16 Mar 2020 | 16:46 UTC — Insight Blog

Why Saudi Arabia’s oil price war is doomed to fail: Fuel for Thought

Oil price wars rarely achieve their objectives. Saudi Arabia and Russia racing to out-pump each other is unlikely to be any different.

Instead of declaring a victory in seizing market share back from their common rivals in the form of US shale, the main protagonists in Moscow and Riyadh are more likely to cause long-lasting damage to petrodollar economies already under pressure from demand destruction caused by climate change action and the onslaught on the global financial system from the coronavirus pandemic.

The effective collapse of the OPEC+ coalition when the group and its allies failed to agree on an additional 1.5 million b/d of cuts on March 6 has triggered a 30% collapse in prices, with no floor in sight. Brent crude is now threatening to dip below $30/b and test levels last seen back in 2004. Some industry veterans even fear prices could plummet further to historic lows.

Platts Oilgram News front page from September 1960

Abdullah bin Hamad al-Attiyah, Qatar’s former oil minister and OPEC president, fears markets are entering virtually uncharted territory.

"I saw the first shock and the first collapse and this is worse," said the former OPEC grandee in an interview from Doha with S&P Global Platts on March 9. "My expectation is for oil to fall below $20/b. We have seen it before."

OPEC/North Sea price war

Al-Attiyah was referring to the time when former Saudi oil minister Zaki Yamani, under pressure from the kingdom’s late ruler King Fahd, launched the OPEC cartel into a price war with ascendant North Sea producers. The strategy saw crude fall to $10/b and Yamani losing his job. Within a year, Saudi Arabia was forced into an ignominious reversal in tactics in a desperate attempt to boost prices.

Al-Attiyah sees echoes of the crisis playing out in today’s market between Russia and the kingdom.

"I was there when OPEC had its emergency meeting in 1985 and Sheikh Yamani said open full production and the North Sea producer will come begging to Vienna," said Al-Attiyah. "They never came and it took us 15 years to properly recover. We have to learn."

Despite the best efforts of Saudi Arabia, OPEC and fluctuating prices, North Sea producers have proved remarkably resilient. Better technology and efficiency means the offshore basin continues to play an important role in the market. Although the best days are over, its resilience was underscored recently by the start of the giant 450,000 b/d Johan Sverdrup field.

How low can Russia go?

Instead of learning from the 1980s debacle of taking on the North Sea, Riyadh and its Persian Gulf allies were intent on escalating their feud with Russia.

The kingdom heavily discounted its official selling prices to Asia and signalled it would push sustainable capacity up to 13 million b/d. The UAE quickly followed Saudi Arabia’s lead stating it would expedite plans to raise capacity to 5 million b/d.

In response, Russia’s oil minister Alexander Novak said the world’s largest producer of commodities could potentially raise output by 300,000 b/d quickly.

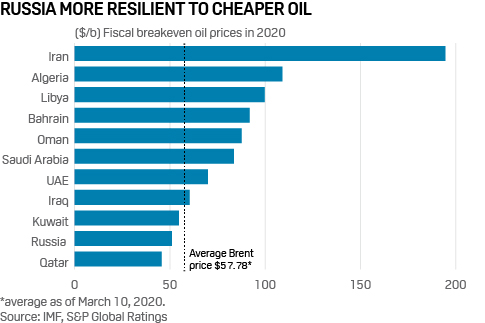

The Kremlin is adamant it can still balance its budget at around $40/b, but the country also exports vast quantities of other raw materials and enjoys a flexible exchange rate, providing it with an economic buffer that Saudi Arabia doesn’t have.

"Everyone will be the loser from this," said Al-Attiyah.

US shale operators look vulnerable

Unless it can eventually push prices back above its fiscal breakeven of around $80/b, the kingdom faces the prospect of running a decade of budget deficits. It is also being forced to drain its foreign currency reserves, which were intended to fund diversification.

"For now it will be survival of the fittest and markets will have to hope a new deal can be struck," said Chris Midgley, head of analytics at S&P Global Platts. But hopes of an early peace have been dashed by the cancellation of the OPEC+ joint technical meeting scheduled for March 18, after Saudi refused to send a representative.

Despite their differences, both Saudi and Russia have a mutual interest in seeing the current collapse in prices damage US shale producers.

Once seemingly an unstoppable force in the oil market, North America’s debt-laden operators now look vulnerable. The US Energy Information Administration forecasts US output to peak just above 13.2 million b/d next month before falling by as much as 660,000 b/d into 2021.

Texas oil barons are spooked. Fracking tycoon and executive chairman of Bakken driller Continental, Harold Hamm has accused Saudi Arabia of "dumping" its crude on the market to damage shale producers. Hamm’s protests didn’t fall on deaf ears in the White House.

President Donald Trump announced late Friday the Federal Government will fill up the Strategic Petroleum Reserve “to the top” to help support the energy industry.

Despite the presidential intervention, Hamm and the entire industry are right to be concerned as the coronavirus pandemic destroys demand as airlines cancel flights and global trade seizes up.

The International Energy Agency forecast on March 9 a full-year reduction in demand of 90,000 b/d in 2020, the first annual fall since 2009. S&P Global Platts Analytics has revised down its 2020 demand growth forecast by over 1 million b/d, from 1.33 million b/d, to just 240,000 b/d.

"2020 is the worst year I have seen since I was born in 1952," warned Qatar’s Al-Attiyah.

Fuel for Thought is a weekly column published first in S&P Global Platts Oilgram News