05 Mar 2020 | 22:02 UTC — Denver

US working natural gas in underground storage decreases by 109 Bcf: EIA

Highlights

Storage volumes increase to 48% above this time last year

Draw of 40 Bcf forecast for week in progress

Denver — US working gas stocks fell by 109 Bcf last week, likely marking the final triple-digit draw of the season, as volumes surge to nearly 50% more gas in storage than this time last year.

Storage inventories fell to 2.091 Tcf for the week ended February 28, the US Energy Information Administration reported Thursday morning.

The pull was slightly more than an S&P Global Platts' survey of analysts calling for a 105 Bcf withdrawal. It was less than the 152 Bcf pull reported during the corresponding week in 2019 but more than the five-year average draw of 106 Bcf, according to EIA data. Storage volumes now stand 680 Bcf, or 48%, more than the year-ago level of 1.411 Tcf and 176 Bcf, or 9%, more than the five-year average of 1.915 Tcf.

US working gas stocks have reported stronger than average declines for most of February, but warmer temperatures for the last week of month saw residential and commercial demand slashed 7.4 Bcf/d, according to S&P Global Platts Analytics. US-level, population-weighted temperatures increased 3 degrees week over week, led by the Midwest, which gained 8 degrees week over week.

The NYMEX Henry Hub April contract slipped 1 cent to $1.817/MMBtu in trading following the release of the weekly storage report. The entire 12-month contract strip edged lower by about 3 cents this morning to an average $2.13, with much of the sell-off weighted towards the front of the curve. With winter officially in the books and April taking the prompt month position, the next ten months are each priced higher than the one before, which puts the price of gas higher in October than the higher-demand months of July and August.

Platts Analytics' supply and demand model currently expects a 40 Bcf draw compared to the five-year average pull of 99 Bcf for the week ending March 6. This would further expand the storage surplus with only about three more weeks of withdrawals remaining before the flip to net injections.

Balances continue to move wider as the winter season moves toward the exit, making for the second straight week where balances have loosened by upwards of 7 Bcf/d, according to Platts Analytics.

Demand once again took a tumble, averaging 102 Bcf/d this week. Notably, the Northeast and Midwest have not been the largest contributors to the drop, and instead the Southeast and Texas regions are driving significant losses in demand, falling by 2.2 Bcf/d and 1.5 Bcf/d, respectively, on a combination of LNG feedgas losses, joined by lower power and residential and commercial as well. Upstream, supplies have also softened, falling 0.5 Bcf/d compared with the week prior, after a slight increase in LNG sendout was outdone by a more than 0.6 Bcf/d drop in Canadian imports and a 0.1 Bcf/d drop in onshore production.

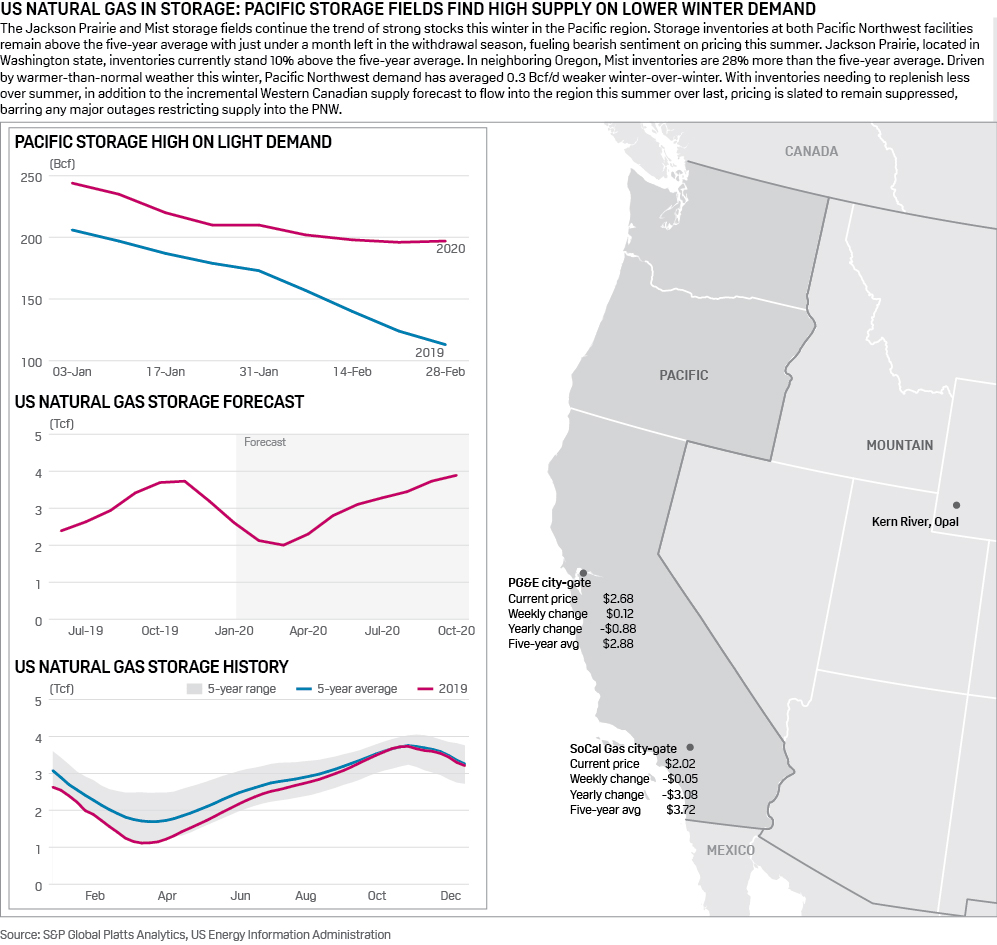

Barring a surprise cold snap, US working gas in storage looks likely to exit the heating season at roughly 2 Tcf, 300 Bcf more than the five-year average and nearly 900 Bcf more than 2019. Currently, only the Mountain and Pacific regions hold working volumes below the five-year average. However, the Pacific made massive year-over-year gains, as storage stands 74.3% higher than this time last year, due in part to increased optionality at the Aliso Canyon storage field.

The Midwest region's storage surplus relative to last year's mark hit a winter-to-date high Tuesday as the region looks to finish well above last year. This winter to date, withdrawals have averaged 0.5 Bcf/d below the five-year average, according to Platts Analytics. Should this continue, the excess storage will likely weigh on Chicago's summer basis, which is trading 2 cents above last year's summer strip of minus 24 cents/MMBtu relative to Henry Hub.

Click here for full-size storage infographic

{kind=link}