05 Feb 2020 | 17:21 UTC — Insight Blog

After Petrobras: Brazil’s liberalizing gas market in limbo

By J Robinson

In the first of a new series, S&P Global Platts editors weigh in on Brazil’s liberalizing gas market, taking in opportunities and risks for third-party pipeline imports from Bolivia, private LNG imports from the global market, and the growth of domestic competition in both the offshore and onshore markets.

Last summer, Brazil began opening its natural gas trade to competition through historic market reforms. But recent challenges are raising doubts about the pace and certainty of liberalization.

Brazil’s so-called “New Gas Market” was inaugurated in June with decisive regulatory changes aimed at ending state-owned oil company Petrobras’ monopoly in the country’s onshore markets, and bringing with it the opportunity for increased foreign investment and market efficiency.

The stakes couldn’t be higher. A successful outcome could lower fuel prices for power generators and industry, bring a wave of new foreign investment to Brazil, and give the country’s struggling economy a decisive boost.

Even for neighboring countries – including Argentina, Bolivia and Chile – a fully liberalized gas market could pave the way for similar reforms across South America’s southern cone, potentially creating an integrated regional market that could ultimately become a major consumer and exporter of LNG.

Transport, distribution and onshore production

Within weeks of the new regulatory framework being introduced, Petrobras announced the sale of a 90% stake in two key midstream gas transportation companies: Transportadora Asociada de Gas or TAG and Nova Transportadora do Sudeste or NTS, both of which account for two-thirds of the countries gas pipelines.

Furthermore, Petrobras also sold major stakes in its state-level gas distribution companies to Japan's Mitsui. Previous to the sale, Petrobras had held a stake in 21 of Brazil’s 27 state gas distributors.

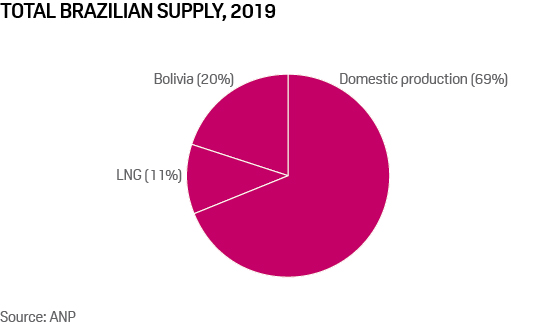

Just two months later, another of Petrobras’ midstream subsidiaries, Transportadora Brasileira Gasoduto Bolívia-Brasil or TBG, – which imports over one-fifth of the country’s marketed gas supply on the 1.1 Bcf/d Gasbol import pipeline from Bolivia – announced an open season for some 60% of its capacity.

In the open season, TBG approved the participation of 18 rival shippers. Among them were foreign oil companies, industrial end-users and state-level distribution companies, along with Petrobras.

Brazil’s National Petroleum Agency, or ANP, simultaneously announced plans to reactivate Brazil’s stalling onshore production – which now comprises less than 20% of the country total domestic output – in a coordinated effort to bring new, third-party producers into Brazil’s gas market.

In the weeks that followed, the future of Brazil’s New Gas Market looked bright, with competitive gas imports from Bolivia expected to hit the domestic market by January 2020.

That burgeoning promise was scuttled just days before Petrobras’ 20-year gas import contract with Bolivia was scheduled to expire on December 31. At the time, ANP abruptly suspended its open season for the Gasbol import pipeline, citing irregularities in the bidding process.

Petrobras, it said, had submitted a bid for the pipeline’s entire 18 million cu m/d contracted import capacity, citing political instability in Bolivia for its aggressive bidding move.

In a subsequent decision that followed weeks later, the ANP reauthorized its Gasbol open season under new rules that will exclude the participation of Petrobras. Still, the delay has raised questions about whether and how quickly other sectors of Brazil’s natural gas market will liberalize.

LNG and offshore competition

As Petrobras’ ambitious and hopeful rivals await the launch of ANP’s reauthorized open season in August, competitive forces in other sectors of Brazil’s gas market seem to face a longer time horizon.

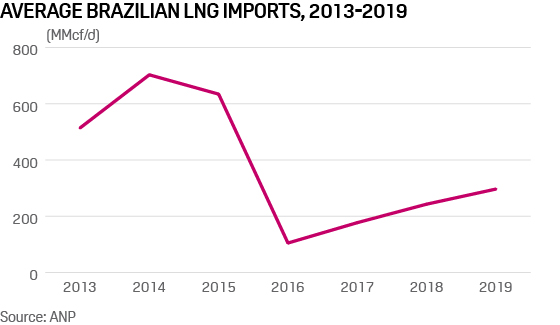

Brazil’s first private LNG-to-power project, which could begin ramping up just days from now, promises to bring competitively priced LNG imports to Brazil’s Northeast. But with limited pipeline infrastructure in the region, excess LNG supplied to the project isn’t likely to reach Brazil’s broader market in any meaningful way.

A second private LNG-import project at the Port of Açu in the state of Rio de Janeiro state, could offer better access to Brazil’s gas grid, but currently faces a longer time horizon for completion.

Third-party producers already operating in Brazil’s offshore subsalt fields offer Brazil’s most hopeful, but also its most distant source, of competitively priced gas supply.

With existing and under-construction offshore-to-onshore pipeline routes largely controlled by Petrobras, third-party producers face limited access to the liberalizing midstream markets onshore.

The limitation reduces the effectiveness of offshore gas meeting Brazilian demand and easing pricing. Over the past five years, Brazil’s offshore gas production has grown by 31%, reaching over 4 Bcf/d this past summer.

According to recent data from Brazil’s Ministry of Mines and Energy, Petrobras supplies gas to end-users at around $8 to $9/MMBtu – a steep premium when compared to sub-$2/MMBtu gas at the US Henry Hub.

Under the existing regulatory framework, getting competitively priced offshore gas production into Brazil’s domestic market requires that third-party producers finance, fund and construct new subsea pipeline routes – a planning and logistical process that could take years.

Additional reporting by Ryan Ouwerkerk