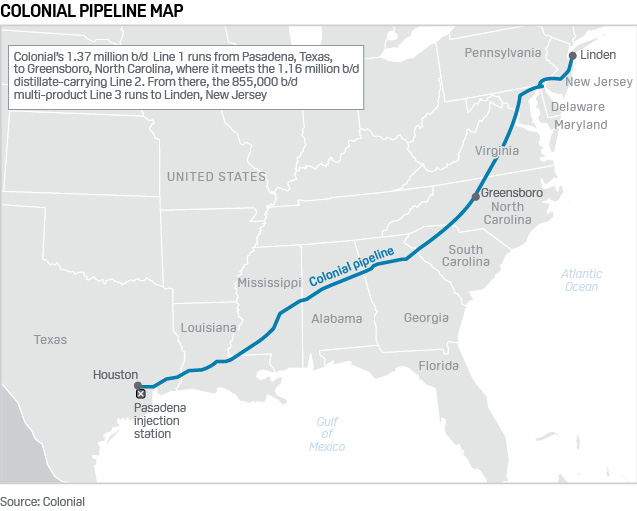

Colonial's operator confirmed on May 9 it had reopened some smaller lines between terminals and delivery points, but its main pipeline network remains down with no timeline for restoration after a cyber attack.

Colonial had halted all pipeline operations because of ransomware, restricting the primary artery for gasoline and refined products for much of the South and East Coast from delivering more than 100 million gal/d of fuel and heating oil.

S&P Global Platts Analytics said it expects a ripple on gasoline and diesel despite this being a potentially short-term event.

"European gasoline is a winner. More imports to New York in a relative short-haul trip. Clean freight gets bid," Platts Analytics said in a note.

However, some European traders remained cautious on May 10.

"To be honest I do not have major hopes in market recovery," said a European based fuel oil trader. "My way of thinking is that this cyber-attack will not take more than few days to fix it. In the end is just online security."

Gasoline boost

Gasoline cracks have already been supported due to resurgent spring demand as COVID-19 vaccinations rise in the US.

USAC refined products inventories are roughly on par with seasonal averages, although with more drivers taking to the road as restrictions ease, gasoline inventories will likely tighten if supplies from Colonial are unavailable.

"With the loss of Colonial's roughly 1.5 million b/d plus of gasoline, inventories will reach 5-year lows (52.4 million barrels seen in October 2017) after 8 days of outages," Platts Analytics added.

A long-term pipeline outage would likely open an arbitrage for waterborne imports, as the region is heavily dependent on Colonial for supply.

NYMEX RBOB and ULSD futures rallied on the open May 9 as Colonial's mainlines remained down. But prices dipped soon after and were rather steady on May 10.

Meanwhile, NYMEX June RBOB surged as high $2.2170/gal before slipping back to trade around $2.1521/gal at 0924 GMT, up 2.52 cents. NYMEX June ULSD was up more than 1% trading at around $2.0373/gal on May 10 morning. Meanwhile, ICE May gasoil was up $6/mt to $556.50/mt at 0900 GMT.

Freight boost

Freight rates for transatlantic tanker routes are also expected to receive a boost. USGC refined products could be shipped by water to the USAC, although that would require the use of higher cost Jones Act vessels. Shippers can apply for Jones Act waivers to the Department of Transport's Maritime Administration, which could not be reached for comment.

"[US Gulf Coast] PADD3 refiners will need to rebalance the products market if that route is impaired for some time," Platts Analytics added. "We don't think that physical storage is a limit, but the gasoline structure imposes a loss to store. We could see more Jones Act ships being used to resupply PADD1[US Atlantic Coast], depending on the outage duration."

The pipeline's closure could also see a jump in USAC imports of refined products, which would help firm continued downward pressure on clean tanker rates from the continent.

Rates for UK Continent-US Atlantic Coast shipments, basis 37,000 mt, firmed between May 3-7 on the back of a rise in gasoline cargo inquiry, but a perceived open arbitrage opportunity for ultra-low sulfur diesel was not apparent, as vessels failed subjects to ship a high volume of ULSD cargoes on transatlantic voyages.

Vacuum gasoil

The US is a major importer of European vacuum gasoil, which could also see some impact. Low sulfur VGO is used by a fluid catalytic cracker to make more gasoline while HSVGO is processed in a hydrocracker to make more diesel. US plants are key exporters of diesel to the global markets while the US is a major consumer of gasoline.

As US refinery utilization rates have picked up, their demand for such products has also grown, trading sources said.

The relative strength of the gasoline crack coupled with the seasonal and post-lockdown increase in driving activity in the US has made gasoline, and therefore LSVGO, more valuable to refiners.