06 Feb 2020 | 21:46 UTC — New York

Factbox: Commodity traders weigh impact of coronavirus as force majeure placed on LNG

New York — Commodity traders on Thursday continued to weigh the impact of the coronavirus on demand growth and prices.

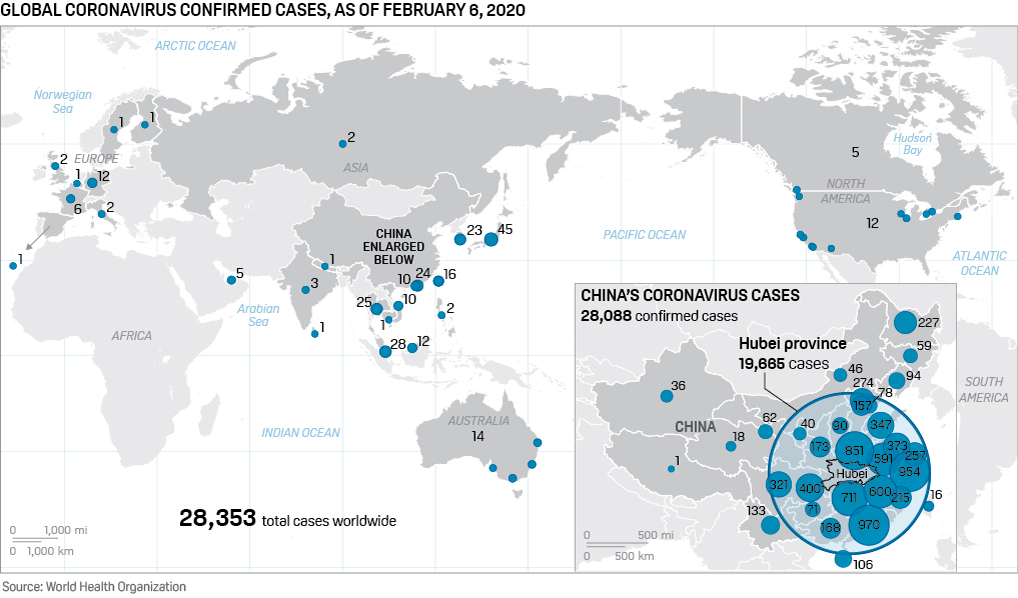

Globally, the number of confirmed cases has risen to 28,353, with 28,088 of those in China, according to John Hopkins University.

With airlines canceling flights into and out of China, and businesses closing stores in infected areas, GDP is expected to take a hit, weighing on commodities demand.

China's state-owned CNOOC has declared force majeure on LNG contracts, a source close to company said Thursday.

The force majeure by CNOOC further dims China's demand outlook and raises concerns about its impact on global trade flows and prices, with Platts JKM plunging to a historic low Thursday of $3.00/MMBtu.

However, the LNG market was already looking bearish.

"The coronavirus outbreak is not fundamentally changing the direction of the LNG market," said Ira Joseph, Platts Analytics Head of Power & Gas. "It was already weak and heading in this direction. Last year, S&P Global Platts Analytics forecasted $3 JKM prices to emerge in 2020; the outbreak is only speeding up their arrival and creating conditions for it to last longer."

Crude prices seem to have found a floor. NYMEX front-month crude has gained $1.34 since Tuesday, settling at $50.95/b Thursday, although is still down $7.59 since January 20, when news of the coronavirus began to rattle markets.

Saudi-led efforts to implement deeper oil output cuts to tackle the virus' impact remained in limbo Thursday, with key ally Russia not yet on board with a proposal for 600,000 b/d in new supply curbs.

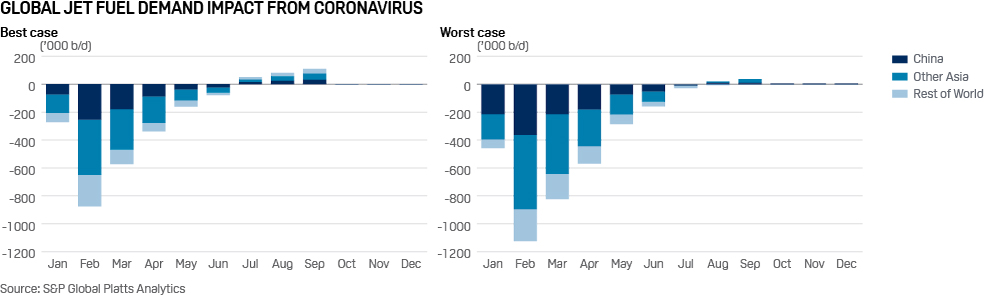

S&P Global Platts Analytics' worst-case scenario shows a drop of 4 million b/d in global oil demand in February because of the virus, with the best-case scenario shows a drop of 1.5 million b/d.

Click here for fuill-size image

{kind=link}

PRICES

Oil

**Dated Brent was assessed by S&P Global Platts at $53.97/b Thursday, down $10.45, or 16%, since January 20.

**The crude price drop has been seen primarily in the front of the curve, reflecting the expectation that demand losses will be short-lived. The NYMEX crude front-month/six-month spread settled in an 82 cents/b contango Thursday, compared to a $1/b backwardation January 20.

**Angolan and Republic of Congo crude grades are under pressure due to the lack of demand from China. Platts assessed Dalia at a 25 cents/b premium to Dated Brent Thursday, down from a $1.85/b premium January 24.

**The Singapore jet crack spread against Brent ended Thursday at $9.20/b, up from $7.02/b Monday but still down from $11.34/b January 20.

**The Rotterdam jet fuel crack against Brent ended Thursday at $12.39/b, down from $14.17/b January 20, but up from $9.97/b on Monday.

LNG

**The Platts JKM, the LNG price benchmark for the Northeast Asia region, fell to an all-time low for a second straight session to be assessed at $3.00/MMBtu Thursday.

Shipping

**The West Africa to East route for VLCCs was assessed at $17.29/mt Thursday, up $1.08 on the day, but down $15.13 since January 21.

**The Arab Gulf to China VLCC route was assessed Thursday at $9.28/mt, down $10.72 since January 20.

Metals

**The front-month rebar futures contract on the Shanghai Futures Exchange closed at Yuan 3,368/mt Thursday, down 9% from recent high on January 20.

**Platts assessed the 62% Fe Iron Ore Index at $82.15/dry mt CFR North China Thursday, up $1.60 on the day, but down 14% from January 20.

**The London Metal Exchange three-month copper price ended $5 higher Thursday at $5,737.50/mt. That was up for the fourth day straight, from $5,587/mt January 31, but still down $334 from January 20. Copper is often seen as a barometer for global economic health.

TRADE FLOWS

Oil

**Platts Analytics worst-case scenario shows a drop of 4 million b/d in oil demand in February; its best-case scenario shows a drop of 1.5 million b/d in oil demand for February.

**Platts Analytics worst-case scenario shows a drop of 1.125 million b/d in global jet demand in February; its best-case scenario shows a drop of 876,000 b/d in for February.

Click here for full-size image

{kind=link}

**Key international airlines have suspended or reduced flights due to the virus, with American Airlines Thursday saying it was extending cancellations through March 27, according to CNBC.

**Hong Kong airline Cathay Pacific said that it intends to cut flights by around 30% over the next two months, including a cut to flights to China of 90%, while staff have been asked to take unpaid leave from March 1 to June 30 to preserve cash.

**The demand destruction was expected to increase jet fuel availability in Asia with the possibility it could make its way into Europe in March.

**Global demand for air freight in 2019 fell by 3.3% on the year -- the first year of declining freight volumes since 2012 and the weakest performance since the 2009 financial crisis when freight contracted 9.7%, according to International Air transport Association data.

**A slump in gasoline demand has many Chinese refineries planning to reduce output or shut plants entirely.

**China's refinery crude runs are expected to be 12 million b/d in February, according to Platts Analytics' best case scenario. In its worst case scenario, runs are forecast at 11 million b/d, down from 13 million b/d assumed before the coronavirus epidemic.

**That reduction represents 30 to 60 million barrels of oil already purchased and on its way to China that will need to be either resold and/or kept in storage for future usage.

**Sinopec, the world's biggest refiner, plans to reduce throughput by around 10% of its total 5.89 million b/d capacity in February. The company's 420,000 b/d Jinling Petrochemical plant will also shut its fluid catalytic cracker as well as its gasoline hydrotreater unit this week for three months as gasoline sales plunge 70% from normal levels.

**Independent refiners in Shandong province have also reduced their average run rates by around 17 percentage points from mid-January to 48% this week, according to local information provider JLC.

LNG

**China's state-owned CNOOC has declared force majeure on LNG contracts, a source close to company said Thursday, as the country's largest LNG importer tackles disruptions in the wake of the outbreak.

**CNOOC has more than 20 million mt/year in FOB and DES sales and purchase agreements.

**Multiple industry sources said force majeure had impacted volumes from Shell, which has a contract with CNOOC for 5 million mt/year, and the Tangguh LNG project.

**Other suppliers of CNOOC's contracts include Australia's North West Shelf and Queensland Curtis LNG, Malaysia's Bintulu, and Qatargas. Total and Petronas also have portfolio contracts with the buyer.

**The force majeure and coronavirus impact, combined with a lack of tariff relief on Chinese imports of US LNG, create a perfect storm for already struggling project developers in the US.

**Several US developers have delayed final investment decisions, with one warning it was running out of cash to continue normal operations.

**Cheniere has a 1.2 million mt/year supply contract with PetroChina. Cargoes are being lifted, but have been diverted since last year due to Chinese tariffs.

**The head of Austria's OMV said Thursday he expected more LNG supplies into Europe in the near future as cargoes are diverted away from China due to the coronavirus outbreak in the country.

**Factory closures and citywide lockdowns could reduce commercial and industrial gas demand, while boosting residential gas volumes, economists at Japan's Nomura bank said.

**Hubei is a major gas hub supplied by four national natural gas pipelines-- PetroChina's West- East line 2, the Huaiwu line (Huaiyang-Wuhan), the Zhongwu line (Chongqing-Wuhan), and Sinopec's Sichuan-Shanghai line, according to local media.

**Platts Analytics forecasts that if reduced industrial activity across Hubei Province extends through the end of February, it would reduce Chinese LNG demand by 5%-7% relative to its base case, driving down imports.

Shipping

**With the coronavirus outbreak coinciding with the Lunar Year holidays, a lack of demand from China has been putting pressure on tonnage requirements out of the West African region. China is a major buyer of WAF crudes.

**Delays in loading and delivery of cargoes in the tanker, dry bulk and container shipping segments are being reported due to ships being forced to sit idle amid a lack of crew availability.

**Singapore, the world's largest bunkering port, has had many resident Chinese nationals returning home from the Lunar New Year holiday. Their return to work, which included crew on ships, workers at ports, shipyards and maritime technicians, is now being delayed due to health inspection and quarantine checks.

**Shipowners who have opted for scrubber installations to comply with the International Maritime Organization's global low sulfur mandate are assessing the impact of the coronavirus outbreak amid the potential for further delays in scrubber fitting programs.

Metals

**Chinese aluminum smelters may cut production due to a shortage of raw materials and a lack of downstream demand.

**The same dynamics are playing out in the steel markets where mills are bringing forward maintenance work as a way of lowering output.

**Henan province produced 10.96 million mt of alumina in 2019, the third largest after Shandong's 25.68 million mt and Shanxi's 19.96 million mt, according to government data. Henan's output accounted for about 15.1% of the nation's total.

**China's finished steel consumption in February could be up to 43 million mt lower than a year ago due to the outbreak closing down construction and manufacturing activity. This equates to a reduction in pig iron consumption of up to 38 million mt.

**Even if the spread of the virus stops accelerating in February, work at factories and construction sites is unlikely to resume to any great extent until February 24.

**In this case, finished steel consumption is likely to be dented by 31 million-43 million mt this month, equating to 28 million-38 million mt of pig iron. The pig iron demand loss is equivalent to around 47%-64% of last February's output of 60.08 million mt.

**China is the world's biggest steelmaker, producing 996.3 million mt of crude steel in 2019, up 8.3% on 2018 and accounting for 53.3% of global output, a growing share, according to the World Steel Association.

**China's car production and sales will be impacted by the coronavirus in the first quarter, denting demand for auto sheet -- but the widespread closure of public transport during the crisis could incentivize new car purchases once things return to normal, S&P Global Ratings analysts said.

**China's auto sector accounts for around 6% of the country's total steel consumption, Platts estimates. The China Iron & Steel Association has forecast that China's total steel consumption will grow by 2% this year to just under 890 million mt.

**The association has predicted that China's passenger car production and sales will decline by 2% this year, which would mark the third consecutive year of declines in the sector.

**A temporary fall in Chinese steel production and demand due to the outbreak and related restrictions could lead to higher steel production elsewhere and a buildup of inventories that may weigh down global steel prices, according to analysts at brokerage firm Jefferies.

**China is the world's biggest iron ore consumer, taking more than half of seaborne supplies.